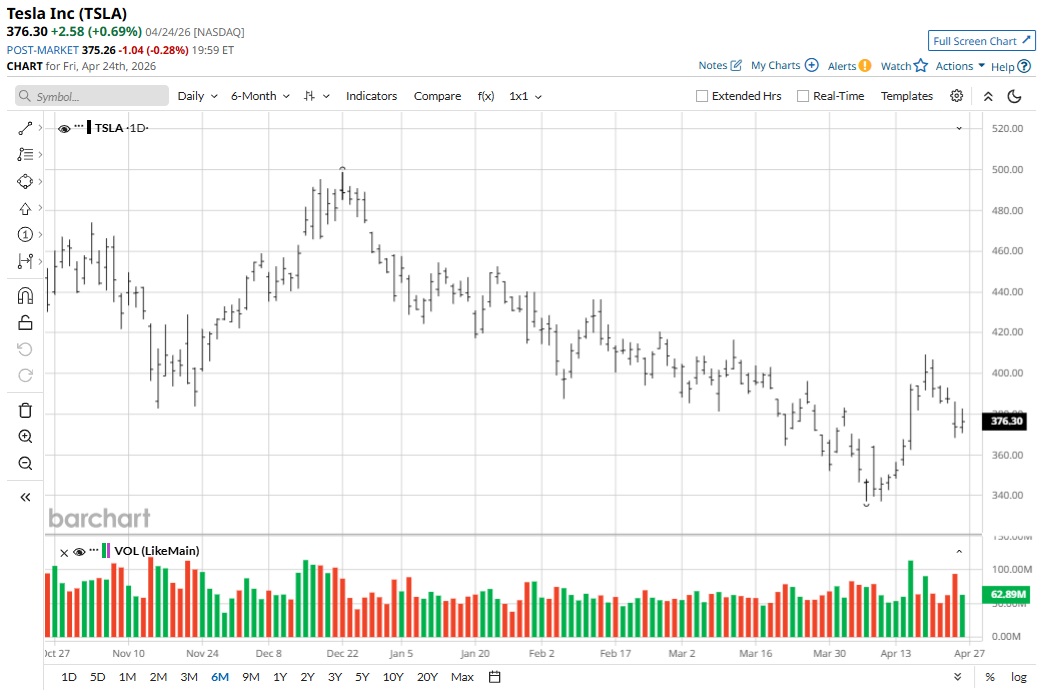

Tesla (TSLA) stock has trended higher by 31% in the last 52 weeks. However, shares have also corrected by almost 25% from the 52-week high of $498.83 in December 2025. Now, the downside seems like a good accumulation opportunity with multiple growth catalysts on the horizon.

Recently, Tesla announced first-quarter fiscal 2026 results. During the period, revenue increased by 16% year-over-year (YOY) to $22.39 billion. Besides multiple positive metrics, Tesla has also indicated that Cybercab, Tesla Semi, and Megapack 3 are on track for volume production in 2026. This is a key top-line growth catalyst.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Among the production ramp-up plans, Cybercab holds immense value creation potential. According to Ark Invest, robotaxi platforms could scale to $4 trillion in net revenue by 2030. This puts the growth potential for Tesla into perspective.

In 2025, S&P Global also opined that Tesla’s robotaxis are likely to drive 45% of automotive sales by the end of the decade. In terms of numbers, Cybercab revenue could possibly reach $1 billion in 2026 and soar to $75 billion by 2030.

If these estimates hold true, Cybercab will likely boost the top line and cash flows in the next few years. The volume production target for 2026 therefore holds significance from the perspective of TSLA stock upside.

About Tesla Stock

Headquartered in Austin, Texas, Tesla is a designer and manufacturer of electric vehicles (EVs) as well as energy generation and storage systems. Currently, the company manufactures five different EV models — the Model 3, Model Y, Model S, Model X and the Cybertruck. Further, the company’s lithium-ion battery energy storage products include Powerwall and Megapack. Tesla also sells energy generation systems directly to customers.

Tesla is currently focused on bringing artificial intelligence (AI) into the real world through products and services like Full Self-Driving (FSD) and Robotaxi. With innovation as a driving factor, the firm remains among the leading players in the global EV ecosystem.

In fiscal 2025, the company produced and delivered 1.66 million vehicles and 1.64 million vehicles, respectively. During the year, Tesla also deployed 46.7 gigawatt-hours (GWh) of energy storage products. This translated into revenue of $94.83 billion coupled with healthy operating cash flows of $14.75 billion.

