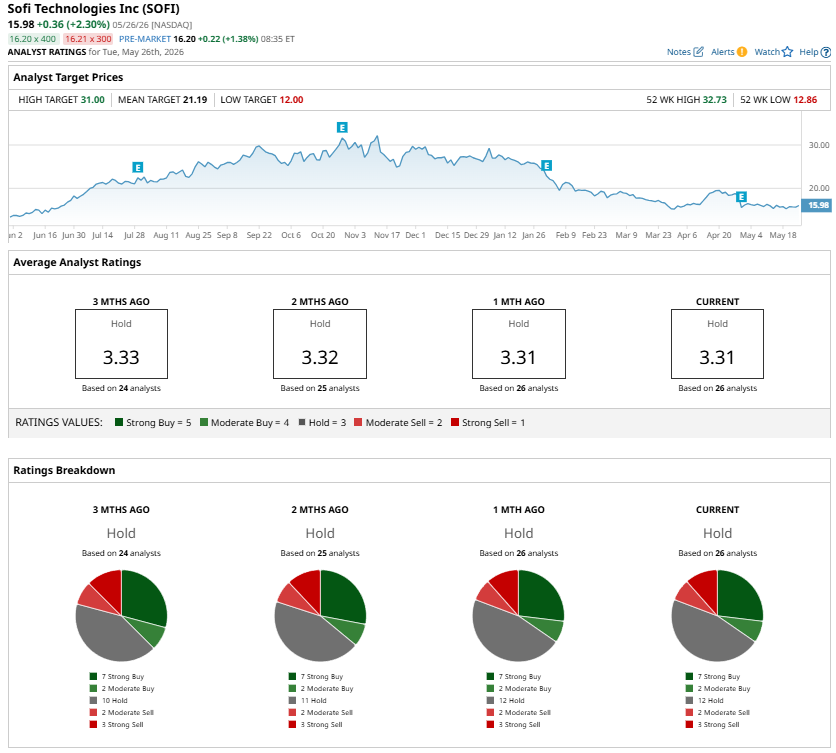

Shares of SoFi (SOFI) have fallen sharply, trading more than 50% below their 52-week high of $32.73. The steep decline reflects investor concerns around valuation and slowing momentum in some of the company’s capital-light revenue streams. However, despite the recent sell-off, SoFi’s business fundamentals remain strong, and the correction presents an attractive opportunity to buy the dip.

Notably, the market’s reaction has largely been driven by weakness in SoFi’s fee-based, capital-light businesses, which have become an increasingly important part of the company’s growth story. These businesses help diversify revenue, reduce exposure to credit risk, and support higher valuation multiples. As growth in those segments moderated, investor sentiment turned cautious.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Still, the slowdown does not appear to undermine the company’s overall trajectory. Management had already stated that its technology platform business would face temporary pressure after a major client fully transitioned off the platform before year-end. Even with that headwind, SoFi continued to post strong operating results and expand across key growth metrics.

www.barchart.com

www.barchart.com SoFi’s Revenue Growth Continues to Accelerate

Despite the headwind, SoFi delivered an impressive first-quarter performance, highlighted by accelerating revenue growth and strong customer engagement. Adjusted net revenue climbed 41% year-over-year in Q1, up from 37% growth registered in Q4 of 2025.

About $690 million came from net interest income, while nearly $390 million was generated from interchange fees, brokerage fees, technology and loan platform fees, loan origination fees, and other fee-based activities. This demonstrates that SoFi is steadily building a more diversified revenue model beyond traditional lending.

Despite concerns about the technology platform business, total fee-based revenue across the company rose 23% year-over-year to $387 million in the first quarter, indicating that demand across its ecosystem remains healthy.

Member and Product Growth Remain Exceptional

One of SoFi’s biggest strengths is its rapidly growing user base while deepening engagement with existing customers.

During the first quarter, the company added a record 1.1 million new members, bringing total membership to 14.7 million, up 35% from the previous year. Product adoption was equally impressive, with SoFi adding a record 1.8 million new products during the quarter. Total products reached 22.2 million, up 39% year-over-year.

The company is also seeing stronger cross-selling trends. About 43% of new products were opened by existing members, up from 40% in the previous quarter and 36% in the same period last year. This indicates that customers are increasingly using multiple SoFi services, which can improve retention and long-term profitability.

SoFi’s Loan Platform Business Sustains Momentum

One of SoFi’s strengths is the flexibility of its loan platform business (LPB). The company can either hold loans on its balance sheet to generate long-term interest income or distribute loans through its platform business to produce capital-light fee revenue without taking on credit risk or loss-sharing obligations.

Notably, the business continues gaining traction. During the quarter, SoFi secured $3.6 billion in new commitments from three major partners, highlighting strong demand for the platform and adding another potential source of high-margin fee revenue.

Lending Business Remains Solid

SoFi’s lending segment also remained robust in the first quarter, with record originations across multiple categories.

Personal loan originations reached an all-time high of $8.3 billion as the company continued gaining market share. Student loan originations surged to $2.6 billion, more than doubling from the prior year. Meanwhile, home loan originations totaled $1.2 billion, nearly 2.4 times the same quarter last year.

These results suggest that SoFi is successfully expanding its presence across key lending categories while benefiting from strong consumer demand.

Deposits Provide a Competitive Advantage

Another major strength is SoFi’s rapidly growing deposit base. Total deposits increased by $2.7 billion during the quarter to reach $40.2 billion. A larger deposit base gives SoFi access to lower-cost funding, which can improve profitability over time.

The Bottom Line

The recent selloff in SoFi reflects investor concerns about slowing growth in certain fee-based businesses, but the company’s broader operating performance remains solid. Revenue growth is accelerating, membership continues to surge, lending activity remains strong, and deposits are expanding rapidly.

While analysts maintain a “Hold” consensus rating on SoFi, the sharp decline represents a compelling opportunity to accumulate shares at a significantly discounted valuation.

www.barchart.com

www.barchart.com On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SoFi Stock Is Down 51% from Its Highs. Don’t Miss this Chance to Buy the Dip. This One Decision Could Make or Break Apple Stock The Under-the-Radar AI Semiconductor Play You Shouldn’t Ignore Bank of America Says Nvidia Is Still the Top AI Compute Stock to Buy Despite YTD Underperformance. Here’s Why.