GE Aerospace GE and Howmet Aerospace Inc. HWM are two prominent names operating in the aerospace and defense industry. As rivals, both companies are engaged in producing highly engineered aircraft components for commercial and military aircraft in the United States and internationally.

Both companies have been enjoying significant growth opportunities in the aerospace and defense space on account of the improving air traffic trend and the expansionary U.S. budgetary policy in the past couple of years. Let’s take a closer look at their fundamentals, growth prospects and challenges.

The Case for GE Aerospace

GE Aerospace is benefiting from its growing installed base and higher utilization of engine platforms, supported by strength across commercial & defense sectors. Growing popularity for LEAP, GEnx & GE9X engines and services, supported by growth in air traffic, fleet renewal and expansion activities, is driving its Commercial Engines & Services business.

In the first quarter of 2026, GE’s total orders climbed 87% year over year to $23 billion. Commercial wins included agreements for more than 650 engines, featuring commitments tied to LEAP-1A and GEnx platforms, alongside a long-term materials agreement to support Ryanair’s fleet of about 2,000 CFM56 and LEAP engines.

Operationally, GE pointed to progress under its FLIGHT DECK lean model, including supplier improvements that contributed to commercial services revenues rising 39% year over year. Total engine deliveries increased 43% from the prior-year quarter, indicating better throughput as the company works through customer demand.

Solid demand for the company’s propulsion & additive technologies, critical aircraft systems and aftermarket services in the defense sector is boosting the Defense & Propulsion Technologies business’ performance. In the first quarter, revenues from GE’s Defense & Systems were up 14% on growth in both services and equipment, including unit deliveries rising 24%. Propulsion & Additive Technologies revenues grew 29%, led by Avio Aero.

The company remains focused on rewarding its shareholders handsomely through dividends and share repurchases. In first-quarter 2026, GE paid dividends of $381 million, up 26.2% year over year, to its shareholders. In the same period, it bought back shares for $2.2 billion. Also, the company raised its dividend by 30.6% to 36 cents per share in February 2026.

Despite the positives, GE has been dealing with the adverse impacts of the high cost of sales and operating expenses. In the first quarter, its cost of sales surged 32% year over year to $7.9 billion. Also, research and development expenses totaled $440 million, reflecting a year-over-year rise of 22.6%. The rising debt level remains another concern. Exiting the first quarter, GE Aerospace’s long-term debt was $18.2 billion.

The Case for Howmet

The strongest driver of Howmet’s business at the moment is the commercial aerospace market. With growth in air travel, demand for wide-body aircraft has increased, supporting continued OEM spending. Pickup in air travel has been favorable for the company as the increased usage of aircraft spurs spending on parts and products that it provides.

The sustained strength was attributed to strong demand for engine spares and a record backlog for new, more fuel-efficient aircraft with reduced carbon emissions. Also, healthy build rates at Airbus for A320 and A350 aircraft, along with the production recovery in the Boeing 737 MAX aircraft, hold promise for HWM’s spare engine demand.

Howmet has also been witnessing strength in the defense aerospace industry, cushioned by steady government support. Solid orders for engine spares for the F-35 program and spares for legacy fighters like the F-15 and the F-16 are augmenting HWM’s performance. Robust defense budgetary provisions set the stage for Howmet, which remains focused on its business to win more contracts, which is likely to boost its top line.

HWM’s measures to reward shareholders are encouraging, too. In 2025, the company paid dividends of $181 million and repurchased shares worth $700 million. Also, in August 2025, the company hiked its dividend by 20% to 12 cents per share (annually: 48 cents), marking its second dividend hike in 2025. The company’s healthy liquidity position also adds to its strength.

However, HWM has been experiencing high input costs and operating expenses. In 2025, the cost of goods sold jumped 6.1% year over year to $5.4 billion due to increasing input costs. Selling, general, administrative and other expenses (SG&A) also increased 6.6% to $370 million.

