For much of the past year, investors worried that generative artificial intelligence (AI) would disrupt the traditional enterprise software model. But Wall Street is beginning to rethink that narrative when it comes to ServiceNow (NOW). Increasingly, analysts see the company not as a casualty of the AI era, but as one of its biggest infrastructure winners.

That shift in sentiment became more visible this week after Bank of America resumed coverage of ServiceNow with a “Buy” rating and a price target of $130.00, arguing that the company is uniquely positioned to benefit from the rise of agentic AI with autonomous AI systems capable of executing tasks, making decisions, and orchestrating workflows across enterprises.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The bullish thesis centers on the idea that as companies deploy more AI agents across IT, customer service, HR, and cybersecurity operations, they will need a centralized platform to govern permissions, approvals, compliance, orchestration, and auditability. Analysts believe ServiceNow already occupies that strategic control layer inside many enterprises, giving it a potentially critical role in the next wave of AI adoption.

Bank of America’s analysts specifically highlighted ServiceNow’s workflow entrenchment, AI Control Tower initiatives, and recent security-focused acquisitions as reasons the company could emerge as a long-term beneficiary of autonomous enterprise software.

After suffering a sharp selloff earlier this year amid fears that AI could disrupt enterprise software, ServiceNow stock is now increasingly being viewed through a different lens not merely as a SaaS company, but as an important player in the agentic AI era.

About ServiceNow Stock

ServiceNow is a leading enterprise software company that provides a cloud-based platform for automating and managing digital workflows across IT service management, customer service, HR, security, and other business functions. The company is headquartered in Santa Clara, California and has a market cap of $105 billion, reflecting its position as one of the most valuable enterprise software providers globally with strong recurring revenue and broad adoption among large organizations.

Shares of ServiceNow have experienced a dramatic reversal over the past year, reflecting both Wall Street’s anxiety around AI disruption and the market’s growing optimism that the company could actually become a major beneficiary of the agentic AI era.

