On March 19, the U.S. Department of Justice unsealed an indictment against three people tied to Super Micro Computer (SMCI) — including co‑founder and Senior Vice President of Business Development Yih‑Shyan "Wally" Liaw — for allegedly running a scheme to divert about $2.5 billion worth of AI servers with restricted Nvidia (NVDA) chips to customers in China, in violation of U.S. export rules. The next day, SMCI stock sank 33%, marking one of the worst single‑day moves in its history.

The hits kept coming. On April 23, shares slid another 8% after Bluefin reported that Oracle (ORCL) had canceled an order for 300 to 400 Nvidia GB300 NVL72 server racks worth an estimated $1.1 billion to $1.4 billion. Analysts tied the move directly to the DOJ overhang. At the same time, supply-chain checks flagged a separate pile‑up of excess B200 GPU inventory that Super Micro had stocked for xAI, only for that business to shift to Dell (DELL) and HP Enterprise (HPE) instead.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Now, several class‑action securities suits are lined up against the company, covering a period that runs from April 30, 2024 through March 19, 2026. Investors who lost money in that window have until May 26 to apply to be lead plaintiff in federal court. With that deadline fast approaching, can the legal and reputational damage already done be contained before the next shoe drops? Let’s take a closer look.

What Do Super Micro’s Latest Numbers Say?

Super Micro Computer is basically a builder of high‑end servers and storage boxes for the AI world, putting together systems that power big AI, cloud and edge workloads, often tailored to what customers want.

The stock tells a rougher story. Over the last 52 weeks, SMCI stock is down about 24%, and down roughly 5% year-to-date (YTD).

www.barchart.com

www.barchart.com SMCI now trades at about 14 times forward earnings, compared with roughly 24 times for the broader sector, which shows investors are asking for a discount.

The business itself is still growing at an exceptional pace despite the legal and reputational challenges from the indictment. In Q2 2026, net sales jumped to $12.7 billion, up from $5 billion in Q1 2026 and $5.7 billion a year earlier. Gross margin fell to 6.3% from 9.3% in Q1 and 11.8% in Q2 2025, as rapid growth came with more pressure on pricing and mix. However, net income climbed to $401 million from $168 million in the previous quarter and $321 million a year ago, with diluted EPS at $0.60 versus $0.26 in Q1 2026 and $0.51 in Q2 2025.

The company used $24 million in operating cash flow in the quarter and spent $46 million on capex and investments. Even so, Super Micro expects at least $12.3 billion in Q3 2026 net sales, with GAAP EPS of at least $0.52 and non‑GAAP EPS of at least $0.60.

A Look at the Fundamentals

Super Micro continues to push innovation across its portfolio in an effort to sustain momentum amid the ongoing DOJ overhang and lost high-margin contracts. On the edge and enterprise AI front, the company has introduced new compact energy‑efficient edge systems built on AMD (AMD) EPYC 4005 “Zen 5” processors, which are meant for real‑time work in retail, factories, hospitals and branch offices. These systems support DDR5, PCIe Gen 5, and optional GPUs, run at TDP as low as 65W, and include TPM 2.0, AMD Secure Encrypted Virtualization (SEV), 4x GbE ports, plus IPMI 2.0 for remote control, so they fit into tight spaces while keeping power use and security in check.

On the data‑center side, the Gold Series goes after speed and simplicity. The company offers 25-plus pre‑configured servers for AI, compute, storage and edge — with CPUs, GPUs, memory and storage already set — shipping from U.S. warehouses in about three business days. That lets Super Micro offer sharper pricing and much shorter lead times than fully custom builds.

For heavier AI data jobs, Super Micro is also rolling out seven AI Data Platform solutions with Nvidia and partners like Cloudian, DDN, Everpure, IBM (IBM), Nutanix, VAST Data and WEKA. These solutions use Nvidia RTX PRO 6000 and 4500 Blackwell Server Edition GPUs, Nvidia Spectrum‑X Ethernet, and software such as Nvidia NIM and NeMo to give enterprises a ready‑made stack for turning their own data into working AI systems.

What Comes Next?

For the current quarter, Wall Street is looking for earnings of $0.55, up from $0.19 a year earlier, which would mark a huge 189% jump year-over-year (YOY). For the June 2026 quarter, the estimate is $0.52, up from $0.31 last year, implying a strong 68% YOY growth rate. On a full‑year view, analysts expect $1.90 in EPS for fiscal 2026 (up about 10% from $1.72) and $2.49 for fiscal 2027 (up roughly 31% from $1.90).

Even with those growth numbers, JPMorgan has turned more cautious on SMCI stock, cutting its price target to $28 from $40 while keeping a “Neutral” rating. The firm appears to see the stock as a riskier, more balanced call now.

