Auna S.A. AUNA, the Latin America-based healthcare provider, is set to release first-quarter 2026 results on May 19, after the closing bell.

The Zacks Consensus Estimate for the company’s first-quarter earnings per share (EPS) suggests flat year-over-year growth to 19 cents. The estimate has moved up 1 cent in the past 30 days. The consensus mark for first-quarter revenues currently stands at $318.3 million, suggesting 8.2% growth over the prior-year period.

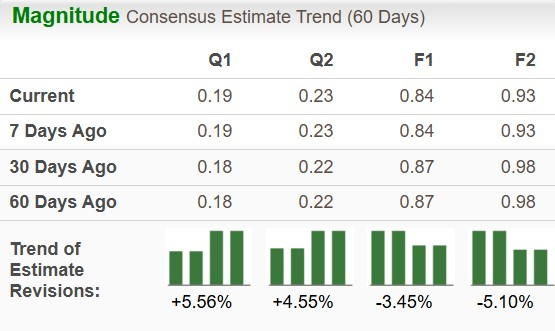

Image Source: Zacks Investment Research

The company has a solid earnings surprise track record, having topped estimates in each of the trailing four quarters, with an average beat of 146.22%.

Image Source: Zacks Investment Research

Q1 Earnings Whispers for Auna

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), along with a positive Earnings ESP, has a higher chance of beating estimates. This is not the case here, as you can see below.

Earnings ESP: Auna has an Earnings ESP of -2.70%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks Rank #1 stocks here.

Factors Shaping AUNA’s Q1 Performance

The company’s consolidated performance in 2025 reflected challenges in its Mexico operations. We assume soft market conditions may have prevailed in the region throughout the first quarter of 2026, affecting surgery volumes and emergency visits and weighing on revenues. However, Auna highlighted stabilization in Mexico in the previous quarter, which is likely to have positioned the business for sustained top-line and EBITDA growth this year.

Under a new leadership team, the company has been working to expand its reach into the larger segments of privately insured families and strengthen alignment with certain physician groups. Auna is likely to have benefited from rolling out targeted pricing initiatives and pre-negotiated physician rates in the Out-of-Pocket segment. In the Institutional segment, the company was awarded an extension of an improved healthcare plan for ISSSTELEON employees, which may have further strengthened the margin profile of the partnership.

The Oncology business is likely to have delivered another quarter of strong performance with the integration of Opcion Oncologia’s physician practice. The newly launched Oncocenter at the Doctors Hospital, which centralizes oncology services while being integrated with Auna's regional health care network, may have also contributed.

Meanwhile, the Peru business is expected to have led the company’s first-quarter performance. Revenue momentum was likely supported by higher complexity services, while investments in new medical equipment, increased bed capacity and targeted marketing initiatives may have driven stronger volumes. On the health plans side, OncoSalud revenues are likely to have benefited from increased total plan memberships. Meanwhile, oncology MLR may have continued its streak of quarterly decrease from a mix of higher tickets and continued moderation in pharmaceutical costs.

In February 2026, Auna announced the formal execution of an addendum to its existing Public-Private Partnership agreement with EsSalud, facilitating the commencement of the construction phase of the Torre Trecca project in Lima.

The Colombia revenues may have gained from the expansion of risk-sharing models for cardiovascular, ambulatory and oncology services, along with continued growth in chemotherapy and imaging services.

Auna also completed a $825 million debt refinancing in the fourth quarter, which improved its maturity profile and lowered its interest expense. Despite the premiums and costs associated with the refinancing, the company maintained its leverage ratio at 3.6, below its target of 3 net debt-to-EBITDA in the medium term. We expect deleveraging progress to have continued in the first quarter.

AUNA’s Peer Earnings Snapshot

Progyny, Inc. PGNY, sporting a Zacks Rank #1, delivered adjusted EPS of 50 cents in the first quarter of 2026, surpassing the Zacks Consensus Estimate by 14.5%. Revenues of $328.5 million topped the consensus mark by 0.29% and grew 1.4% on a year-over-year basis. Gross profit in the quarter increased 10% from the prior-year period, reflecting ongoing efficiencies realized in the delivery of care management services alongside a decrease in stock-based compensation expense.

Tenet Healthcare THC, carrying a Zacks Rank #3, delivered first-quarter 2026 earnings of $4.21, beating the Zacks Consensus Estimate by 14.39%. However, revenues of $5.37 billion slightly fell short of the consensus mark by 0.36%. Net operating revenues in Tenet’s Ambulatory Care segment increased 10.6%, driven by strong growth in consolidated same-facility net patient service revenues, acquisitions of facilities and increased service lines. Hospital revenues rose 0.6%, supported by an increase in adjusted admissions.

AUNA’s Price Performance & Valuation

Over the past year, Auna shares have dropped 26.8%, underperforming the industry, the broader Medical sector, as well as the S&P 500 Composite. Meanwhile, shares of THC and PGNY have risen 23.2% and 7.8%, respectively, in the same time frame.

AUNA One-Year Price Comparison

Image Source: Zacks Investment Research

In terms of valuation, Auna trades at a forward 12-month Price/Earnings (P/E) of 5.84X, lower than its median and industry average.

AUNA’s 1-year P/E

Image Source: Zacks Investment Research

Endnote

Auna’s first-quarter 2026 earnings are expected to continue highlighting the strength of its Peru operations, alongside persistent soft market conditions in Mexico. The risk-mitigation measures put in place in Colombia may have contributed as well. Valuation-wise, the stock is trading at a discount. However, the company’s performance over the last 12 months has trailed its peers, industry and the benchmark. We believe existing AUNA investors may find it prudent to exit their position at this stage, until there is clearer evidence of recovery in Mexico and the company reaches its medium-level leverage target.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tenet Healthcare Corporation (THC): Free Stock Analysis Report

Progyny, Inc. (PGNY): Free Stock Analysis Report

Auna S.A. (AUNA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).