Semiconductor stocks have turned into Wall Street’s favorite AI trade. From giant data centers to advanced artificial intelligence (AI) models, almost every new wave of technology now depends on powerful chips running behind the scenes. And right in the middle of that rush sits the memory market, where companies like Micron Technology (MU) play a critical role supplying the DRAM and NAND storage needed to keep AI systems running.

That massive excitement has also sparked concerns that chip stocks may have climbed too far, too fast. But not everyone on Wall Street thinks the sector has entered bubble territory. Vivek Arya, senior semiconductor analyst at Bank of America Securities, recently argued that many semiconductor companies, including memory leader Micron, are still trading below their long-term historical valuation levels despite the strong AI-driven growth story unfolding.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In his view, the sector is not overheated, but rather “extended but not expensive,” especially when compared with the pace of earnings growth being delivered. The basis of this argument is a major structural shift in the memory business, driven by AI.

The analyst explains that demand is rising four to five times faster than the industry can expand supply, and that’s a gap the memory market has rarely seen before. As AI moves beyond basic applications into reasoning models and agentic systems, the need for high-performance memory has surged sharply. This has pushed high bandwidth memory (HBM) pricing sharply higher, with strong sequential gains and tight supply conditions expected to persist.

Wall Street is bullish on Micron, and with memory demand remaining exceptionally strong while supply remains tight, investors might be wondering whether Micron has already had its run or if this AI-fueled story is only warming up. Let’s dig into more details.

About Micron Stock

Micron Technology, the semiconductor powerhouse headquartered in Boise, Idaho, operates as the only U.S.-based manufacturer of DRAM, NAND, and NOR memory technologies. Micron designs and fabricates high-performance memory and storage solutions under the Micron and Crucial brands for AI, data centers, mobile, automotive, and industrial markets. The company currently has a market cap of $1.04 trillion.

The rally in shares of Micron Technology has gone from impressive to almost unbelievable. Over the past decade, the memory-chip giant has soared more than 7,160%, surviving brutal memory downturns and coming out even stronger each time. Over the past five years alone, MU stock has climbed 1,002%, while the three-year gain stands above 1,235%.

