Amazon.com (AMZN) is sharpening its healthcare ambitions with a calculated push, introducing a program that streamlines access to weight-loss treatments while fundamentally reengineering how GLP-1 therapies reach patients.

The move places the company in direct competition with entrenched leaders like Eli Lilly and Company (LLY) and Novo Nordisk A/S (NVO), but with a fundamentally different playbook built on integration and scale.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Through Amazon One Medical, Amazon is rolling out a “GLP-1 Management Program” that brings together in-person consultations, telehealth access, prescription oversight, and pharmacy fulfillment within a single, coordinated framework. Each element feeds into the next, allowing patients to move through diagnosis, treatment, and follow-up without the usual disconnects that slow care delivery.

The strategy rests on groundwork already in place. Amazon launched its online pharmacy in 2020 and expanded its clinical reach with the 2023 acquisition of One Medical. It previously partnered with drugmakers, offering treatments like Lilly’s weight-loss pill and Novo’s oral Wegovy, but now is stepping beyond distribution into active care management.

By aligning clinical services with logistics and pharmacy capabilities, Amazon is well set for growth.

About Amazon Stock

Amazon started as an online bookstore but now sits at the center of how people shop, stream, and store data. With a market cap of $2.75 trillion, it blends fast delivery, a massive seller network, and cloud infrastructure into one ecosystem, while monetizing attention, logistics, and infrastructure at scale.

The Seattle, Washington-based giant also operates across retail, subscriptions, advertising, and enterprise services, sells its own devices, produces media, and delivers cloud computing, artificial intelligence (AI), and analytics tools globally.

The stock’s performance reflects the operational breadth. Over the past 52 weeks, Amazon shares have surged 41.23%, followed by an additional 10.51% gain year-to-date (YTD). Momentum has intensified recently, with the stock advancing 21.38% in just the past month.

www.barchart.com

www.barchart.com From a valuation standpoint, AMZN stock currently trades at 32.36 times forward adjusted earnings. The multiple places the stock at a premium relative to the broader industry, yet still below its own five-year historical average.

A Closer Look at Amazon’s Q4 Earnings

In its Q4 fiscal 2025 earnings report released on Feb. 5, Amazon delivered a robust top line performance while maintaining operational leverage. Revenue grew 13.6% year-over-year (YOY) to $213.4 billion, exceeding analyst expectations of $211.3 billion, reflecting continued strength across its diversified business segments.

EPS rose 4.8% from the previous year’s period to $1.95 but came in slightly below the Street’s forecast of $1.97. While the marginal miss tempered the headline, it did little to overshadow the company’s underlying momentum, as revenue growth and segment expansion continued to drive the broader narrative.

North America revenue rose 9.9% YOY to $127.1 billion, while International sales climbed 16.8% to $50.7 billion. Moreover, Amazon Web Services (AWS), the company’s most profitable segment, delivered another standout quarter, with revenue increasing 23.6% YOY to $35.6 billion.

Profitability metrics further reinforce the story. Operating income grew 17.8% YOY to $25 billion, while net income climbed 5.9% to $21.2 billion. The balance sheet added another layer of strength as cash and cash equivalents stood at $86.8 billion as of Dec. 31, 2025, up from $78.8 billion a year earlier.

Amazon is scheduled to release its Q1 fiscal year 2026 financial results on Wednesday, April 29, after the closing bell, setting the stage for another closely watched checkpoint. Management expects net sales to land between $173.5 billion and $178.5 billion, translating into a solid 11% to 15% YOY growth against Q1 2025.

On the other hand, analysts project Q1 fiscal year 2026 EPS to surge 1.26% YOY to $1.61. For the full fiscal year 2026, the bottom line is projected to rise 7.67% to $7.72, followed by a further 21.37% increase to $9.37 in fiscal year 2027.

What Do Analysts Expect for Amazon Stock?

AMZN stock has received a reaffirmed bullish stance from KeyBanc Capital Markets equity analyst Justin Patterson. He maintains an “Overweight” rating while raising the price target from $285 to $325, reflecting increased confidence in the company’s forward trajectory.

