Burbank, California-based The Walt Disney Company (DIS) operates as an entertainment company in the Americas and internationally. The company has a market cap of $179.8 billion and operates through the Entertainment, Sports, and Experiences segments, producing and distributing film and television content under the ABC Television Network, Disney, Freeform, FX, Fox, National Geographic, and Star brand television channels.

DIS shares have lagged behind the broader market over the past year, growing 11.1% compared to the S&P 500 Index ($SPX) 28.3% surge. Moreover, in 2026, the stock has declined nearly 11%, lagging behind the SPX’s 4.2% rise as well.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Focusing on its industry benchmark, the State Street Communication Services Select Sector SPDR ETF (XLC) has risen 20.8% over the past year, outperforming the stock. In 2026, as well, XLC declined 2.1% and has rallied the stock.

www.barchart.com

www.barchart.com DIS stock has declined consecutively over the last five trading sessions. Investors are cautious of the stock’s weaker fundamentals. Its large revenue base makes it harder to increase sales quickly; its annual revenue growth of 9.5% over the last five years is below analyst expectations, which is also not a good sign. DIS has also exhibited poor expense management, showcased by an operating margin of 14.8%, below the industry average.

For the current year, which ends in September, analysts expect DIS’ EPS to rise 11.5% to $6.61 on a diluted basis. The company’s earnings surprise history is solid. It surpassed the consensus estimate in each of the last four quarters.

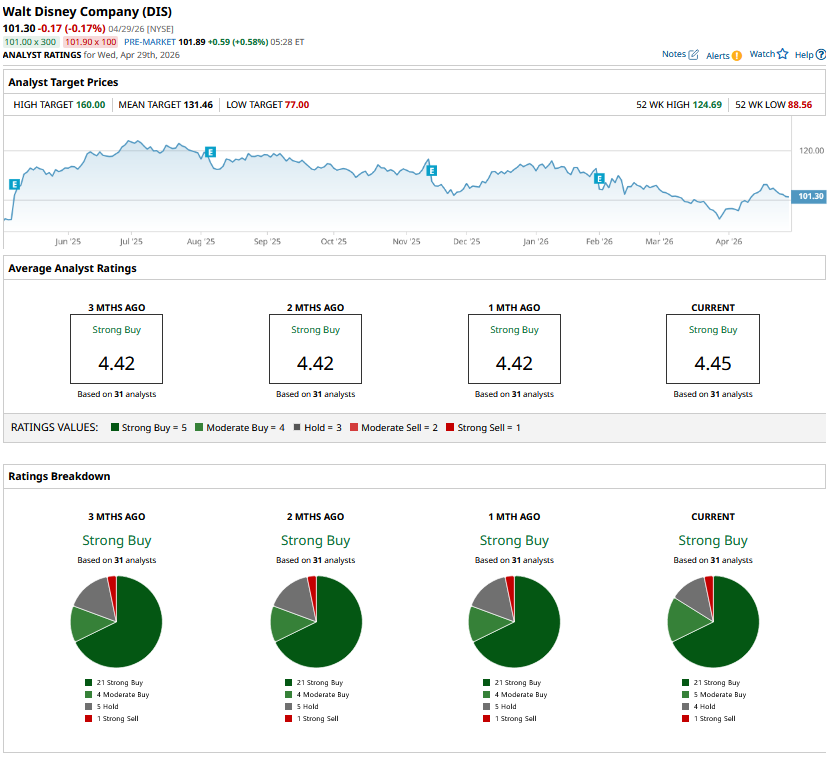

Among the 31 analysts covering DIS stock, the consensus is a “Strong Buy.” That’s based on 21 “Strong Buy” ratings, five “Moderate Buys,” four “Holds,” and one “Strong Sell.”

www.barchart.com

www.barchart.com This configuration has remained mostly stable in recent months.

On Apr. 8, Barclays analyst Kannan Venkateshwar maintained a “Buy” rating for DIS stock and lowered its price target from $140 to $130.

DIS’ mean price target of $131.46 indicates a premium of 29.8% from the current market prices. Its Street-high target of $160 suggests a robust 57.9% upside potential from current price levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Dan Ives Is Betting on 35% Upside for Oracle Stock: This ‘Secret Sauce’ Will Make ORCL a Key Part of the ‘AI Revolution’ Coca-Cola Just Proved Blue-Chip, Dividend Stocks Aren't Boring as KO Stock Pops on 10% Revenue Growth Down Nearly 50% from All-Time Highs, Should You Buy the dip in POET Technologies Stock? ‘I’d Love to Be Able to Save an Airline,’ Says Trump About Spirit. But Is There Any Saving FLYYQ Stock?