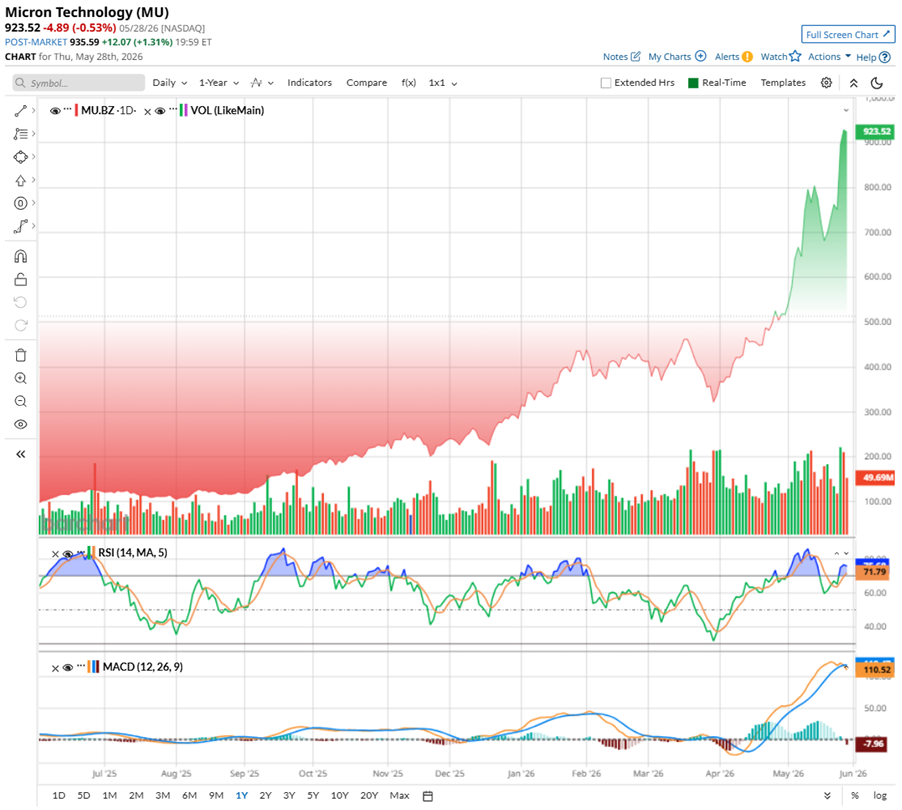

But 2026 is where things shifted into another gear. The stock ripped to a record high of $956.16 on May 27 after analysts rolled out fresh bullish price targets. At one point on May 26, the rally even pushed Micron past the $1 trillion market-cap milestone for the first time.

The stock has cooled slightly since then, slipping a mere 0.26% from its peak. Still, the bigger trend remains hard to ignore. Shares are up 894.72% over the last 52 weeks and 304.57% in just six months. Year-to-date (YTD), MU stock has surged 235.21%, making it one of 2026’s top-performing large-cap tech stocks.

The fuel behind the move is pretty clear – investors appear to be doubling down on the AI infrastructure boom. AI data centers need enormous amounts of HBM and storage, and Micron is sitting right in the middle of that demand wave. Tight global memory supply has also pushed pricing higher, helping margins and earnings expectations climb fast.

Technically, Micron’s chart is showing slight signs of exhaustion after its explosive rally. The 14-day RSI of 77.36 has moved into overbought territory, usually a signal that the stock may need time to cool off before making another big move higher. At the same time, trading volume has recently turned weaker, while the MACD indicator has flashed a bearish crossover with red histogram bars appearing. Together, those signals suggest momentum is slowing in the short term, even though the broader bullish trend still remains firmly in place.

www.barchart.com

www.barchart.com Valuation-wise, MU stock may look a little pricey, trading at 43.63 times trailing earnings. But Wall Street is not really looking in the rearview mirror anymore. On a forward basis, the stock trades at 16.06 times adjusted earnings, still below many sector peers and its historical average. That’s why plenty of analysts still see value here. AI demand is lifting margins, cash flow is getting stronger, and even through all the memory-cycle drama, Micron has quietly kept its dividend streak alive for four straight years.

A Snapshot of Micron’s Q2 Results

Micron Technology reported its fiscal second quarter 2026 results on March 18, and this wasn’t just another good quarter from a memory-chip company, but it was AI money showing up in full force. Revenue skyrocketed to $23.9 billion, up a staggering 196% from a year ago, as demand for DRAM, NAND, and especially high-bandwidth memory chips went into overdrive. Those HBM chips have basically become the fuel tanks for AI data centers, and right now, everyone wants more than the industry can produce.

Adjusted EPS amounted to $12.20, crushing expectations and jumping nearly 682% year-over-year (YOY). Across the business, growth looked almost unreal. The Cloud Memory Business unit brought in $7.8 billion in revenue, while the Core Data Center business surged 210.8% annually to $5.7 billion. Even the Mobile and Client segment jumped nearly 245% annually.

And Micron isn’t just posting flashy growth numbers. The balance sheet still looks solid. The company ended the quarter with $16.7 billion in cash and investments against $9.56 billion in debt, while adjusted free cash flow hit a hefty $6.9 billion.

Then came the part that really got traders leaning forward – guidance. Management projected fiscal Q3 revenue around $33.5 billion, plus or minus $750 million, and adjusted EPS near $19.15 per share, plus or minus $0.40. The company is expected to release its Q3 earnings report on Wednesday, June 24.

Also, analysts tracking Micron anticipate the company’s EPS for the third quarter to rise significantly to $19.29. Looking ahead, EPS is expected to be $58.62 for fiscal 2026, which reflects an increase of 663.3% YOY, and then rise by another 73.6% annually to $101.76 in fiscal 2027.

What Do Analysts Expect for Micron Stock?

Wall Street’s getting increasingly comfortable betting big on Micron Technology, and Mizuho just turned up the volume. The brokerage firm recently lifted its price target on MU to $1,150 from $800 while sticking with its “Outperform” rating, signaling it believes the AI memory boom is still in the early innings.

