OPKO Health, Inc. OPK is well-positioned for growth in the coming quarters, supported by the potential of RAYALDEE. Optimism surrounding the stock is driven by RAYALDEE’s strong performance and strategic partnerships. However, overdependence on RAYALDEE remains a key concern.

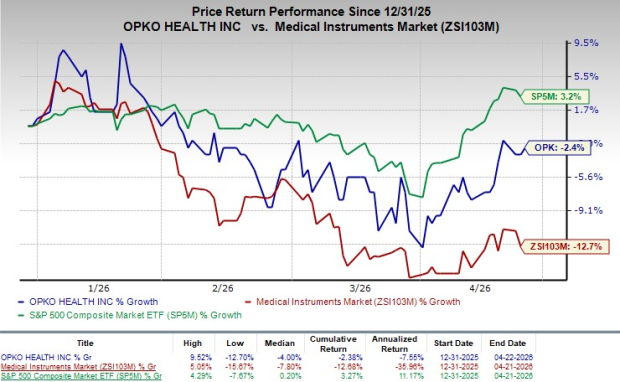

Shares of this Zacks Rank #3 (Hold) company have lost 2.4% in the year-to-date period compared with the industry's 12.7% decline. The S&P 500 has increased 3.2% in the said time frame.

This renowned multinational biopharmaceutical and diagnostics company has a market capitalization of $926.1 million. OPK predicts 10% growth for 2026 and anticipates maintaining its strong performance going forward. The company’s earnings surpassed estimates in two of the trailing four quarters and missed in the other two, the average beat being 41.97%.

Image Source: Zacks Investment Research

Factors Favoring OPK Stock

Strategic Transformation Boosting Profitability Outlook: OPKO’s divestiture of its oncology diagnostics assets has streamlined BioReference into a more focused, cost-efficient operation. Management highlighted a significantly reduced cost base, including nearly 29% workforce reduction, alongside improved margins and operational efficiencies.

The business is now centered on core clinical labs and the 4Kscore franchise, positioning it for positive operating income and cash flow in 2026. This restructuring reduces historical drag from unprofitable segments and enhances visibility into a more sustainable, profitability-driven diagnostics model.

Increasing Contributions From Partnerships and Royalty Streams: OPKO is increasingly benefiting from partnership-driven revenues, including rising profit share from Pfizer’s NGENLA and initial royalties from Lilly’s mazdutide launch in China. The Pfizer gross profit share reached a record $12.5 million in the fourth quarter, reflecting improved market penetration and tiered economics.

These recurring and scalable revenue streams diversify OPKO’s income base beyond its core operations, providing incremental upside with limited incremental cost. Over time, successful commercialization by partners could materially enhance cash flow stability.

ModeX Pipeline Advancing Well: ModeX has evolved into a multi-asset clinical-stage platform spanning oncology, vaccines and immunology, with several programs already in trials and more entering soon. The collaboration with Regeneron, potentially exceeding $1 billion in milestones plus royalties, validates the platform’s scientific value and de-risks development through partner-funded programs.

The Merck-partnered EBV vaccine and BARDA-backed infectious disease programs provide diversified, non-dilutive funding streams, strengthening OPKO’s ability to progress its pipeline without excessive capital strain.

A Factor That May Offset OPK’s Gains

Overdependence on Rayaldee: OPKO Health remains dependent on Rayaldee as a key proprietary pharmaceutical product, and its ability to generate revenues and achieve profitability is significantly influenced by the product’s commercial performance. However, Rayaldee faces competition from alternative treatments and is subject to pricing pressures and reimbursement challenges, which may limit its growth potential.

While OPKO Health is pursuing diversification through pipeline development and strategic partnerships, these initiatives remain in relatively early stages and are subject to significant uncertainty, including clinical, regulatory and commercialization risks. Revenues from newer programs and collaborations may not materialize as expected or within anticipated timeframes.

Any decline in Rayaldee’s sales, negative safety perceptions or reduced market acceptance could have a material adverse effect on OPK’s financial condition. Until diversification efforts yield meaningful and stable revenue contributions, the company remains exposed to concentration risk associated with this single product.

Estimate Trends of OPK

OPKO Health is witnessing a stable estimate revision trend for 2026. In the past 30 days, the Zacks Consensus Estimate for its loss per share has remained stable at 27 cents.

The Zacks Consensus Estimate for the company’s first-quarter 2026 revenues and loss per share is pegged at $130.6 million and 7 cents, respectively. The estimate for revenues indicates a 12.9% decline from the year-ago quarter’s reported number, while that for loss implies a 30% improvement.

Key Picks

Some better-ranked stocks from the broader medical space are Globus Medical GMED, Phibro Animal Health (PAHC) and Cardinal Health CAH. While GMED sports a Zacks Rank #1 (Strong Buy) at present, PAHC and CAH carry a Zacks Rank #2 (Buy) each. You can see the complete list of today’s Zacks #1 Rank stocks here.

Shares of GMED have gained 7.4% in the year-to-date period. Estimates for the company’s 2026 earnings per share (EPS) have increased by 1 cent to $4.46 in the past 30 days. GMED’s earnings surpassed estimates in three of the trailing four quarters and missed one, the average surprise being 18.8%. In the last reported quarter, it delivered an earnings surprise of 20.8%.

PAHC shares gained 44.8% in the year-to-date period. Estimates for the company’s 2026 EPS have remained constant at $3.03 in the past 30 days. PAHC’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 20.1%. In the last reported quarter, it delivered an earnings surprise of 26.1%.

CAH shares lost 0.3% in the year-to-date period. Estimates for the company’s 2026 EPS have increased by 1 cent to $10.32 in the past 30 days. CAH’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 9.3%. In the last reported quarter, it posted an earnings surprise of 10%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

OPKO Health, Inc. (OPK): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).