Salesforce, Inc. CRM used its first-quarter fiscal 2027 call to press a forward-looking case centered on Agentforce, Slack and a new Headless 360 strategy, while also defending confidence in a stronger second half.

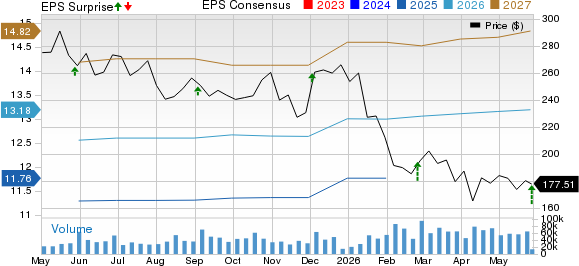

The quarter itself was solid, with non-GAAP earnings of $3.88 per share beating the Zacks Consensus Estimate of $3.12 by 24.36% and revenues of $11.13 billion edging past the consensus $11.06 billion estimate by 0.68%. Still, management spent more time on monetization paths, bookings signals and guidance assumptions than on the reported beat alone.

Salesforce, Inc. Price, Consensus and EPS Surprise

Salesforce, Inc. price-consensus-eps-surprise-chart | Salesforce, Inc. Quote

CRM Pushes Agentforce Deeper

Chair and chief executive officer Marc Benioff framed agentic AI as Salesforce’s biggest growth opportunity and said the company is embedding Agentforce across Customer 360, not treating it as a stand-alone add-on. He pointed to $1.2 billion in Agentforce ARR, more than 28.6 trillion tokens processed to date and 3.8 billion Agentic Work Units delivered.

That message was reinforced in the company’s new disclosure framework. In the press release, Salesforce recast subscription and support revenues into Agentforce Apps and Data 360, Headless Platform & Other, underscoring how management now wants investors to view AI as integrated into the core portfolio.

Management also tied AI adoption to broader platform expansion. President, chief revenue officer Miguel Milano said bookings for premium sales and service packages tied to agentic capabilities grew nearly 60% year over year, while Robin Washington said the top 10 customers by Agentic Work Unit usage increased total Salesforce spending by 1.5 times over the past year.

Salesforce Raises Bar on H2

President, chief operating and financial officer Robin Washington raised the midpoint of full-year fiscal 2027 revenue guidance to a range of $45.9 billion to $46.2 billion, while introducing second-quarter revenue guidance of $11.27 billion to $11.35 billion. She also maintained the non-GAAP operating margin target at 34.3%.

Washington’s more important signal was the setup for the back half. She said first-half net new annual order value (AOV) growth should outpace AOV growth and support organic revenue reacceleration in the second half of fiscal 2027.

At the same time, she was explicit about offsets. The full-year guide still assumes momentum in Agentforce, Data 360 and Slack, but also ongoing weakness in Marketing and Commerce, softer Tableau bookings and renewals, and more license revenue volatility from Informatica’s on-premise business.

CRM Uses Q&A to Defend Growth

A Morgan Stanley analyst pressed management on why confidence in second-half acceleration remains high despite CRPO landing in line with guidance and persistent pressure in Tableau and Commerce. That exchange produced some of the clearest call commentary.

Washington argued investors should focus less on CRPO in isolation and more on the combination of stronger net new AOV, a growing consumption motion and improving bookings mix. She added that renewal timing can distort CRPO’s relationship to revenues.

Milano went further, saying six of the top 10 deals in the quarter were broader enterprise agreements bundled with Flex Credits, while seven of the top 10 added seats. He said that mix supports management’s confidence that monetization is broadening beyond initial AI experimentation.

Salesforce Sees Headless as New Surface

The most debated strategic topic in Q&A was Headless 360. A Goldman Sachs analyst asked whether giving customers and partners more flexible access to Salesforce data and workflows could enable value leakage or encourage more in-house development.

Benioff, chief marketing officer Patrick Stokes and president, chief engineering and customer success officer Srinivas Tallapragada all argued the opposite. Their view was that Headless expands Salesforce’s monetizable surface area by letting users access the platform inside Slack, coding tools and third-party interfaces rather than only through the traditional app layer.

Management backed that claim with early usage data, including more than 1.5 million Headless MCP tool calls and 50 million Slack MCP tool calls. Milano said customer conversations around Headless have turned notably more constructive because it lets outside agents tap Salesforce data while keeping the company at the center of the workflow.

CRM Balances AI Spend and Returns

A Deutsche Bank analyst asked how Salesforce can absorb surging token usage without visible gross margin erosion. Benioff and Washington answered that through productivity and scale rather than through a near-term margin sacrifice story.

Washington said AI coding tools helped double features and code shipped year over year while reducing defects, and Slackbot is generating 3.8 million hours of annualized employee productivity gains. That internal “Customer Zero” posture is central to management’s Rule of 50 framework for fiscal 2030.

Capital allocation stayed aggressive as well. Salesforce returned $27.5 billion to shareholders in the quarter, including a $25 billion accelerated share repurchase that reduced diluted share count by 10% year over year.

Salesforce Leaves a Clear Priorities List

The call ended with management sounding confident, but also unusually specific about what has to go right. The core priorities were clear: keep converting AI usage into broader bookings, use Slack and Headless to widen access points, and deliver the second-half revenue acceleration management has now reiterated several times.

Just as important, the pressure points were not dismissed. Tableau, Commerce, Marketing softness and Informatica-related revenue volatility all remain in the model, which made the tone of the call read more like a defended operating plan than a victory lap.

Zacks Signals on CRM

CRM carries a Zacks Rank #2 (Buy), with a Value Score of B, Growth Score of A, Momentum Score of C and a VGM Score of A, based on the data provided. In Zacks’ framework, the strongest setups tend to be stocks with a Zacks Rank #1 (Strong Buy) or 2 paired with a Style Score of A or B. A VGM Score of A or B can further strengthen the overall profile.

You can see the complete list of today’s Zacks #1 Rank stocks here.

That places CRM in a favorable part of the Zacks system, especially on growth and combined style measures. Even so, the Zacks Rank is driven first by earnings estimate revisions, so that rating can change after analysts update their models following the quarter and management’s outlook.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Salesforce, Inc. (CRM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).