Mizuho expects Micron’s fiscal 2027 revenue and earnings to jump 70% and 85%, respectively, powered by strong DRAM and NAND demand. But the real excitement sits around HBM chips, which are becoming the backbone of AI servers. The firm believes HBM pricing could surge another 70% to 100% next year as supply stays tight and AI demand keeps snowballing. Even outside AI, customers are reportedly still undersupplied, giving Micron another tailwind.

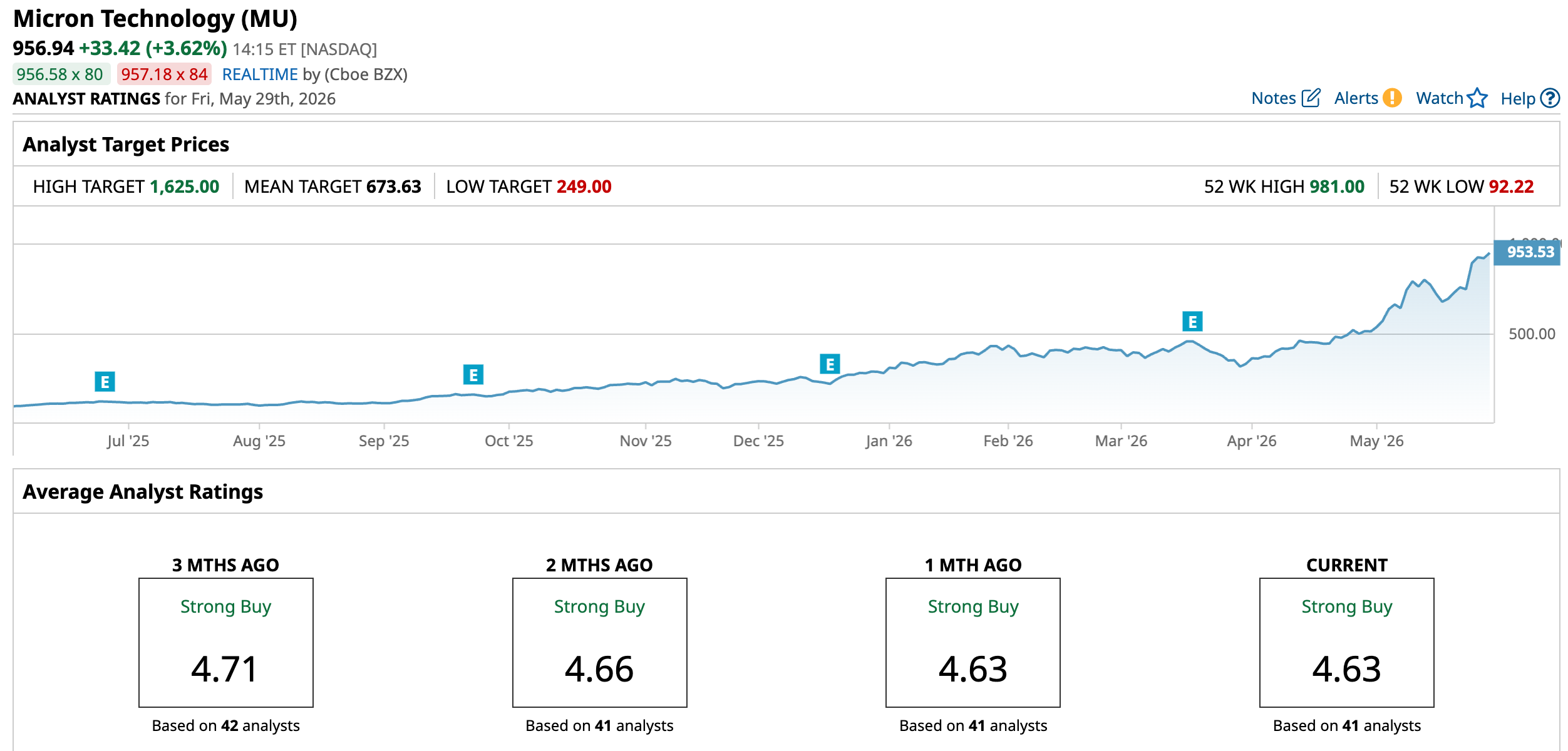

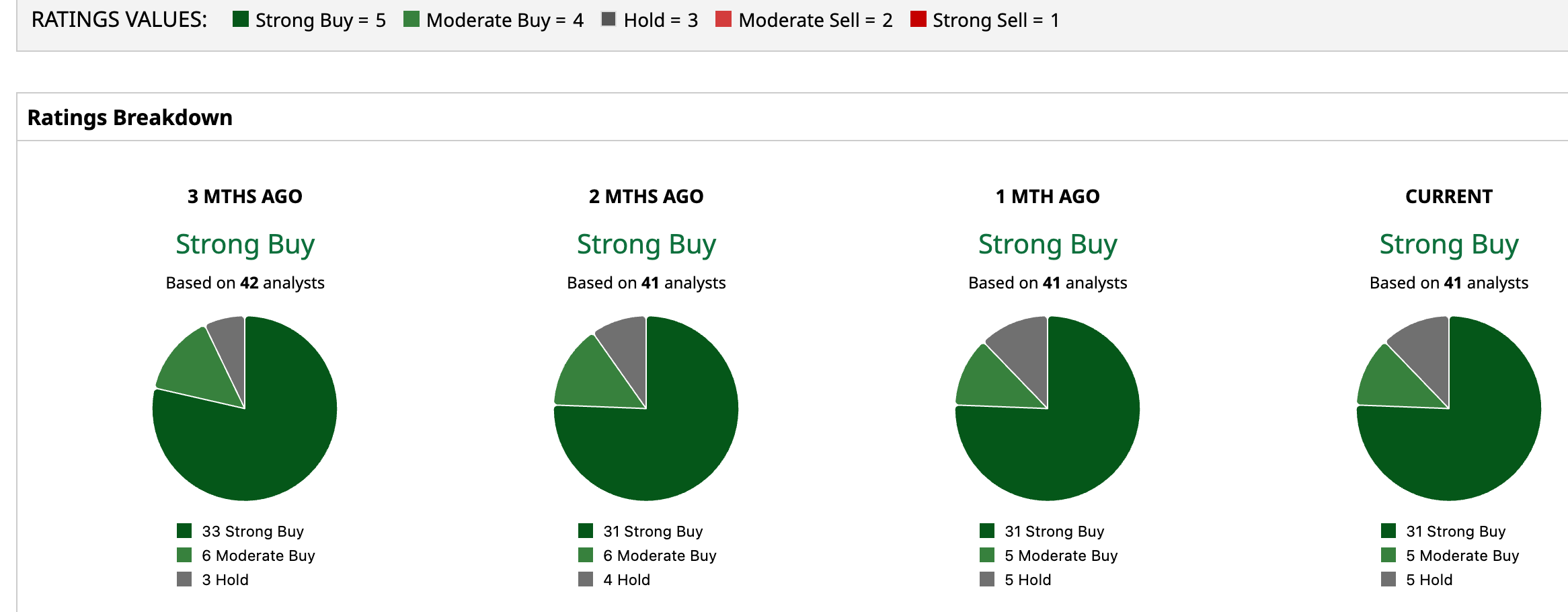

Wall Street’s optimism in Micron is strong. MU has a consensus “Strong Buy” rating overall. Out of 41 analysts covering the AI chip stock, 31 recommend a “Strong Buy,” five advise a “Moderate Buy,” and five analysts stay cautious with a “Hold” rating. Interestingly, Micron’s rally has already pushed the stock past the average price target of about $673.63. UBS’ Street-high target of $1,625 implies 69.8% upside ahead.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wedbush Just Set a New Street-High Price Target of $325 on Palo Alto Networks. What This Means for PANW Stock. Billionaire Mark Cuban Asks Why Insurance Companies Pay $2,500 for an MRI When ‘a Center Down the Street’ Only Charges $350 Dropbox Gets A New CEO. The Payoff for DBX Stock Could Take a Long Time. Micron Stock Is Trading at 42x Trailing Earnings. Analysts Say That’s Still Cheap.