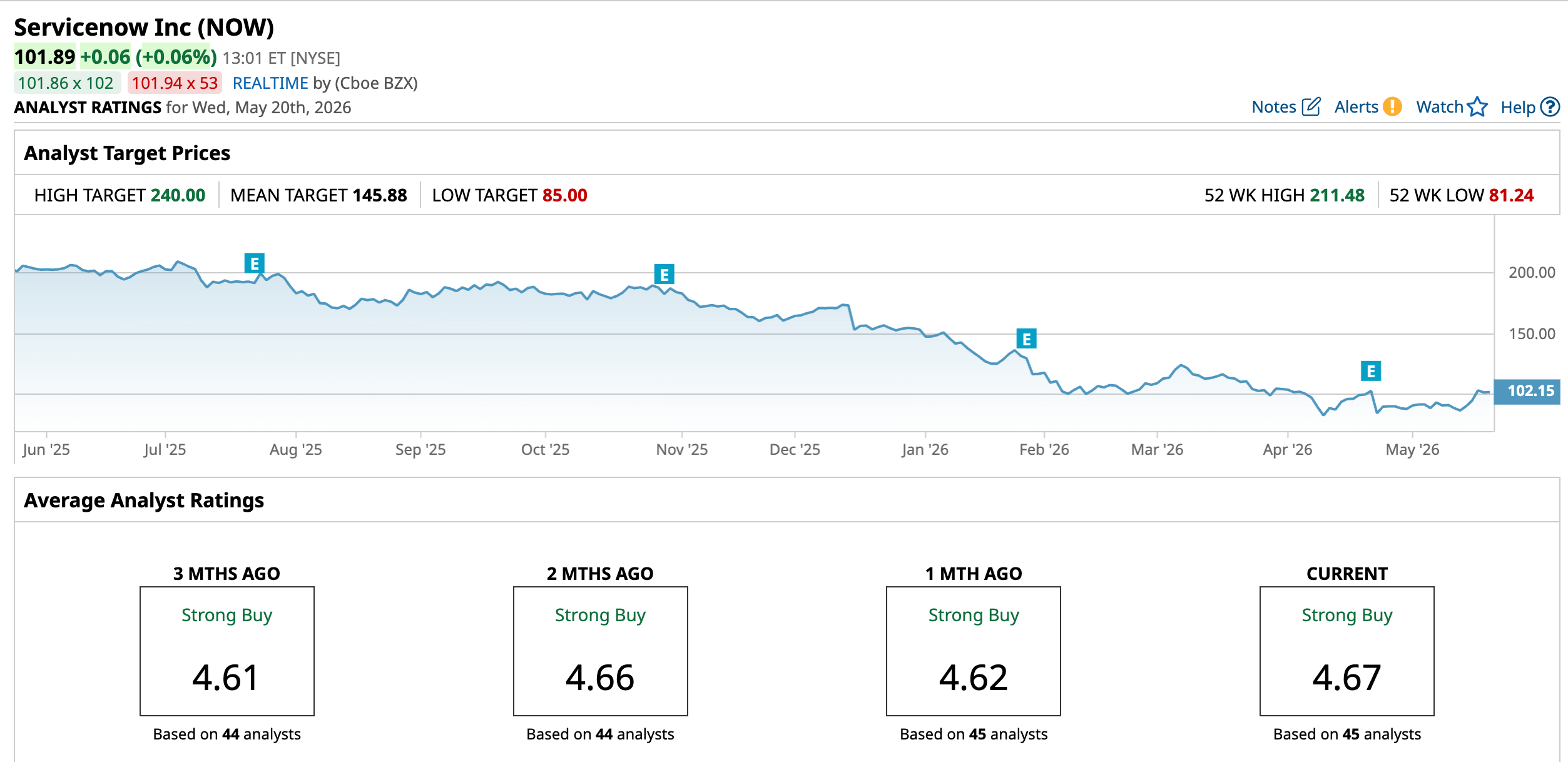

The stock remains deeply below its prior highs, with shares down 50.25% over the past 52 weeks and about 33.63% year-to-date (YTD) after a brutal selloff across enterprise software names earlier this year.

Much of that weakness was driven by investor fears that autonomous AI agents could disrupt the traditional SaaS model, pressuring premium software valuations across the sector. ServiceNow became one of the biggest casualties of that narrative, with the stock falling 51.9% from a 52-week high of $211.48 reached last year.

However, sentiment has begun shifting sharply in recent sessions. Over the past five days, ServiceNow shares have surged 16.79%, fueled by renewed optimism surrounding its positioning in enterprise AI orchestration.

The rally accelerated after Bank of America reinstated coverage, arguing that ServiceNow could emerge as a critical control layer for managing AI agents across large organizations. That bullish call triggered one of the stock’s strongest single-day performances, with shares jumping 8.8% on May 18, which was followed by a modest pullback in the next session.

www.barchart.com

www.barchart.com The stock is trading at 43.93 times forward earnings, which is higher than the sector median but below its own historical average.

Steady Q1 Results

ServiceNow reported first-quarter 2026 earnings on April 22. For Q1 2026, subscription revenue increased 22% year-over-year (YOY) to $3.7 billion, while total revenue also rose 22% to $3.8 billion.

Current remaining performance obligations (cRPO), a key forward-looking indicator of contracted revenue expected over the next 12 months, climbed 22.5% YOY to $12.6 billion. Remaining performance obligations (RPO) increased 25% YOY to $27.7 billion, reflecting continued strong enterprise spending commitments on the platform.

Also, the company posted strong customer expansion metrics. ServiceNow reported 16 transactions above $5 million in net new annual contract value during the quarter, representing nearly 80% YOY growth. The number of customers generating more than $5 million in annual contract value rose 22% YOY to 630. Meanwhile, Now Assist customers spending more than $1 million annually grew over 130% YOY, highlighting rapid enterprise adoption of ServiceNow’s AI products.

Moreover, non-GAAP operating margin expanded to 32%, while non-GAAP subscription gross margin was 81.5%. Non-GAAP net income rose to around $1 billion, and non-GAAP EPS increased to $0.97 from $0.81 in the prior-year quarter.

Management highlighted that ServiceNow’s role as an “AI control tower” is becoming increasingly central as enterprises deploy autonomous AI agents across IT, cybersecurity, HR, and customer service operations. The company also emphasized strong momentum from workflow orchestration, security offerings, data fabric capabilities, and optimism around recent acquisitions, including Armis.

Meanwhile, ServiceNow’s Q2 2026 guidance called for subscription revenue of $3.815 billion to $3.820 billion, representing 22.5% YOY growth, alongside projected cRPO growth of 19%. Management said the recently completed Armis acquisition would contribute about 125 basis points to subscription revenue growth in both Q2 and full-year 2026.

Despite stable performance, shares plunged sharply as investors focused on geopolitical deal delays in the Middle East, softer near-term cRPO expectations, and concerns surrounding acquisition-related margin pressure.

