The artificial intelligence race has divided the stock market into two camps. On one side, manufacturers of hardware with their astronomical multipliers. On the other, a multitude of startups, promising to disrupt the market, but for now burning capital.

Investors in search of windfall profits often forget about Warren Buffett's first rule of investing: Never lose money. If you search for an asset that will allow you to participate in the development of technologies of artificial intelligence, but still sleep soundly, Alphabet (GOOG) (GOOGL) looks like the most protected fortress on the market. Yes, this is one of the most expensive companies in the world by capitalization. Possibly, it will not show the fastest multiple growth in short-term perspective. But from the point of view of the balance of risk and sustainability of the business-model, Alphabet today is in a league of its own. And here are the fundamental reasons why.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comAdequate Valuation and Nature of Profit: Where There Is No Place for Bubbles

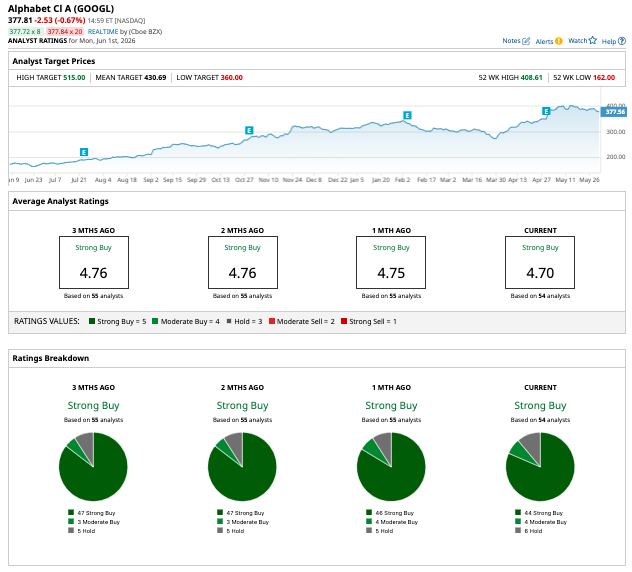

Today the P/E multiplier of Alphabet currently sits at a very reasonable 29–30x. For the leader of the technological sector, this is a grounded valuation. But the main here is even not the figure itself, but the quality and structure of revenue, on which this P/E bases itself. Let us compare the nature of incomes of the current favorites of the market.

Windfall profits are “here and now.” A number of the largest technological giants today show a cosmic margin due to a temporary factor: a bottleneck and a deficit of equipment. Investors price this margin into future periods, forgetting, that any deficit sooner or later comes to an end. As soon as supply catches up with demand, windfall profits can correct. Infrastructural overheating. Other players — for example, in the segment of e-commerce and clouds — extract a huge benefit from the deficit of cloud computing. If this deficit changes to a surplus, their financial indicators will turn out under pressure.

Google has a fundamentally different story. Its revenue is based on classic, understandable and maximally reliable sources of income, in which physically there are no signs of a bubble. Search advertising sells by standard market prices, tied to the real sector of the economy and consumption. YouTube generates advertising and subscription revenue by ordinary, organic tariffs. User subscriptions — such as Google One and YouTube Premium — are a stable, forecastable regular income (ARR), not depending on the hype around AI. Alphabet does have a cloud segment (Google Cloud), but given the giant's scale possible fluctuations of cloud pricing, this is a drop in the bucket. The core framework of the company is protected from momentary market deformations. There isn't room for these incomes to deflate.

Absolute Vertical Integration and Access to the Client

Technology for the sake of technology does not bring profit. In the end, he who can deliver this technology to billions of users without overpaying middlemen wins. Google possesses a full cycle, including chips and architecture, unlike many players on the market who are forced to rely on complex partnerships with creators of language models or do not have its own mass ecosystem. The company has developed its own processors (TPU) for years and pioneered the Transformer architecture that became the backbone of modern AI.

Alphabet also has direct access to consumers. Android, Chrome, YouTube and Google — these are billions of daily touches. Google does not need to search for whom to sell its artificial intelligence, it simply integrates AI into products that the world already uses every second.

Finally, Alphabet has an uninterrupted flow of behavioral data that makes their AI-models self-learning and unique.

Successful Passing of the ‘Crash Test’: Immunity to the Overproduction of Capacities

I recently analyzed in detail the approaching threat of hyper-saturation of the market by data centers. The market of AI-infrastructure can in the nearest future collide with a harsh “crash test.” If the colossal capital expenses of the technological sector lead to an oversupply, spot prices on cloud computing will inevitably go downward. For companies whose business model builds itself predominantly on resale or renting out of computing capacities to other businesses, this could become a strong blow to the margin.

For Google, this scenario is not simply safe. It is advantageous. Alphabet builds infrastructure and data centers primarily for itself. If the cost of compute on the market falls multiple times, the operating costs to support search, the generation of AI-answers, and YouTube could lower. That could worsen the margin of purely infrastructural players and make the own end services of Google more profitable.

Financial armor: Real Cash Against Expectations

Building AI infrastructure demands astronomical capital expenses (capex). Many companies are financing this construction at the expense of the debt market or overstated expectations of investors. Google finances its AI initiatives with a powerful operational cash flow from its diversified advertising and service business. Real, cold hard cash. It flows into the accounts of the company uninterruptedly. Even if the AI-effect on the market begins to cool temporarily, and the commercialization of technologies goes slower than forecasts, the base business of Alphabet will not disappear. The company has more than enough margin of safety to stay in the game, to continue systematic investments, and calmly to survive any market turbulence.

www.barchart.com

www.barchart.comSummary

Buying Alphabet by a multiplier around 30x, you acquire not simply a promise of future AI-revolutions. You buy a super-profitable company generating a gigantic cash flow classic business that is protected from infrastructural shocks. This is an instrument that allows shareholders to find themselves on the frontline of technological progress and minimize risks tied to the overheating of separate segments of the market. Reliability and revenue security cost a lot, but in the epoch of macroeconomic storms they are exactly what allows you to sleep soundly.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

If You Want to Invest in AI Without Losing Sleep, Buy Google Stock Now Dear Microsoft Stock Fans, Mark Your Calendars for June 2 Nucor Is Fighting the Tariff Tide as NUE Stock Surges 130% Dell Stock Is No Longer Just Riding the AI Wave. It Is Leading the Charge.