This earnings season has sparked renewed interest in artificial intelligence (AI) stocks. Two of the tech titans leading the race, Meta Platforms (META) and Alphabet (GOOGL), are spending billions to make sure they control the next phase of AI. Both companies just delivered explosive quarters fueled by AI, digital advertising, cloud computing, and massive data-center expansion. While both companies look strong today, long-term investors are likely wondering which name is better positioned to win over the next decade.

I believe one clearly has the edge. Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The Case for Meta Platforms (META)

Meta Platforms' social media empire remains incredibly powerful. AI is transforming engagement, content, ad performance, and revenue growth throughout its ecosystem. Revenue in the first quarter jumped 33% year-over-year (YOY) to $56.3 billion, with the Family of Apps (FoA) segment contributing $55 billion of revenue, also rising 33% YOY.

Management stated that a 19% growth in ad impressions and a 12% increase in average ad pricing globally drove this performance. Adjusted earnings rose 62% YOY to $10.44 per share in the quarter. The company is also seeing rapid adoption of its generative AI advertising products, with over 8 million advertisers now actively using at least one of the company’s AI-driven creative tools.

www.barchart.com

www.barchart.com The FoA segment, which serves some 3.5 billion users globally, is compensating for the weakness in the company’s Reality Labs business. This segment remains a drag financially, with revenue down 2% YOY to $402 million and an operating loss of $4 billion in Q1.

Another reason to like Meta is its valuation. Despite enormous growth, META stock currently trades at 17 times forward 2027 earnings, which is lower than many high-growth AI peers. Analysts expect Meta’s earnings to increase by 13% in 2027 to $36.19 per share.

However, the risks with Meta are also hard to ignore. Meta expects to spend as much as $125 billion to $145 billion in capital expenditures in 2026 to build AI infrastructure and data centers. Meta also disclosed a massive $107 billion increase in contractual commitments tied to infrastructure purchases and cloud agreements extending through 2027. CEO Mark Zuckerberg defended the aggressive spending, claiming that AI compute capacity could become one of its biggest long-term advantages in the technology sector. While this is true, these heavy investments could pressure profit margins in the short run, as Meta's Reality Labs segment is still a drag on its overall financials.

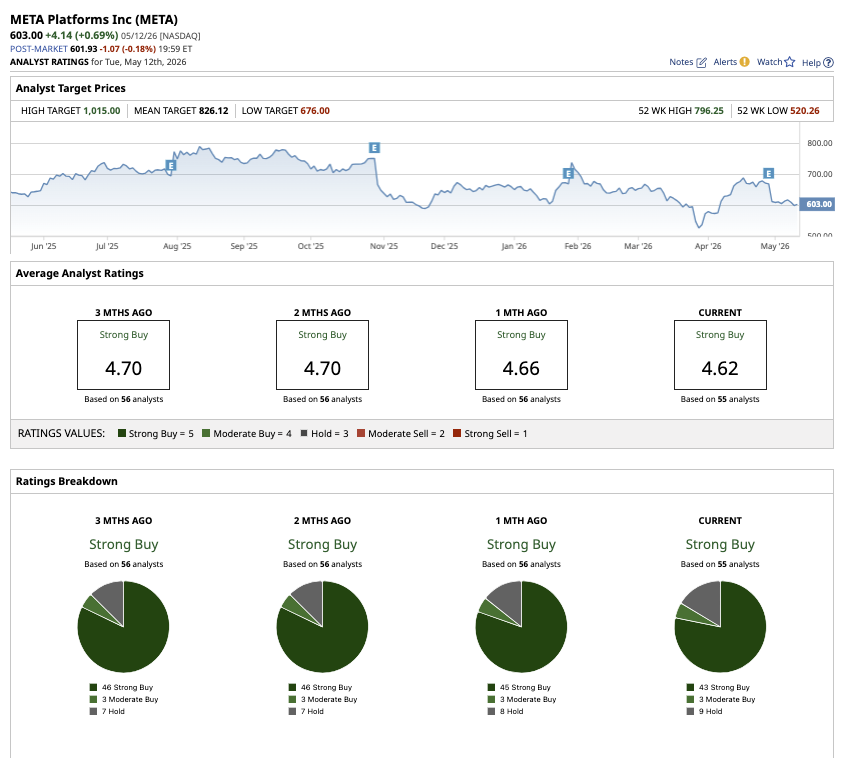

Despite a great quarter, META stock is down 6% year-to-date (YTD), underperforming the Nasdaq Composite’s ($NASX) 15% gain. On Wall Street, META has a consensus “Strong Buy” rating with an average target price of $826.12, which implies potential upside of 34% from current levels. Of the 55 analysts tracking the stock, 43 rate it as a "Strong Buy," three as a "Moderate Buy," and nine as a "Hold." The high price target of $1,015 implies that shares could climb as much as 64% from here.

www.barchart.com

www.barchart.com The Case for Google (GOOGL)

Alphabet could be entering one of the most powerful growth cycles the company has seen in years. From Search and YouTube to Cloud and Gemini, the company’s AI products are driving higher engagement, stronger monetization, and explosive infrastructure demand.

