Myriad Genetics, Inc. MYGN entered 2026 with a strategy centered on its Cancer Care Continuum and a busy oncology launch schedule. The first quarter showed progress, even with stable total testing volumes.

The next test is whether a stronger second half can offset rising commercial spend and deliver on guidance.

MYGN’s Cancer Care Continuum Is Gaining Momentum

In the first quarter of 2026, Cancer Care Continuum volumes rose 13% year over year, while total testing volumes held steady. That mix supported 2% year-over-year revenue growth. The Cancer Care Continuum segment produced $120.2 million of revenue, up 4% year over year.

Myriad Genetics’ Hereditary Cancer Demand Supports Core Sales

MyRisk demand remained broad-based, with volumes up 10% in the affected population and 16% in the unaffected population versus the year-ago quarter.

The company is leaning on a dedicated hereditary cancer sales force and workflow programs, alongside menu expansion. MyRisk now spans 63 genes across more than 11 cancer types, and disease-specific panels were added in the first quarter.

MYGN’s 2026 Launch Calendar Adds New Revenue Levers

Precise minimal residual disease testing moved into early commercialization with a limited March 2026 launch for select breast cancer customers, supported by positive early feedback on the ultrasensitive assay. Management expected to launch the AI-enhanced Prolaris test in June 2026, and the company later announced the Prolaris + AI Test launch. Menu refreshes are designed to reduce provider friction and improve clinical utility.

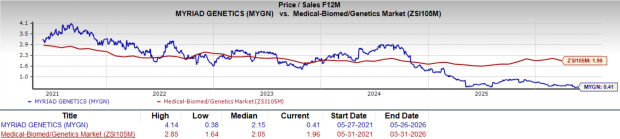

In terms of valuation, MYGN shares are trading at a forward, five-year Price/Sales (P/S) of 0.41X, lower than its median and the industry average.

Image Source: Zacks Investment Research

Myriad Genetics’ Tumor Profiling Gets a Regulatory Lift

MyChoice CDx received Food and Drug Administration approval as a companion diagnostic for Zejula in advanced ovarian cancer. The approval adds momentum to tumor profiling as MYGN competes on menu breadth and practice support.

MYGN’s GeneSight Reimbursement Improves Near-Term Setup

GeneSight volumes increased 7% year over year in the first quarter, and ordering clinicians exceeded 39,000. Revenues rose 24% to $38.3 million on improved reimbursement, with management citing better payer coverage tied to biomarker legislation and revenue cycle optimization. Coverage decisions remain a swing factor that can change access and pricing.

Myriad Genetics’ Prenatal Headwinds Still Matter in 2026

Prenatal volumes declined 12% year over year in the first quarter and revenue fell 15% to $41.9 million. The business is reactivating accounts after a disruption linked to the 2025 second-quarter order management system rollout. FirstGene is targeted for a full commercial launch in the second half of 2026, with results delivered within 14 days.

MYGN’s 2026 Outlook Balances Upside and Execution Risk

MYGN reaffirmed 2026 revenue guidance of $860 million to $880 million and adjusted EBITDA guidance of $37 million to $49 million, with second-half revenue expected to exceed first-half levels. The stakes are higher because investment is rising. The company is expanding the sales organization by more than 100 account executives and expects gross margins to fluctuate by quarter based on mix and pricing trends.

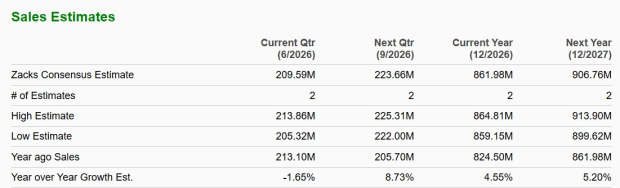

The Zacks Consensus Estimate projects the company’s revenues to increase 4.6% in 2026, followed by a 5.2% growth in 2027.

Image Source: Zacks Investment Research

Competitive pricing and shifting payer coverage can pressure average revenue per test, even if volumes hold. Management also flagged foreign-exchange sensitivity given international operations, and noted that the minimal residual disease landscape is still forming as payer expectations and community oncology workflows evolve.

Liquidity remains a support, with $124.4 million in cash and $120.3 million of long-term debt exiting the first quarter, plus access to $199 million in capital.

MYGN currently carries a Zacks Rank #2 (Buy). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Within the broader industry, ACADIA Pharmaceuticals Inc. ACAD focuses on medicines for neurological and rare diseases, while Halozyme Therapeutics, Inc. HALO centers on drug-delivery technologies aimed at improving the patient experience.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Myriad Genetics, Inc. (MYGN): Free Stock Analysis Report

Halozyme Therapeutics, Inc. (HALO): Free Stock Analysis Report

ACADIA Pharmaceuticals Inc. (ACAD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).