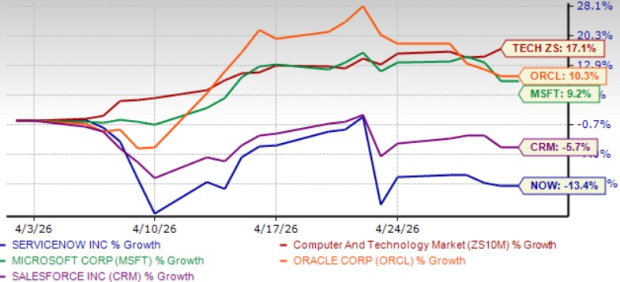

ServiceNow NOW shares have plunged 13.4% in a month, underperforming the Zacks Computer and Technology sector’s return of 17.1%, reflecting macroeconomic and geopolitical challenges, as well as stiff competition. Management noted that first-quarter 2026 subscription revenue growth (22% year over year) faced an approximately 75-basis-point (bps) headwind from delayed closings of several large on-premise deals in the Middle East due to regional conflict, which is expected to spill over to the second quarter of 2026.

NOW’s SaaS business model has suffered from strong adoption of AI-native solutions. Intensifying competition from the likes of Microsoft MSFT, Oracle ORCL and Salesforce CRM has been a headwind for the company. Shares of Microsoft and Oracle have returned 9.2% and 10.3% in a month, while Salesforce has dropped 5.7%.

So, what should investors do with ServiceNow shares? Let’s find out.

NOW Stock’s Price Performance

Image Source: Zacks Investment Research

ServiceNow Stock Trades at a Premium

ServiceNow stock has a Value Score of F, which suggests a stretched valuation at this moment.

The stock is trading at a premium, with a forward 12-month price/sales of 5.35X, higher than Salesforce’s 3.07X. However, NOW shares are trading below Microsoft’s P/S multiple of 8.25 and Oracle’s 5.38.

NOW Stock’s Valuation

Image Source: Zacks Investment Research

NOW’s Subscription Benefits From Armis Deal, Margins Suffer

ServiceNow raised subscription revenue guidance for 2026, which is now expected between $15.735 billion and $15.775 billion, suggesting 20.5-21% on a non-GAAP constant currency (cc) basis. This includes a 125-bps contribution from Armis. However, the subscription gross margin of 81.5% and operating margin of 31.5% includes a 25 bps and 75 bps headwind from Armis, respectively. Free cash flow margin of 35% includes a 200-bps headwind from Armis.

For second-quarter 2026, NOW expects subscription revenues between $3.815 billion and $3.820 billion, suggesting year-over-year growth in the 21-21.5% range at cc. Current Remaining Performance Obligation (cRPO) growth is expected to be 19.5% at cc. Both subscription revenues and cRPO include a 125-bps contribution from Armis. However, the operating margin of 26.5% includes a 125-basis-point headwind from Armis.

The Zacks Consensus Estimate for NOW’s 2026 revenues is pegged at $16.18 billion and indicates 21.9% growth from 2025’s reported figure. The consensus mark for NOW’s second-quarter 2026 revenues is currently pegged at $3.92 billion, suggesting 21.97% growth over the figure reported in the year-ago quarter.

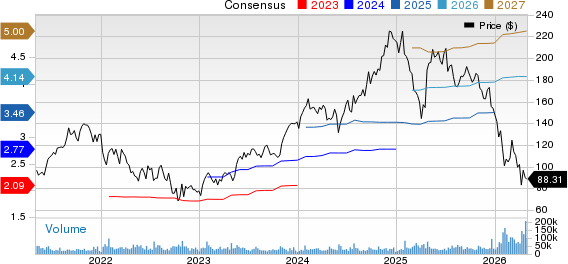

ServiceNow, Inc. Price and Consensus

ServiceNow, Inc. price-consensus-chart | ServiceNow, Inc. Quote

The Zacks Consensus Estimate for NOW’s 2026 earnings has been steady at $4.14 per share over the past 30 days and indicates 17.95% growth from 2025’s reported figure. The consensus mark for NOW’s second-quarter 2026 earnings estimate is currently pegged at 85 cents per share, down 8.6% over the past 30 days and suggests 3.66% growth over the figure reported in the year-ago quarter.

NOW’s Aggressive AI Push to Boost Top-Line Growth

ServiceNow’s aggressive push into AI is strengthening its core platform by embedding intelligence directly into every product rather than treating AI as an add-on. Management emphasized that all SKUs are now AI-native, with incremental “Assist” capabilities layered into pricing. This approach increases attach rates, enhances product value and reinforces the platform’s centrality within enterprise workflows. AI is revitalizing the core business, driving higher customer engagement and expanding the relevance of ServiceNow’s system-of-record foundation across IT, HR, CRM and security.

AI is also emerging as a meaningful and rapidly scaling revenue driver. The company indicated that its AI-related revenue trajectory is already trending toward roughly $1.5 billion, significantly ahead of earlier expectations. This reflects strong enterprise demand as customers move from experimentation to full-scale deployment of AI solutions. Enterprises are using AI-driven automation to reduce labor costs, eliminate redundant tools, and streamline operations, freeing up spending that can be reinvested into the platform. This creates a self-reinforcing adoption cycle: as customers realize efficiency gains, they expand usage, adopt more modules and deepen their reliance on ServiceNow.

Another key benefit is the expansion of NOW’s total addressable market (TAM) through entirely new AI-driven offerings. Products like AI Control Tower, Autonomous Workforce, and EmployeeWorks position the company as the orchestration and execution layer for enterprise AI agents. Rather than competing with large language model providers, ServiceNow sits above them, coordinating workflows, governance and real-time decision-making. This strategic positioning allows the company to capture value from the broader AI ecosystem, effectively turning the proliferation of AI tools into a tailwind for its own growth.

Conclusion

NOW’s expanding TAM, strong portfolio, aggressive AI push and benefits from the Aramis acquisition are expected to improve its top-line growth. However, geopolitical headwind in the Middle East, Aramis’ dilutive impact on margins, stiff competition and stretched valuation are concerns for investors.

ServiceNow currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

ServiceNow, Inc. (NOW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).