GOOGL stock has climbed 28% YTD, outperforming the tech-heavy Nasdaq Composite.

www.barchart.com

www.barchart.com In Q1, Alphabet’s revenue climbed 22% YOY to $109.9 billion. Alphabet also maintained its streak with 11-straight quarters of double-digit revenue growth. Even more impressive was the 82% growth in earnings to $5.11 per share. AI appears to be strengthening the company's most dominating business, Google Search, rather than disrupting it. Search & Other revenue climbed 19% YOY to $60.4 billion, owing mainly to retail and financial-services advertising demand.

The Gemini ecosystem is expanding rapidly across consumer products, enterprise software, developer tools, and cloud infrastructure. Notably, Gemini Enterprise paid monthly active users grew 40% quarter-over-quarter, while overall paid subscriptions across Google reached 350 million. This growth was fueled by YouTube subscriptions, Google One, and rising adoption of Gemini AI plans.

Furthermore, Google Cloud revenue surged 63% to cross $20 billion for the first time. Alphabet is also strengthening its cybersecurity offerings after acquiring Wiz in March. Like most AI companies, Alphabet’s AI spending is also exploding. Capital expenditures reached $35.7 billion in Q1, with servers accounting for nearly 60% and data centers and networking equipment accounting for 40%. For the full year, capex could be around $180 billion to $190 billion, accelerating even higher in 2027.

AI infrastructure investments continue to pressure free cash flow, which came in at $10.1 billion. The company ended Q1 with $126.8 billion in cash and marketable securities alongside $77.5 billion in long-term debt. Despite the heavy AI spending, Alphabet increased its quarterly dividend by 5%. Overall, Alphabet still appears highly profitable compared to Meta because its core businesses continue generating enormous cash flow.

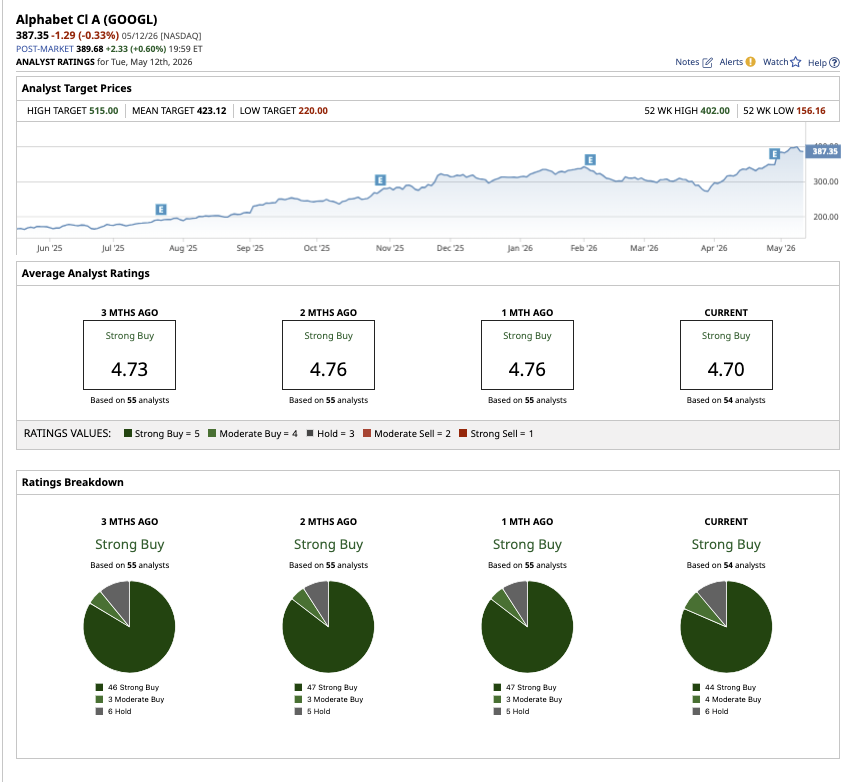

On Wall Street, GOOGL stock has a consensus “Strong Buy” rating. Of the 54 analysts tracking the stock, 44 rate it as a "Strong Buy," four as a "Moderate Buy," and six as a "Hold." The stock has an average target price of $423.12, which implies potential upside of roughly 6% from current levels The high price target of $515 implies that shares could go up as much as 28% from current levels.

www.barchart.com

www.barchart.com Which Is the Better Buy for the Next Decade?

Meta is still one of the strongest AI companies in the market, with billions of users, a proven monetization engine, and one of the most profitable advertising businesses ever built. However, if I had to pick one name for the next decade, it would be Alphabet. Search remains dominant, YouTube continues growing, Google Cloud is becoming an AI powerhouse, and Gemini gives the company a direct path into the generative AI race.

With diversification across search, cloud, AI infrastructure, subscriptions, and video, GOOGL stock appears to be the more balanced investment for the next decade.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.