Dell Technologies (DELL) reported an astounding 88% YoY Q1 gain and 42% YoY free cash flow (FCF) growth. DELL skyrocketed almost ⅓ higher on Friday, May 29. But it could be worth much more, up to 30%, based on its strong FCF margins, before buybacks. This article will show why.

DELL closed at $420.91 on the last trading day of May 2026, up 32.76%. And in the last 2 months, it's up $256.78 from March 31 ($164.13), i.e., up 156%. It's all due to strong AI-related demand for its servers and its AI factory with Nvidia (NVDA).

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

DELL stock - last 6 months - Barchart - May 29, 2026

DELL stock - last 6 months - Barchart - May 29, 2026 Moreover, its free cash flow (FCF) surged, even after huge capex increases. That implies DELL stock could keep on this upward trajectory.

Strong FCF and FCF Margins

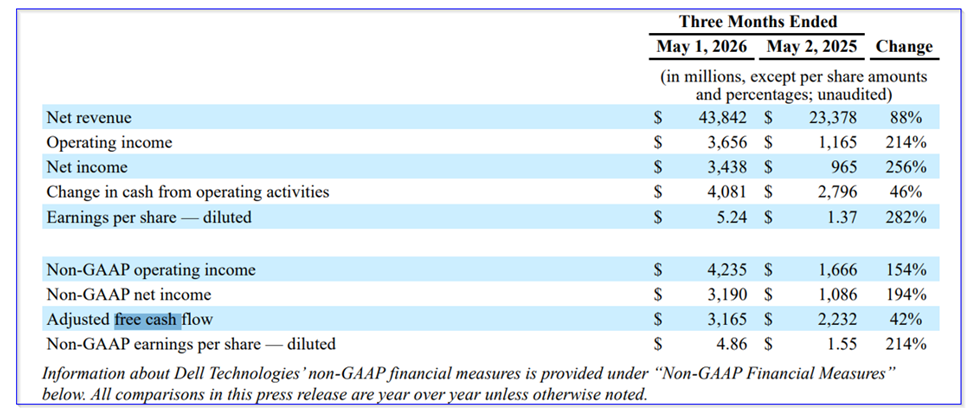

The table from page 3 of Dell Technologies' earnings release shows the strong Q1 revenue and FCF performance.

It shows that revenue rose 88% and its adjusted (adj.) FCF was up 44%, similar to the increase in its operating cash flow (+46%). The difference was due to higher capex.

Dell Technologies - Q1 earnings release - page 3

Dell Technologies - Q1 earnings release - page 3 Note that Dell's FCF margin (i.e., FCF/revenue) was 22.6% lower than last year. Again, that was due to higher capex related to Dell's reinvestment in its operations to meet higher demand.

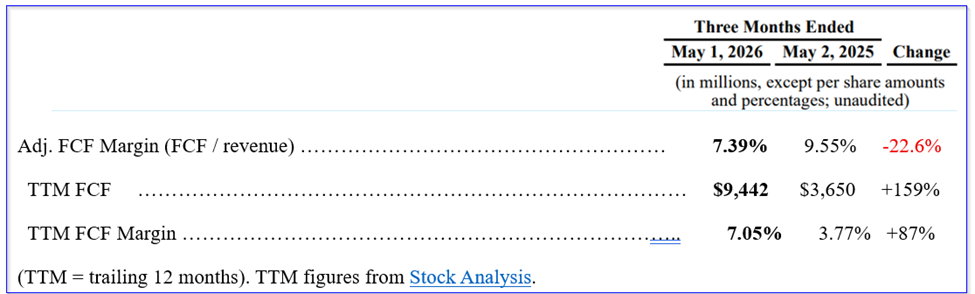

This can be seen in the table I prepared below. However, on a full-year basis, looking back over the trailing 12 months (TTM), Dell's FCF margin was actually higher.

Dell's FCF margins - on a TTM basis, using Stock Analysis data

Dell's FCF margins - on a TTM basis, using Stock Analysis data This shows that both over the past quarter and in the TTM period, Dell has maintained at least a 7.05% FCF margin, even with significantly higher capex outlays. We can use this to project its FCF using analysts' revenue estimates.

Projecting Dell's FCF

For example, based on management's guidance, analysts now project that revenue for the year ending January 2027 will be $170.93 billion. That is up 50.6% from last year ($113.538 billion), and even +27.6% from its TTM revenue of $134 billion, according to Stock Analysis.

Moreover, for the following year, these analysts are now projecting $184.32 billion. That's up $50 billion from its TTM revenue (i.e., +37.3%). This implies Dell's free cash flow could surge from here.

For example, if the company can maintain a 7.05% FCF margin, even though it's likely to increase just as it did from a year ago), FCF could rise to $13 billion:

$184.32b x 0.0705 = $13.0 billion in FCF FY 2028

That is 37.7% over the $9.442 billion in TTM FCF it made over the past year (see the table above). This implies Dell's valuation could rise from here.

Valuing DELL Stock Using FCF Yield

Let's assume that Dell pays out 100% of its FCF to shareholders. Given its market cap of $273.41 billion (according to Yahoo! Finance), the dividend yield would be:

$9.442b TTM FCF / $273.41 billion mkt cap = 0.0345 = 3.45%

Given the future time frame, let's round that up to 3.50% and apply it to our FY 28 FCF estimate:

$13.0b / 0.035 = $371.43 billion future mkt value

In other words, Dell stock can be expected to rise almost $100 billion (i.e., $371.43b - $273.41b = +98.02 billion), or +35.9%:

$98.02b / $273.41b = 0.3585

This means our price target for DELL stock is 35.9% higher:

$420.91 x 1.3585 = $571.80 price target (PT)

However, there is a good deal of risk with this estimate. For example, if management cannot maintain a 7% FCF margin, the $13 billion FCF estimate will be much lower.

Summary and Conclusion

Dell could be worth up to 36% more based on these estimates. However, this DELL price target should probably be discounted by the time value of money, say 5%. This is because the PT is based on FY 2028 revenue and FCF estimates (over a year from now):

1/1.05 = 95.238%

So, $571.80 x 0.95238 = $544.57 price target

However, that revised PT is still $123.66 over Friday's close, i.e., +29.4% upside.

The bottom line is that DELL stock looks undervalued here, despite its rise.

However, investors should look for opportunities to buy DELL stock at a cheaper level. I will discuss ways to do this, including shorting out-of-the-money (OTM) put options, later this week in a future Barchart article.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dell Stock Could Be Worth 30% More - Based on Strong AI Demand and FCF Option Volatility And Earnings Report For June 1-5 Jobs Data, Tech Earnings and Other Key Things to Watch this Week How Overzealous Option Traders Are Making 3X Leveraged ETFs Look Like Saviors