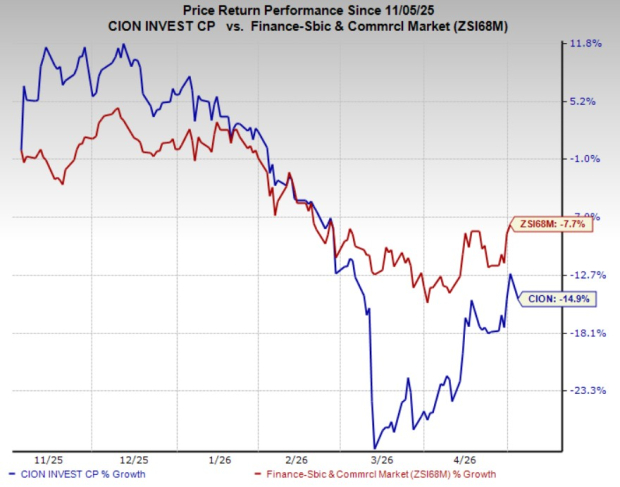

CION Investment Corp. CION is drawing attention for two reasons: a dividend yield of about 15% and a stock price that has fallen hard. The shares are down 14.9% over the past six months compared with the industry's decline of 7.7%.

Image Source: Zacks Investment Research

That combination creates a classic “cheap vs. risky” setup. The yield looks compelling, but the selloff suggests investors are discounting real pressure on earnings power and credit quality.

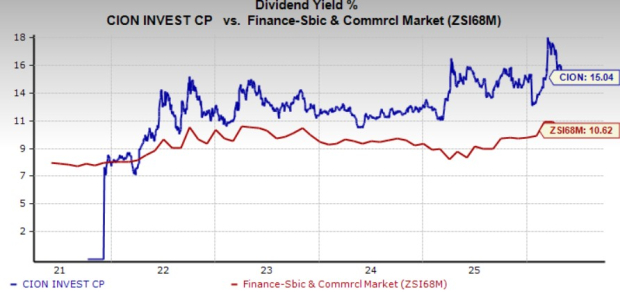

CION Investment’s Yield Looks Big

CION’s $1.20 annualized dividend and 15% yield stand out in a yield-starved market.

Image Source: Zacks Investment Research

For context within the same space, Main Street Capital MAIN and Golub Capital BDC GBDC has a yield below CION’s level. MAIN has a dividend yield of 5.5% while GBDC has a dividend yield of 9.6%. The contrast highlights how the market can assign very different risk premiums across business development companies.

For income investors, the key issue is whether the payout is being supported through a normal cycle. CION’s recent performance points to a tougher operating backdrop, where spreads are tighter, lender protections are looser, and leverage across the private-credit market is rising.

Credit concerns add another layer. Non-accruals climbed sharply beginning in the second quarter of 2025, increasing the risk that portfolio income and valuation marks remain under pressure.

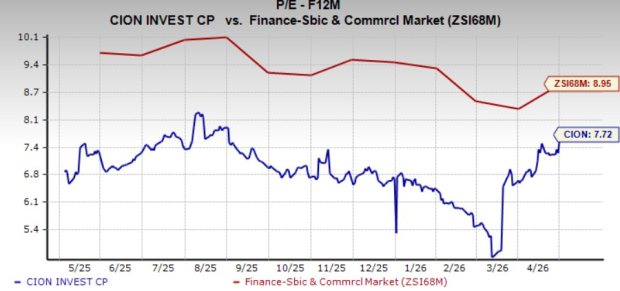

On earnings multiples, CION looks undeniably discounted. The stock trades at 7.72X forward 12-month price-to-earnings, below the Zacks sub-industry at 8.95X.

Image Source: Zacks Investment Research

CION’s Earnings Track Record Has Been Unsteady

CION’s recent earnings execution has been uneven. Results have topped estimates in only one of the last four quarters and missed in the other three.

The fourth quarter of 2025 underscored that challenge. Net investment income was 35 cents per share, below the Zacks Consensus Estimate of 39 cents, as total investment income declined. Total investment income fell 7.1% year over year to $53.8 million, and the top line also came in below expectations.

Expense control helped offset some pressure, with operating expenses down 9.1% year over year to $35.5 million. Still, the earnings pattern reinforces why investors have been reluctant to reward the stock, even at a compressed multiple.

CION’s Liquidity Supports Distributions and Buybacks

CION’s liquidity provides a measurable buffer. As of Dec. 31, 2025, the company held $124 million in cash and short-term investments and had an additional $100 million available under financing arrangements.

That flexibility supports capital returns alongside portfolio management. The company repurchased 555,652 shares in the fourth quarter of 2025 at $9.37 per share, and the repurchase authorization had $24.5 million remaining at year-end 2025.

Liquidity also matters because the company is maintaining its base distribution and shifting to monthly payments in early 2026, which can appeal to income investors who prioritize steady cash flow cadence.

CION’s Leverage and Debt Mix Stay a Watch Item

Leverage remains a central monitoring point. Net debt-to-equity stood at about 1.44X, with total debt of $1.14 billion. The debt mix was roughly 65% unsecured and 35% bank debt.

Portfolio structure provides some support. As of Dec. 31, 2025, first-lien investments represented 80.8% of the portfolio, and approximately 98% of the portfolio was risk rated 3 or better.

CION Investment’s Decision Frame Using Rank, Not Hype

For a practical decision lens, start with the short-term rating profile. CION carries a Zacks Rank #5 (Strong Sell), alongside a Value Score of B but weaker Growth and Momentum scores.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The debate comes down to whether the elevated yield compensates for the specific risks in front of the company. Competitive private-credit conditions are pressuring spreads and structures, regulatory constraints can raise funding costs and limit access to capital markets, and rising non-accruals elevate the probability of weaker near-term income and dividend coverage.

Investors who want exposure to the group without leaning into the highest-risk profile may prefer to compare opportunities across the space, including names like Main Street Capital and Golub Capital BDC, which currently carry stronger Zacks Ranks than CION.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Main Street Capital Corporation (MAIN): Free Stock Analysis Report

Golub Capital BDC, Inc. (GBDC): Free Stock Analysis Report

CION Investment Corporation (CION): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).