Marvell Technology (MRVL) is heading into its May 27 earnings report with gaining fresh Wall Street attention.

Last week, Stifel raised its price target on Marvell to a Street-high $210 from $140, predicting a beat and raise for the upcoming quarter. Investors welcome the news and shares climbed about 3% hitting the fresh all-time high at $198 following the note on Friday. Traders are increasingly betting that the artificial intelligence infrastructure boom is still in its early stages, even after Marvell's stock has already surged triple digits year-to-date in 2026.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The company has quietly become one of the most important suppliers in the AI ecosystem. Marvell designs custom silicon, optical interconnects, and networking hardware that allow hyperscale data centers to move massive amounts of data without bottlenecks. Every major AI buildout needs faster connectivity, and that is exactly where Marvell fits in.

Stock Movement Shows Strong AI Optimism

Marvell stock’s performance tells the story clearly. Shares are up about 243% over the past year, dramatically outperforming the broader semiconductor sector and the S&P 500.

Technically, the momentum remains strong. Marvell’s 50-day simple moving average sits near $133, while the 200-day moving average rests around $101. That gap reflects the aggressive buying pressure that has followed the company throughout 2026.

Two major developments helped fuel that rally. Recently, Nvidia (NVDA) invested $2 billion into Marvell through convertible preferred stock and expanded its partnership with the company to integrate Marvell’s custom XPUs and optical connectivity products into the NVLink Fusion ecosystem. Marvell also acquired Celestial AI and XConn, strengthening its position in AI scale-up networking and optical infrastructure.

When Nvidia backs a company with a multibillion-dollar investment, Wall Street pays attention.

www.barchart.com

www.barchart.com Valuation Looks Expensive, but Growth Is Backing It Up

That performance comes with some premium. Marvell stock trades at a forward price-to-earnings ratio above 43x and an enterprise-value-to-sales multiple near 20.2x.

For comparison, the sector median EV/sales ratio is around 3.6x. That is an enormous premium, and it highlights how much future AI growth investors are already pricing into the stock.

Still, Marvell’s growth metrics help explain the valuation. Revenue expanded 42% year-over-year, far above the semiconductor sector median of roughly 11%. The company also posted a net income margin near 33%, compared with a sector median closer to 6%.

Investors are clearly willing to pay a premium for a company tied directly to AI infrastructure spending. If Marvell continues growing revenue above 30% annually, today’s valuation may eventually look justified. But if AI spending slows, the stock could face meaningful pressure given how much optimism is already built into the shares.

Latest Quarterly Results Highlight Data Center Strength

Marvell’s latest quarterly results reinforced the bullish narrative. The company reported fiscal fourth-quarter 2026 revenue of $2.2 billion on March 5, up 22% from the prior year and slightly ahead of analyst expectations.

The data center business remained the primary growth engine, generating $1.65 billion in revenue during the quarter. That accounted for roughly 74% of total company sales.

Management also highlighted strong cash generation. Cash from operations totaled $374 million during the quarter, while cash and equivalents stood at $2.64 billion at quarter end.

Guidance Suggests More AI Expansion Ahead

Looking forward, management guided first-quarter fiscal 2027 revenue to $2.4 billion, plus or minus 5%, alongside EPS between $0.74 and $0.84.

For the full fiscal year, Marvell expects revenue growth above 30%, putting annual sales close to $11 billion. The company also raised its fiscal 2028 revenue target to approximately $15 billion, signaling confidence that AI networking demand remains strong.

Wall Street analysts are modeling full-year revenue near those levels, with EPS expectations above $3 for fiscal 2027.

That outlook suggests hyperscaler AI spending is still accelerating rather than slowing down.

Analyst Opinions Remain Overwhelmingly Bullish

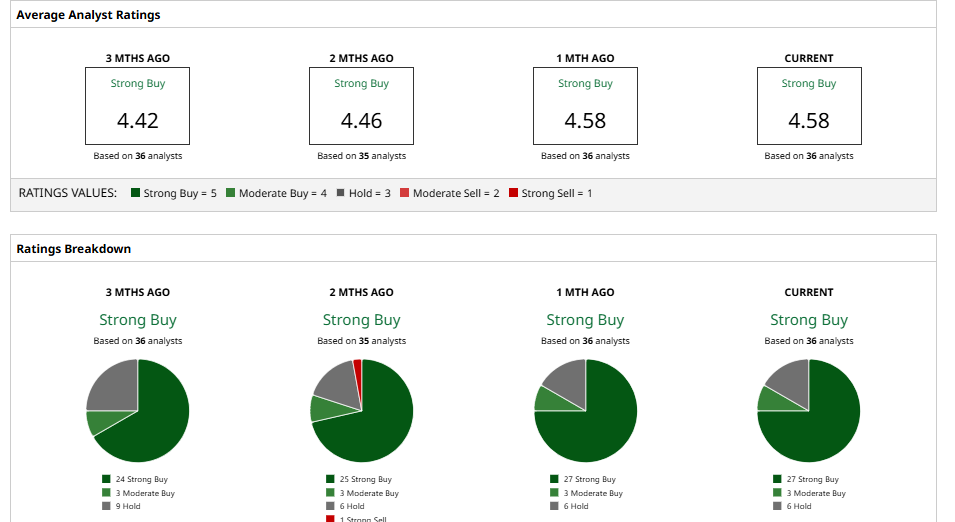

Wall Street sentiment on Marvell remains highly positive. According to Barchart data, the stock carries a “Strong Buy” consensus rating based on 36 analysts in coverage.

However, the average analyst price target sits around $150, implying downside risk of around 28% from current levels.

Separately, Stifel analyst Tore Svanberg recently raised his target to $210 from $140 and said he expects Marvell to deliver an earnings beat on May 27. He also increased his fiscal 2027 data center revenue growth forecast to more than 40%, while projecting interconnect revenue growth above 50%.

Likewise, Citi analyst Atif Malik lifted his target to $215, citing strong Trainium-related demand. Bank of America increased its target to $200 after raising its AI networking market opportunity forecast. RBC Capital Markets also moved to $200, highlighting optical connectivity momentum, while Wells Fargo raised its target to $195 on expectations for further AWS Trainium expansion.

Most bullish calls share the same core thesis. Marvell’s custom silicon pipeline is scaling faster than expected, and the Nvidia partnership gives the company added credibility with institutional investors.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Jefferies Just Upgraded Generac Stock. Here’s Why. Billionaire Dan Loeb’s Third Point Just Took a New Position in Hut 8. What This Means for HUT Stock. Wall Street Is Only Just Beginning to Recognize Advanced Micro Devices’ Agentic AI Upside Potential Why You Should Buy Marvell Technology Stock Before May 27