TSLA stock has declined by 18% in the last six months amid headwinds like intense competition and geopolitical tensions. However, with strong fundamentals and an attractive product pipeline, the outlook remains positive.

www.barchart.com

www.barchart.com Strong Fundamentals Support Growth Plans

Tesla ended Q1 with a cash buffer of $44.7 billion. Operating cash flow for the period was $3.9 billion, implying an annualized OCF potential of $15.6 billion. With multiple top-line growth catalysts, it’s likely that OCF will continue to swell and provide headroom for big investments.

With high financial flexibility, Tesla can pursue potential acquisitions to support accelerated innovation in its core business. Recently, Tesla acquired an unnamed AI hardware company for a consideration of $2 billion.

Another important point to note is that Tesla reported roughly 72% of fiscal 2025 revenue from the United States and China. Accordingly, the company has ample scope for growth in markets like Southeast Asia and Latin America. With recent news of Tesla developing a smaller and cheaper EV, the firm could see significant growth in emerging markets.

What Do Analysts Say About TSLA Stock?

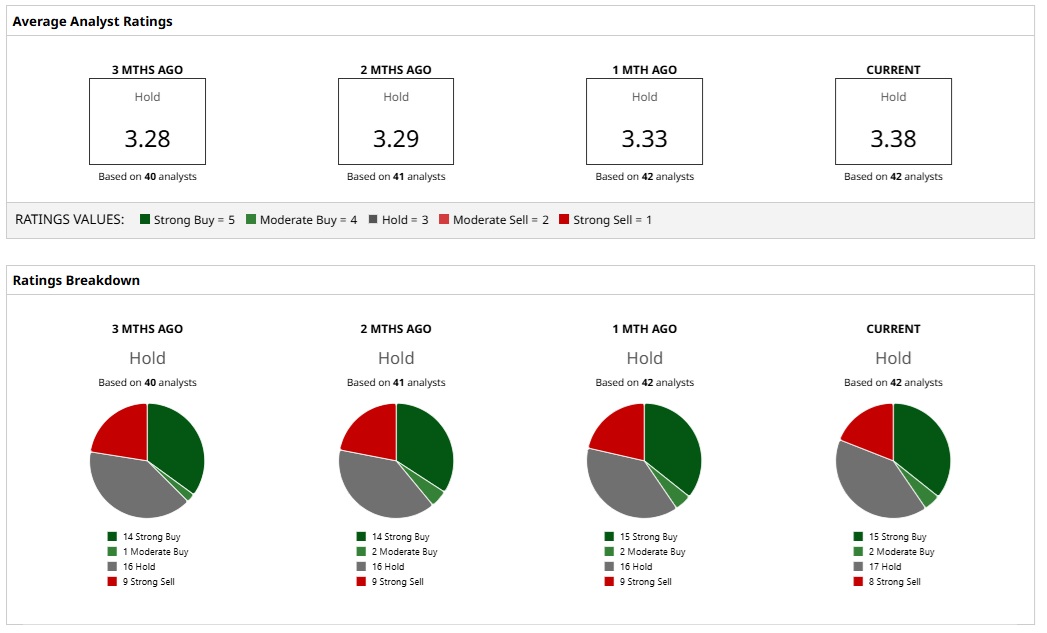

Based on 42 analysts with coverage, TSLA stock has a consensus “Hold” rating. While 15 analysts have a “Strong Buy” rating, two analysts have a “Moderate Buy,” 17 have a “Hold” rating, and eight analysts have a “Strong Sell.” The mean price target of $404.20 represents potential upside of about 8% from current levels. Further, the most bullish price target of $600 suggests that shares could climb as much as 60% from here.

Strong earnings growth is a potential catalyst for a rally. Analysts expect Tesla to deliver earnings growth of 21% and 37% for fiscal 2026 and fiscal 2027, respectively.

Finally, Wedbush believes that the proposed Terafab chip fabrication facility — which is a project between Tesla, SpaceX, and xAI — is a first step toward a potential merger in 2027. This is another potential catalyst for TSLA stock in the next 18 to 24 months.

www.barchart.com

www.barchart.com On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Which Matters Most for Tesla Stock: The Cybercab, the Semi, or Megapack 3? This IBM Stock Bull Spread Allows You to Take Advantage of the Market’s Fear TSMC Is Doubling Down on AI With A13. Does That Make TSM Stock a Buy? AT&T Yields 4.3% and Verizon Yields 6%. Which Telecom Stock Will Actually Pay You More in the Long Term?