Operating breakeven still appears some distance away for Navitas Semiconductor NVTS, but the company seems to be moving in the right direction as its AI infrastructure business begins scaling and restructuring efforts stabilize the cost base.

Navitas generated $8.6 million in first-quarter 2026 revenues, up from $7.3 million in the fourth quarter of 2025 due to stronger demand in higher-power applications such as AI data centers, grid and energy infrastructure, performance computing and industrial electrification. The company expects second-quarter revenues of roughly $10 million at the midpoint, implying more than 16% sequential growth.

While the revenue base remains relatively small, improving growth and stable operating expenses can gradually narrow losses over time.

Gross margin trends were encouraging. Adjusted gross margin improved to 39% in the first quarter from 38.7% in the prior quarter, and the company expects another modest improvement in the second quarter. At the same time, adjusted operating expenses are expected to remain roughly flat sequentially at around $14.5 million-$15.5 million.

Cost discipline matters because Navitas suggested quarterly revenues in the high-$30 million range could support operating profitability under its current gross margin and expense structure. The company remains well below that level today, but the gap could narrow if AI infrastructure demand continues accelerating over the next several quarters.

Much of the company’s future growth thesis now depends on AI infrastructure. In the first quarter of 2026, AI infrastructure revenues, including AI data centers and grid infrastructure, grew 50% sequentially from the fourth quarter of 2025. Navitas believes AI data centers could represent a $1.4-$2.5 billion market opportunity by 2030, while energy and grid infrastructure could add another $1-$1.8 billion opportunity.

The company has shifted away from lower-growth consumer markets toward higher-value GaN and silicon carbide products used in AI power systems, grid modernization and industrial applications. If revenue growth continues improving while operating expenses remain controlled, Navitas could gradually move closer toward operating breakeven over the next few years, even if meaningful net profitability still appears some distance away today.

Peer Check: How Are ON & IFNNY Faring?

ON Semiconductor ON reported first-quarter 2026 AI data center revenue growth of more than 30% sequentially and more than double year over year, while adjusted gross margin expanded for a third consecutive quarter to 38.5%. ON Semiconductor expects AI data center revenues to double in 2026. For the second quarter of 2026, ON Semiconductor guided revenues of $1.53-$1.63 billion. The company expects adjusted gross margin at 38-40%.

Infineon Technologies’ IFNNY overall revenues grew 4% sequentially in the second quarter of fiscal 2026. However, adjusted gross margin was down two percentage points sequentially to 41%. It expects revenues to reach roughly €4.1 billion in third quarter of fiscal 2026. Infineon raised its full-year 2026 guidance as demand for AI data center power supply solutions strengthened further. Infineon forecasts the adjusted gross margin to lie in the low-to-mid forties percent range.

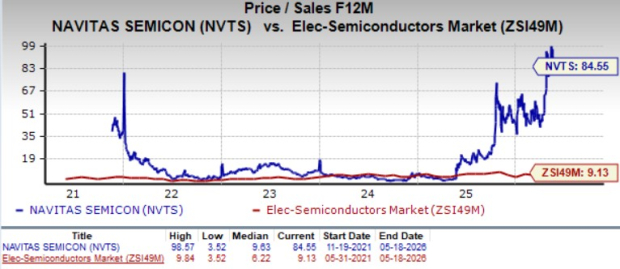

NVTS' Price Performance, Valuation & Estimates

Shares of Navitas Semiconductor have surged more than 170% year to date compared with the industry’s growth of 37%.

From a valuation standpoint, Navitas Semiconductor trades at a forward price-to-sales ratio of 84.55X, significantly higher than the industry’s average of 9.13X.

The Zacks Consensus Estimate for Navitas’ 2026 and 2027 bottom line is pegged at a loss of 17 cents per share and 15 cents per share, respectively. See how the loss estimates have been revised over the past 90 days.

Navitas currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Infineon Technologies AG (IFNNY): Free Stock Analysis Report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

Navitas Semiconductor Corporation (NVTS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).