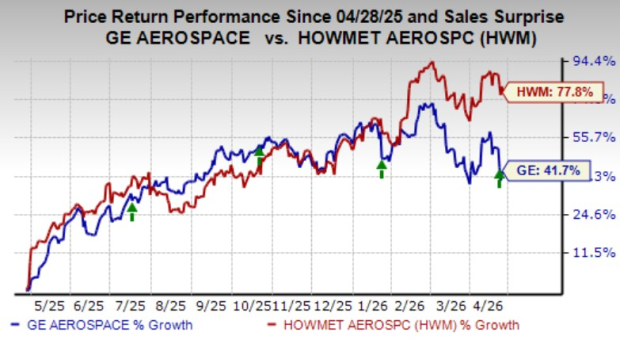

Price Performance

In the past year, GE Aerospace shares have gained 41.7%, while Howmet stock has surged 77.8%.

Image Source: Zacks Investment Research

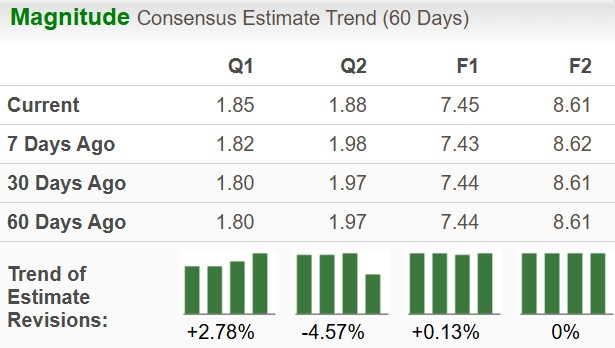

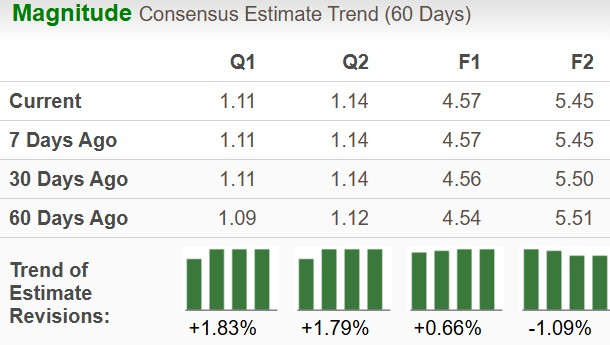

The Zacks Consensus Estimate for GE & HWM

The Zacks Consensus Estimate for GE’s 2026 sales and EPS indicates year-over-year growth of 14% and 17%, respectively. GE’s EPS estimates have been trending northward over the past 60 days for 2026.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for HWM’s 2026 sales and earnings per share (EPS) implies year-over-year growth of 12.1% and 21.2%, respectively. HWM’s EPS estimates for 2026 have increased over the past 60 days.

Image Source: Zacks Investment Research

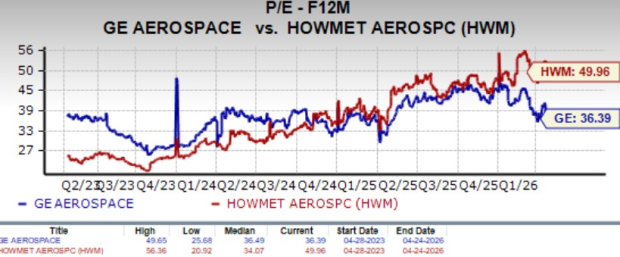

Valuation Comparison

HWM is trading at a forward 12-month price-to-earnings ratio of 49.96X, above its median of 34.07X over the last three years. GE’s forward earnings multiple sits at 36.39X, close to its median of 36.49X over the same time frame.

Image Source: Zacks Investment Research

Final Take

GE Aerospace and Howmet currently have a Zacks Rank #3 (Hold) each, which makes choosing one stock a difficult task. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

GE Aerospace’s strong momentum in the commercial and defense aerospace markets, driven by solid build rates, wide-body aircraft demand and robust defense budget, bodes well for growth. However, GE's strength in the markets has been dented by rising operating expenses and high debt, which might affect its margins and profitability.

In contrast, Howmet’s market leadership position and strength in both the commercial and defense aerospace markets provide it with a competitive advantage to leverage the long-term demand prospects in the aerospace market. Despite its steeper valuation, HWM holds robust prospects due to strong estimates, stock price appreciation and healthy fundamentals. Given these factors, HWM seems to be a better pick for investors than GE currently.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

GE Aerospace (GE): Free Stock Analysis Report

Howmet Aerospace Inc. (HWM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).