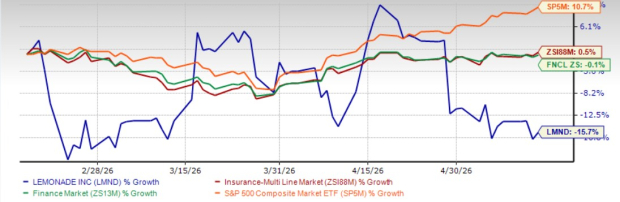

Shares of Lemonade LMND have lost 15.9% in the past three months, underperforming the industry, the Finance sector and the Zacks S&P 500 composite.

Lemonade offers renters, homeowners, pet, car and life insurance, backed by artificial intelligence and behavioral economics. It operates through full-stack insurance carriers in the United States, the United Kingdom and Europe.

Its peer Root Inc. ROOT, a provider of automobile and renters insurance products, envisions being the largest and most profitable personal lines insurance carrier in the United States. It has lost 5.1% in the past three months. Another of LMND’s peers, EverQuote Inc. EVER, an online insurance marketplace, has gained 17.9% in the same time frame.

LMND vs. Industry, Sector & S&P 500 in 3 Months

Image Source: Zacks Investment Research

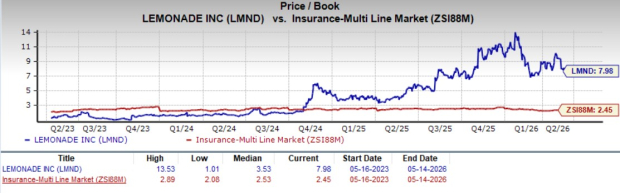

Are LMND Shares Expensive?

LMND shares are trading at a premium to the industry. Its price-to-book value of 7.98X is higher than the industry average of 2.45X and the median of 3.53X over the last three years.

Image Source: Zacks Investment Research

LMND is expensive when compared with Root and EverQuote.

Mixed Analyst Sentiment for LMND

The Zacks Consensus Estimate for LMND 2026 earnings has witnessed northbound movement in the past 30 days, while that for 2027 earnings has moved south in the same time.

Image Source: Zacks Investment Research

The consensus estimate for EVER’s 2026 and 2027 earnings has moved north in the past 30 days. Estimates for ROOT’s 2026 and 2027 earnings has witnessed no movement in the past 30 days.

Growth Estimates for LMND

The Zacks Consensus Estimate for the company’s 2026 and 2027 earnings indicates a 25.5% and 54.7% year-over-year decline, respectively. The consensus estimates for 2026 and 2027 revenues suggest year-over-year improvements. LMND has a Growth Score of A.

Factors in Favor of LMND

Lemonade is a technology-driven insurer that uses data analytics, artificial intelligence and automation to improve efficiency and create a scalable, low-cost operating model. Originally focused on renters and homeowners insurance, the company has expanded into auto, pet and life insurance, supported partly by its acquisition of Metromile. This diversification has broadened revenue sources and reduced reliance on a single business line.

Its multi-product strategy enhances customer lifetime value through cross-selling opportunities while supporting a recurring, subscription-like revenue model. Strong customer retention and engagement continue to fuel growth, with management forecasting 32% revenue growth for the second quarter and 33% for full-year 2026. The auto insurance segment has been particularly strong, with further acceleration expected from expansion into additional states and increased brand investments.

Lemonade’s in-force premium (IFP) reached $1.33 billion in the first quarter, marking the 10th straight quarter of accelerating growth. This momentum reflects the growing contribution of its AI- and automation-driven platform, which enables efficient scaling. Management has outlined a long-term goal of increasing IFP to $10 billion.

A major strength of the business is its reinsurance strategy, which shifts a substantial portion of claims risk to partners, helping stabilize earnings and reduce volatility. At the same time, Lemonade continues investing in proprietary AI systems such as AI Maya and AI Jim to streamline underwriting and claims processing, contributing to improved efficiency and a relatively low loss adjustment expense ratio.

Although profitability remains a challenge, margins are improving, free cash flow has turned positive, and management expects EBITDA profitability by the fourth quarter of 2026.

Parting Thoughts on LMND Stock

Lemonade is focused on expanding its business through strategic acquisitions and by focusing on its car insurance segment, which management views as a major future growth driver. In addition to strengthening its presence in renters, homeowners, pet and life insurance, the company continues to diversify its offerings and broaden its market reach.

By leveraging technology, automation and artificial intelligence, Lemonade aims to improve operational efficiency, strengthen its competitive position and scale its business more effectively. The company has also established ambitious in-force premium growth targets, reflecting its long-term objective of achieving tenfold expansion.

However, given a premium valuation and persisting earnings pressure, it is wise to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) insurer. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EverQuote, Inc. (EVER): Free Stock Analysis Report

Lemonade, Inc. (LMND): Free Stock Analysis Report

Root, Inc. (ROOT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).