Ondas Inc. ONDS will release results for the first quarter of 2026 on May 14.

ONDS’ earnings missed the Zacks Consensus Estimate in the last quarter. It has missed the estimate in three of the four trailing quarters, while beating once, with an average negative surprise of 144.77%.

Ondas Holdings Inc. Price and EPS Surprise

Ondas Holdings Inc. price-eps-surprise | Ondas Holdings Inc. Quote

Let us see how ONDS is expected to fare in terms of revenues and earnings this time.

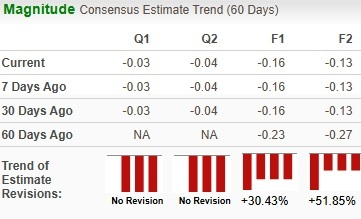

The Zacks Consensus Estimate for the first-quarter 2026 bottom line stands at a loss of 3 cents, unchanged in the past 30 days. The same for revenues stands at $39.6 million, indicating an 831.1% jump from the year-ago actual. Management guided quarterly revenues to be between $38 million and $40 million.

Image Source: Zacks Investment Research

The company’s guidance is driven by strong business momentum, especially in its Ondas Autonomous Systems (“OAS”) division. Robust M&A activity is a key factor here.

Earnings Whispers for ONDS

Our proven model does not predict an earnings beat for Ondas this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not the case here.

ONDS currently has a Zacks Rank #5 (Strong Sell) and an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

ONDS Q1: Factors at Play

Ondas entered the first quarter with significant momentum in the OAS unit following a transformative 2025.

OAS has quickly become a comprehensive “system-of-systems” platform. The division is now a multi-domain autonomy platform spanning Intelligence, Surveillance, Reconnaissance or ISR, Counter-UAS, loitering munitions/strike systems, unmanned ground vehicles and stratospheric sensing via World View acquisition.

Through the OAS unit, the company is expanding its footprint with new defense and homeland security customers across Europe, the Middle East and the United States. Simmering geopolitical tensions and rising defense budgets are driving increased demand for solutions such as counter-UAS systems and ISR platforms. On the last earnings call, management noted increasing customer interest, RFP activity and urgency in procurement decisions.

The company executed five acquisitions alone in the first quarter of 2026 and expects these to add $230 million to 2026 revenues. Full-year revenues are expected to be at least $375 million and management expects it to be a back-half-loaded growth story.

Image Source: Zacks Investment Research

Ondas recently completed the Mistral merger, valued at $175 million. The company noted that Mistral has captured programs topping $1 billion in value. Ondas had a backlog with orders in hand of $177 million as of March 31, 2026, compared with $68.3 million at year-end 2025. The pro forma backlog is $457 million, after adjusting contracted backlog from Mistral ($264 million) and World View ($16 million).

That said, execution risks remain substantial. So many acquisitions in such a short period can create integration overload and execution risks, as achieving targets depends on timely integration and conversion of backlog into revenues. Even if a single large customer delays, reduces or cancels, revenues would decline materially.

Profitability remains concerning despite sharp revenue growth. The adjusted EBITDA losses are expected to widen in the first quarter due to higher operating expenses, including increased leadership hiring and marketing investments to support rapid growth. Ondas expects EBITDA margins to improve over the year and expects product-level profitability by the third quarter of 2026.

Image Source: Zacks Investment Research

Moreover, OAS profitability is expected by the third quarter of 2027, and more importantly, company-wide profitability only by the first quarter of 2028. Management characterizes these investments as necessary to support growth. However, this can pose a significant concern for investors as the path to profitability remains heavily dependent on flawless execution. Any delays in integration and order conversion could push the profitability timeline further out.

Though ONDS’ balance sheet provides a cushion, it also introduces dilution risk. The company has resorted to financing ($1.8 billion since mid-2025), and this has boosted the pro forma cash balance to $1.5 billion. ONDS highlights this as an advantage to scale rapidly, but frequent equity dilution can erode shareholder value.

Cash generation also remains a problem. The company used $38.7 million in operating activities for 2025 and expects cash usage to increase in the first half of 2026.

Revenues from Ondas Networks are expected to remain modest due to uncertain rail network buildout timelines.

Given the multiple tailwinds and growth opportunities, the drone space is now witnessing increasing competition. Players such as Red Cat Holdings RCAT, Kratos Defense & Security Solutions KTOS and Draganfly DPRO are also vying to capture a larger share.

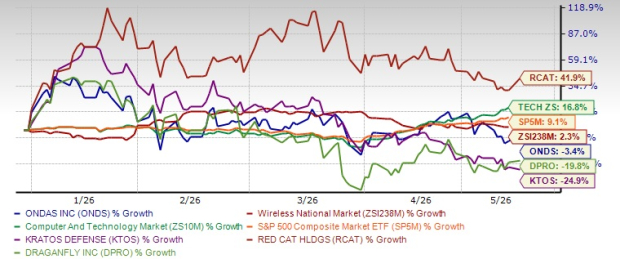

ONDS Stock Performance vs. Peers

ONDS’ shares have declined 3.4% year to date, underperforming the Wireless-National industry’s growth of 2.3%. The S&P 500 composite and the Zacks Computer and Technology sector are up 9.1% and 16.8%, respectively, in the same time frame.

Image Source: Zacks Investment Research

KTOS and DPRO have lost 24.9% and 19.8%, respectively, over the same time frame, while RCAT is up 41.9%.

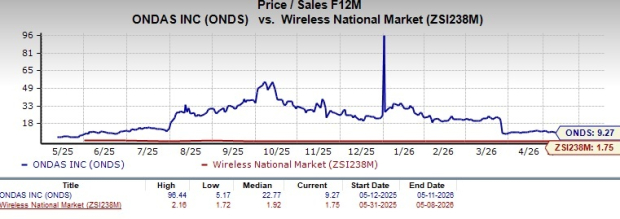

Key Valuation Metric for ONDS

ONDS stock is trading at a substantial premium, with a forward 12-month price/sales of 9.27X compared with the industry’s 1.75X.

Image Source: Zacks Investment Research

In comparison, KTOS, RCAT and DPRO trade at multiples of 5.86X, 7.32X and 1.4X, respectively.

How to Approach ONDS Before Q1 Earnings Release

Ondas’ heavy reliance on M&A, widening losses, and cash burn make the investment case risky. With profitability still years away, execution missteps and integration challenges remain significant concerns.

Its premium valuation exposes investors to sharp volatility and heightens downside risk in the near to medium-term. Until Ondas can demonstrate sustainable organic growth and make progress toward profitability, new investors need to exercise caution.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Kratos Defense & Security Solutions, Inc. (KTOS): Free Stock Analysis Report

Ondas Holdings Inc. (ONDS): Free Stock Analysis Report

Red Cat Holdings, Inc. (RCAT): Free Stock Analysis Report

Draganfly Inc. (DPRO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).