With a market cap of $17.8 billion, Essex Property Trust, Inc. (ESS) is a residential real estate investment trust (REIT) that owns, develops, redevelops, and manages multifamily apartment communities primarily along the U.S. West Coast. Headquartered in San Mateo, California, the company focuses on high-barrier, supply-constrained markets such as Northern California, Southern California, and the Seattle metropolitan area.

Shares of the REIT have underperformed the broader market over the past 52 weeks. ESS shares have increased 2.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 29.6%. Moreover, shares of the company are up 6% on a YTD basis, compared to SPX’s 9.8% gain.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Focusing more closely, shares of the REIT have lagged behind the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 10% return over the past 52 weeks and 10.8% YTD rise.

www.barchart.com

www.barchart.com Essex Property’s shares popped 4.3% after the company announced its FY2026 Q1 earnings. Its core FFO per share rose 2.3% year over year to $4.06, beating analyst expectations of $3.96. Total revenue increased 4.3% to $484.87 million, also topping consensus estimates. Operationally, same-property revenue grew 2.9% year over year, while same-property NOI climbed 4.1%, reflecting healthy leasing trends and effective expense management.

Looking ahead, management reaffirmed its full-year 2026 guidance, projecting core FFO in the range of $15.69 to $16.19 per share. The company also expects same-property revenue growth of 1.7% to 3.1% and NOI growth of 0.8% to 3.4% for the year.

For the fiscal year ending in December 2026, analysts expect Essex Property Trust’s core FFO to grow marginally year-over-year to $16.06 per share. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

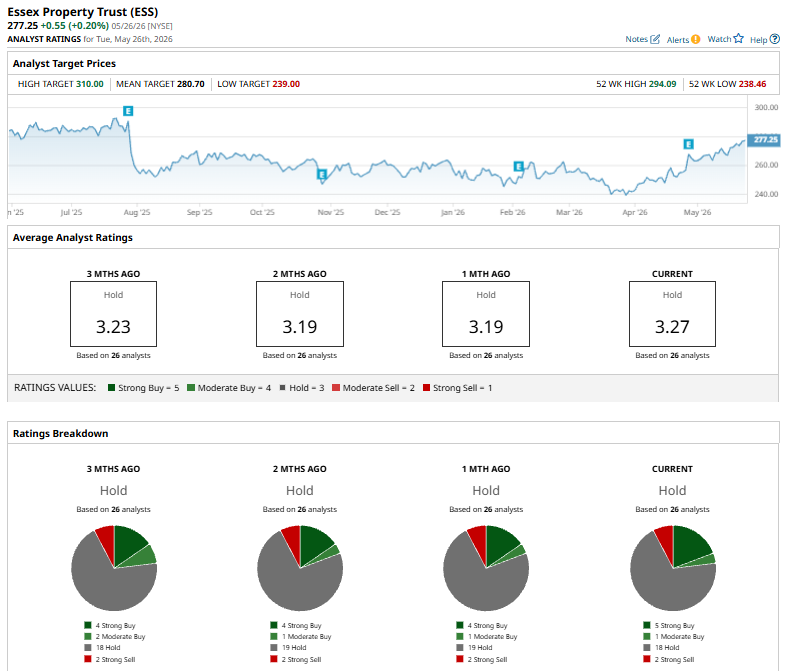

Among the 26 analysts covering the stock, the consensus rating is a “Hold.” That’s based on five “Strong Buy” ratings, one “Moderate Buy,” 18 “Holds,” and two “Strong Sells.”

www.barchart.com

www.barchart.com The configuration is bullish than a month ago when the stock had four “Strong Buy” suggestions.

On May 18, Anthony Paolone raised the price target on Essex Property to $275 from $272 while maintaining an “Underweight” rating on the stock. Separately, Scotiabank increased its price target to $282 from $278 and reiterated an “Outperform” rating, citing Essex as one of its preferred multifamily REITs due to its strong exposure to Northern California apartment markets despite expectations for a slower recovery across oversupplied Sunbelt markets.

The mean price target of $280.70 represents a premium of 1.2% to ESS’s current levels. The Street-high price target of $310 implies a potential upside of 11.8% from the current price.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Broadcom’s AI Revenue Is Taking Off. Back Up the Truck on AVGO Stock Now. With Analysts Calling for Western Digital to Double Earnings, the WDC Stock Rally Isn’t Over Yet 2 Top AI Stocks I’d Buy Now and Hold for the Next Decade Why Traders Are Watching Bull Call Spreads on GOOGL