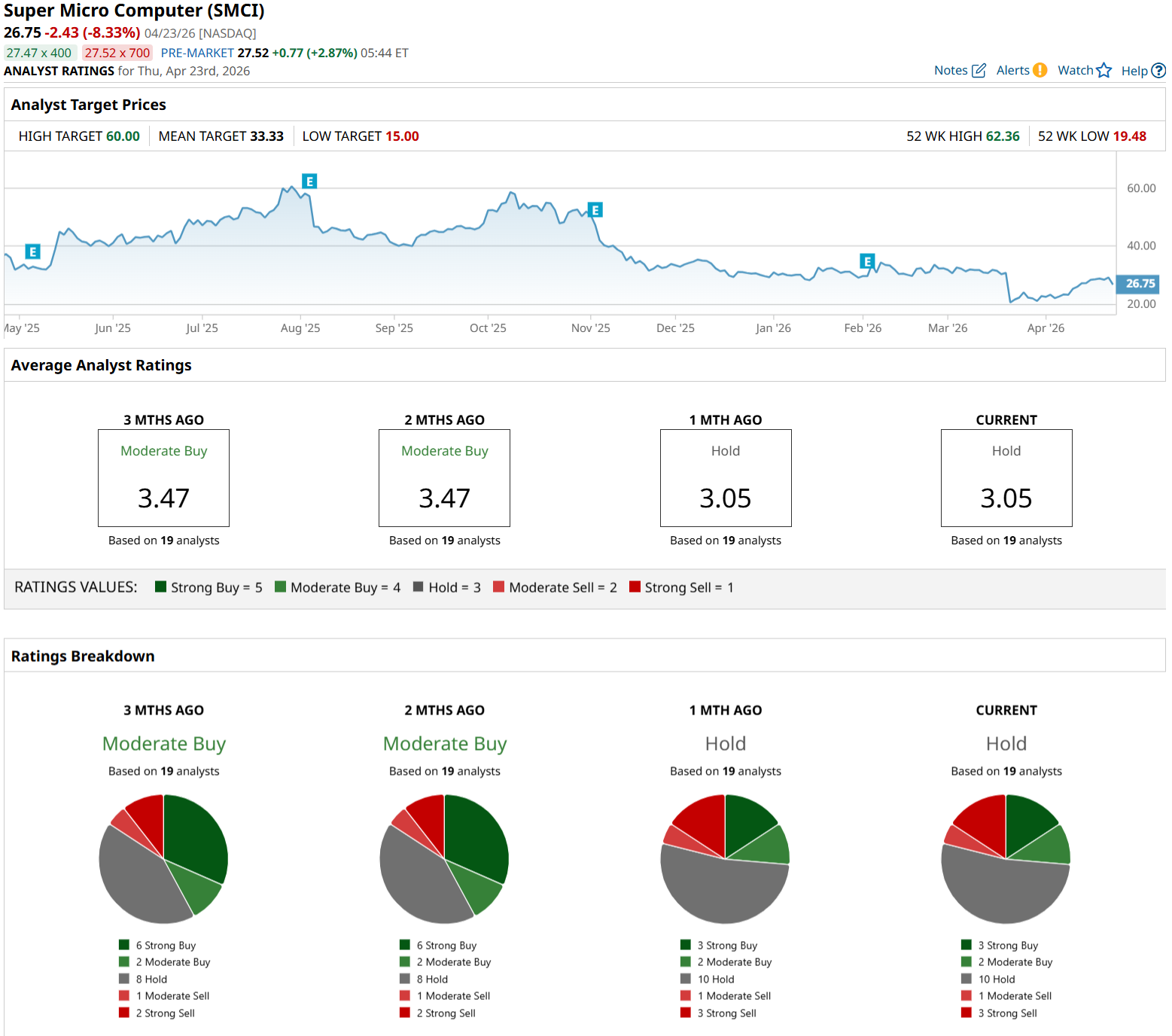

More broadly, 19 analysts tracked by Barchart have a consensus “Hold” rating for SMCI stock. The average price target of $33.33 works out to roughly 20% potential upside from current levels.

www.barchart.com

www.barchart.com Conclusion

For Super Micro fans, the takeaway here is pretty simple: this is still a high‑growth AI infrastructure story, but it is now trading under a legal and reputational cloud that is real, not theoretical. Between the DOJ indictment, the lost Oracle contract, and the May 26 lead‑plaintiff deadline, the path of least resistance in the near term is probably sideways, with sharp reactions around both the May 5 earnings print and any new legal disclosures. Over a longer horizon, if Super Micro can keep delivering on its earnings trajectory and avoid further legal bombshells, SMCI stock could grind higher toward the mid-$30 range rather than collapse outright — but anyone stepping in here needs to treat position sizing and risk management as non‑negotiable.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Kevin Warsh Has Been Labeled a ‘Sock Puppet.’ A Potential Federal Reserve ‘Shadow Chair’ Is a Much Greater Threat for Investors. Follow the Trend Seeker: Beaten-Down SelectQuote Stock Surges 54% in 1 Month as Barchart’s Data Signals ‘Buy’ AMD Stock Slides on Analyst Downgrade. What to Know. Is Qualcomm Stock a Buy Amid Reports of OpenAI Partnership?