SentinelOne (S) stock has performed poorly in the last 52 weeks with a decline of nearly 10% during the period. This sluggish performance can be attributed to results that have disappointed the markets even as the industry outlook remains bright.

For the first quarter of fiscal 2027, SentinelOne missed top-line estimates marginally while Q2 guidance fell short of expectations. Besides concerns related to growth acceleration, SentinelOne also recently announced that it is letting go of approximately 8% of its employees. This will likely translate into a one-time charge of $25 million.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

However, not all analysts are concerned. Wedbush analyst Dan Ives has an “Outperform” rating with a price target of $20 for S stock. Ives believes that under new CFO Sonalee Parekh, the company is positioned to “capture the growing opportunity around AI security.” Similarly, Bank of America has a “Buy” rating and believes the selloff is overdone.

Amidst such mixed sentiment, there is a strong case for considering SentinelOne stock after a period of underperformance, especially as the company’s Singularity Platform can potentially deliver steady annual recurring revenue (ARR) growth in a big addressable market.

About SentinelOne Stock

Headquartered in Mountain View, California, SentinelOne is a cybersecurity provider through its Singularity Platform. According to the company, Singularity is one of the first purpose-built AI-powered cybersecurity platforms for autonomous defense. SentinelOne’s generative AI technology, Purple AI, is fully-integrated across Singularity solutions, helping organizations run autonomous security operations.

SentinelOne has a global presence. For fiscal 2026, the company derived roughly 39% of revenue from outside of the United States. Fiscal 2026 also saw SentinelOne report revenue of more than $1 billion, implying year-over-year (YOY) growth of 22%. For the same period, the company reported a non-GAAP gross margin of 79% and a non-GAAP operating margin of 3%.

While SentinelOne has delivered mixed numbers, S stock has remained sideways in the last six months, down by 3%. This seems like a good accumulation opportunity as the company leverages on AI-powered cybersecurity to pursue growth acceleration.

www.barchart.com

www.barchart.com Positive Points From SentinelOne's Q1 2027 Results

The markets were disappointed with SentinelOne's recent Q1 results, which came in largely in-line with estimates. However, there were ample positives in the quarterly results that point to continued growth.

As of Q1, SentinelOne reported ARR growth of 23% on a YOY basis to $1.16 billion. Further, it’s worth noting that the number of customers with ARR of $100,000 or higher was 1,411 as of January 2025 and 1,667 as of January 2026. At the end of Q1, this figure swelled to 1,702 customers, suggesting a clear positive trend pointing to continued upside in ARR.

SentinelOne's adjusted free cash flow margin was 22% in Q1. Further, the firm reported a cash buffer of $812 million. Financial flexibility is therefore robust for both organic growth and acquisition-driven growth. In September 2025, SentinelOne expanded its platform capabilities through the acquisition of Prompt Security and Observo AI.

Lastly, another bullish point to note is that the company reached 50% ARR from non-endpoint solutions, which includes data, AI, and cloud. Growth acceleration from these solutions is a positive catalyst for the coming years, considering structural industry tailwinds for both AI and cloud businesses.

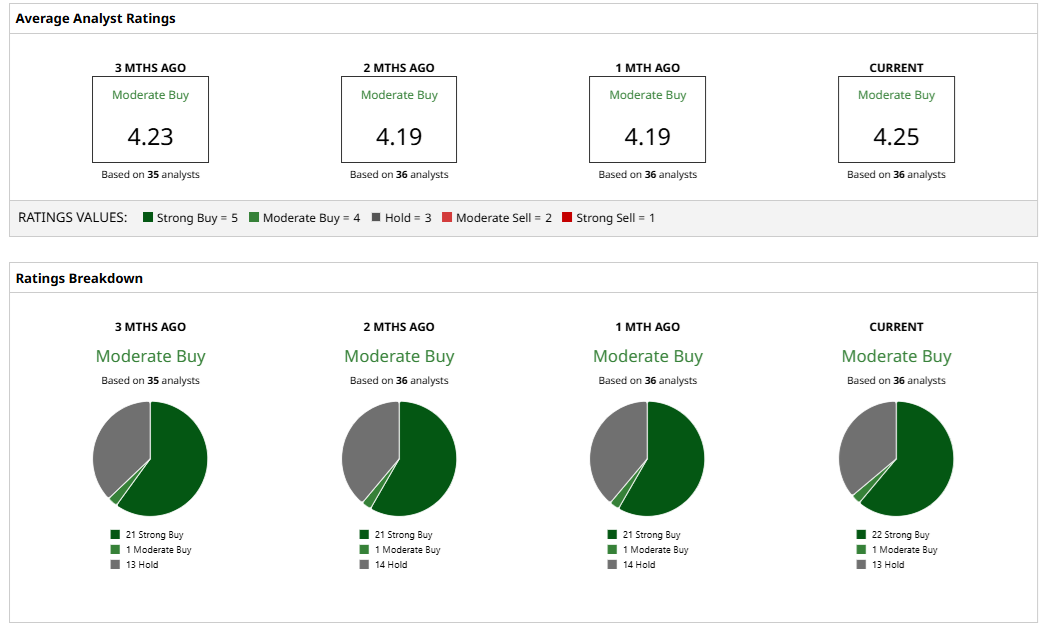

What Do Analysts Say About SentinelOne Stock?

Based on 36 analysts with coverage, S stock has a consensus “Moderate Buy” rating. While 22 analysts have a “Strong Buy” rating for S stock, one analyst has a “Moderate Buy,” and 13 have a “Hold” rating.

The mean price target of $19.63 represents potential upside of 18% from current levels. Meanwhile, the most bullish price target of $26 suggests that S stock could climb as much as 57% from here.

www.barchart.com

www.barchart.com Conclusion

For 2025, SentinelOne believes that the total addressable market for the company’s solutions was in excess of $100 billion. Therefore, there is ample headroom for growth.

Specific to the company, it’s worth noting that operating margin was -19% for fiscal 2024. However, SentinelOne's operating margin expanded significantly to 3% in fiscal 2026. With steady growth in ARR, it’s likely that long-term margin expansion will sustain and translate into cash flow upside.

Overall, the markets seem to have overreacted to the layoff news. SentinelOne is likely to deliver steady results backed by industry tailwinds as well as both organic and acquisition-driven growth.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Spend $75 or Less to Make Contrarian Bets on These 3 Hard-Hit Value Stocks Wedbush Just Increased Its Price Target on IBM Stock. The Company Is Quietly Building a New Chapter. The SentinelOne Stock Correction Is Overdone as the Singularity Platform Drives Steady Growth Up 1,000% in the Past Year, It’s Too Late to Buy Western Digital Stock