Analysts tracking NOW project the company’s EPS to rise 19.9% YOY to $2.35 in fiscal 2026 and grow 28.5% to $3.02 in fiscal 2027.

What Do Analysts Expect for ServiceNow Stock?

In addition to BofA Securities showing confidence, Cantor Fitzgerald has reiterated its “Overweight” rating and $122 price target on ServiceNow this month, amid strengthening confidence in ServiceNow’s role as the governance and orchestration layer for the emerging agentic AI enterprise.

ServiceNow received another bullish endorsement from Truist Securities, which reiterated its “Buy” rating and $120 price target.

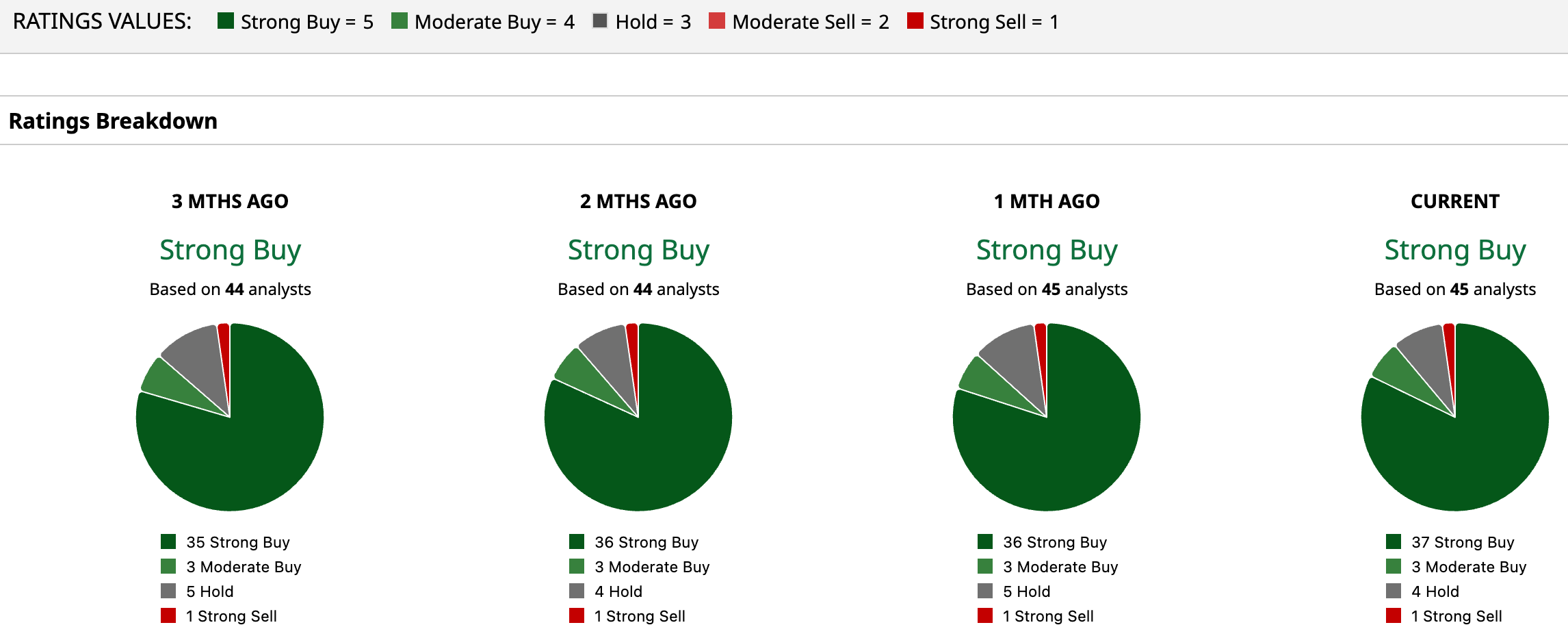

NOW has a consensus rating of a “Strong Buy” overall. Of the 45 analysts covering the stock, 37 advise a “Strong Buy,” three suggest a “Moderate Buy,” four analysts give it a “Hold” rating and one “Strong Sell.”

While NOW’s average price target of $145.88 suggests an upside of 43.2%, the Street-high target of $240 signals that the stock could rise as much as 135.6% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Is Warming Up to ServiceNow Stock. That’s Because It’s Now a Bet on Agentic AI. INM Stock Alert: What to Know as InMed, Mentari Announce Merger The $2.6 Billion Power Play: How Akamai Is Weaponizing Debt to Build the AI Edge Up 153% YTD, Here's Why Micron Stock Is Already My 2026 Winner