Ralph Lauren Corporation RL used its fourth-quarter fiscal 2026 earnings call to stress that the story is less about one strong quarter and more about a diversified growth model that management believes is holding up across regions, channels and categories.

The company beat the Zacks Consensus Estimate for both adjusted earnings and revenues, but the bigger message from management was confidence in fiscal 2027 growth and margin expansion despite a volatile macro backdrop.

RL Focuses on Diversification

President and CEO Patrice Louvet said the company’s first year under its Next Great Chapter: Drive plan outperformed because growth came from multiple sources rather than a single product, market or temporary tailwind. He pointed to brand momentum, broad product breadth and stronger consumer engagement across generations.

That framing matters because management repeatedly returned to durability. Louvet said that the company is still seeing resilient core consumers in North America, Europe and Asia, even as it remains mindful of macro volatility.

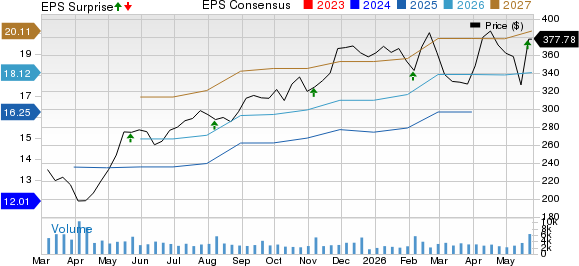

The financial backdrop supported that message. Adjusted fourth-quarter earnings were $2.80 per share, topping the Zacks Consensus Estimate of $2.52 by 11.11%, while revenues rose to $1.98 billion and beat the Zacks Consensus Estimate of $1.85 billion by 7.23%.

Ralph Lauren Corporation Price, Consensus and EPS Surprise

Ralph Lauren Corporation price-consensus-eps-surprise-chart | Ralph Lauren Corporation Quote

Ralph Lauren Leans on Brand & Pricing Power

Louvet highlighted sports, fashion and cultural activations as major drivers of customer recruitment, including the Winter Olympics, runway events and Lunar New Year campaigns. Management said that those efforts helped add 6.5 million direct-to-consumer customers in fiscal 2026 and pushed social followers to about 70 million.

The company also tied its margin performance to continued brand elevation. Chief financial officer Justin Picicci said that the adjusted gross margin expanded in the quarter even though management had expected contraction, helped by stronger average unit retail, favorable mix and disciplined discounting.

That pricing and mix story remains central to the fiscal 2027 setup. Picicci said AUR growth should stay positive, though at a more normalized mid-single-digit pace after a 16% increase in the fiscal fourth quarter.

RL Sees Asia Leading, Europe Facing More Caution

Geographically, Asia remained the standout. Fourth-quarter revenues in the region rose 28% in constant currency, with China growing more than 50%, supported by Lunar New Year demand, digital expansion and continued focus on key city clusters.

Europe was different in tone. While the region posted solid fourth-quarter growth, management adopted a more prudent stance for fiscal 2027 because of higher energy costs, softer sentiment and weaker tourism tied to Middle East disruption.

North America, meanwhile, was presented as firmly back on a growth path. Picicci said that better full-price selling and stronger replenishment helped offset lower-tier wholesale rationalization, and Louvet described the company’s wholesale relationships as more aligned with brand elevation than they were a few years ago.

Ralph Lauren Outlines Measured FY27 Guidance

For fiscal 2027, management guided constant-currency revenue growth of 4-5% on a 52-week comparable basis, with 40-60 basis points of operating margin expansion. The company also expects the 53rd week to add one point to revenue growth.

The fiscal first-quarter guidance was stronger, with revenues expected to rise at a mid to high-single-digit rate in constant currency and the operating margin projected to expand 80-120 basis points. Management said that the first-half margin expansion should benefit from the timing of marketing and a lower prevailing tariff rate.

In Q&A, analysts pressed on whether year-one outperformance was sustainable, how much Europe risk was embedded in the outlook and whether unit growth can finally contribute more alongside AUR. Management’s answers were steady rather than promotional, emphasizing continued investment discipline, modest expected unit growth and flexibility if demand comes in stronger than planned.

RL Leaves the Call on Offense

The clearest read-through from the call was management’s insistence that Ralph Lauren is still in investment mode, not harvest mode. Louvet and Picicci both described a company willing to keep spending on marketing, AI, digital capability and key-city expansion, while still targeting margin gains.

That posture was backed by balance-sheet commentary as well. The company ended fiscal 2026 with $2.1 billion in cash and short-term investments, returned more than $700 million to shareholders through dividends and repurchases, and raised its quarterly dividend 10%.

Ralph Lauren’s Zacks Signals

RL currently has a Zacks Rank #3 (Hold), along with a Value Score of C, Growth Score of B, Momentum Score of A and a VGM Score of B. Based on the Zacks Style Scores guidance, the strongest combinations typically pair a Zacks Rank #1 (Strong Buy) or #2 (Buy) with A or B style scores, while a Rank #3 can still support a hold stance with better grades viewed more favorably. You can see the complete list of today’s Zacks #1 Rank stocks here.

For RL, the strong Momentum Score and solid VGM and Growth grades point to favorable style characteristics, but the current Zacks Rank #3 keeps the signal balanced rather than decisive. That rank can change as earnings estimate revisions adjust after the quarter.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ralph Lauren Corporation (RL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).