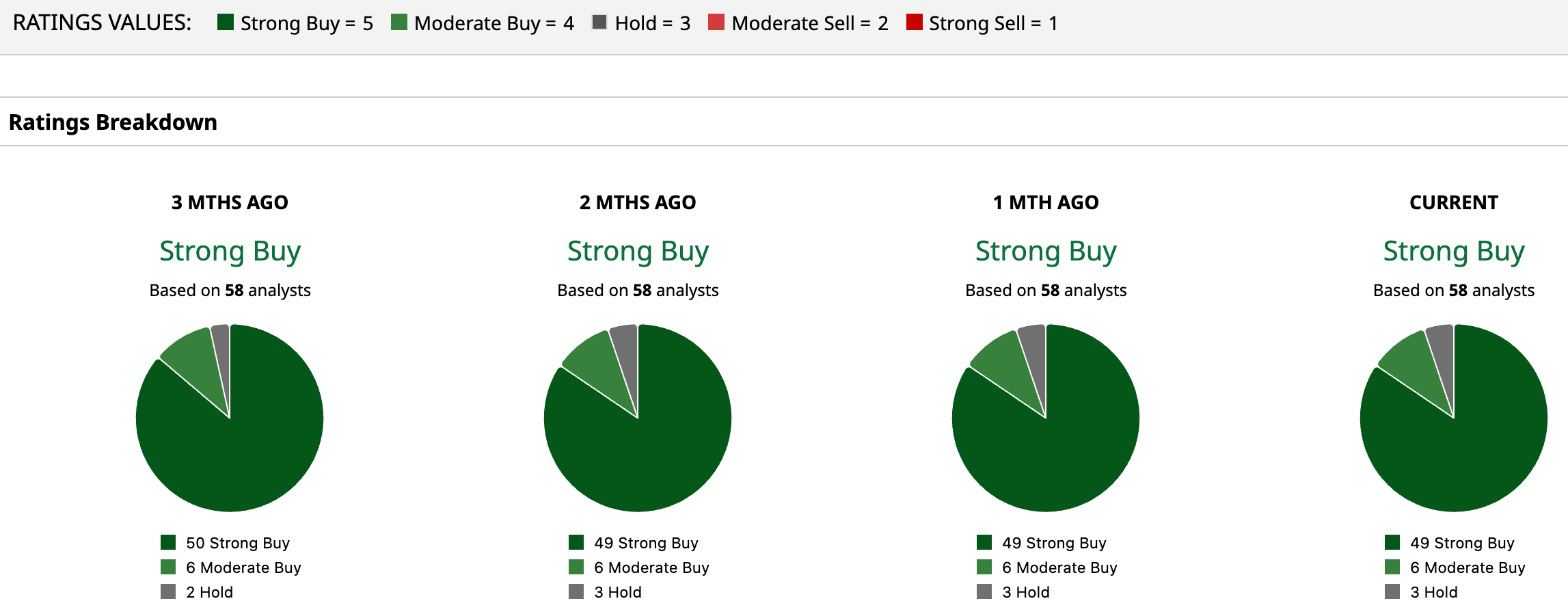

The broader analyst base supports the view, establishing a clear consensus rating of “Strong Buy.” Among 58 analysts covering AMZN stock, 49 have issued a “Strong Buy,” six have assigned a “Moderate Buy,” and three have opted for a “Hold.”

To that end, the mean price target of $288.14 signals potential upside of 13%. Meanwhile, the Street-high target of $360 suggests a gain of 41.2% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tesla Beats in Q1—But TSLA Stock’s Bull Case Still Needs Fuel KeyBanc Sees AI Saving the Day for CrowdStrike Stock Despite Broad Wall Street Panic. Who’s Right? Amazon Aims to Take Over the GLP-1 Market Next. Will That Move the Needle for AMZN Stock? Should You Buy the Dip in ServiceNow Stock Today?