Palo Alto Networks (PANW) delivered strong FY 26 Q3 free cash flow (FCF) growth (+57%), and its adjusted FCF margin rose to 37.5% of sales. Management is targeting a 40% adj. FCF margin in FY 28. Using a 37.5% margin against analysts' FY 27 forecasts could push PANW stock 29% higher to $350 p/sh. This article will show how this works.

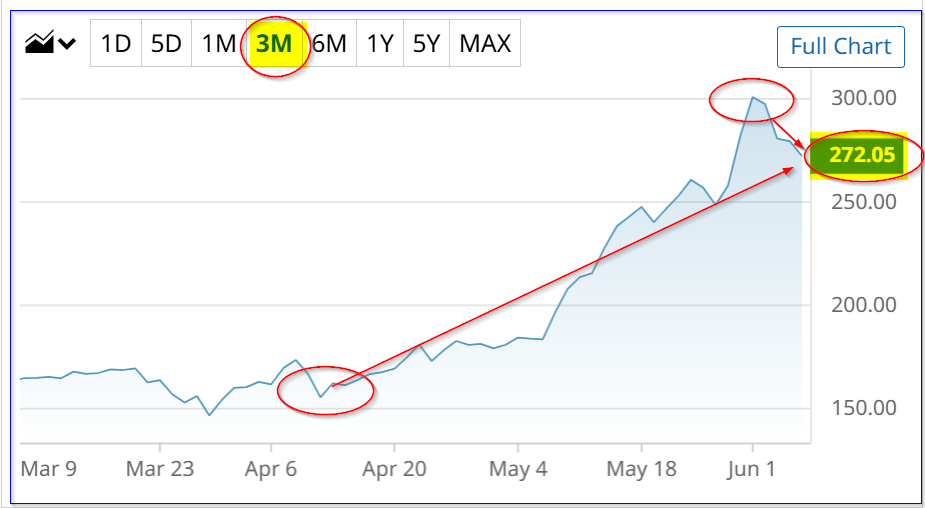

PANW closed Friday down 2.6% to $272.05, and it's off a pre-earnings peak of $300.48 on June 1, before the June 2 earnings release for the quarter ending April 26.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

PANW stock - last 3 months - Barchart - June 5, 2026

PANW stock - last 3 months - Barchart - June 5, 2026 But PANW is up significantly from a month and a half ago, when I wrote an April 21 Barchart article, “Palo Alto Networks Stock Looks Cheap Ahead of Earnings - Shorting PANW Puts Works.”

In that article, I wrote that PANW stock could be worth $199 when it was trading for $169.56. So it has blown past my price target and those of other analysts.

Can it keep rising from here? After all, PANW is down from its peak. Let's look at its free cash flow (FCF) more closely.

FCF Margins Could Push FCF Higher

Palo Alto Networks, which sells cybersecurity solutions, mostly on a subscription basis, reported that its FY 26 Q3 revenue rose 31% YoY to $3 billion. Its free cash flow, on an adjusted basis, was $910 million, representing 30% of revenue.

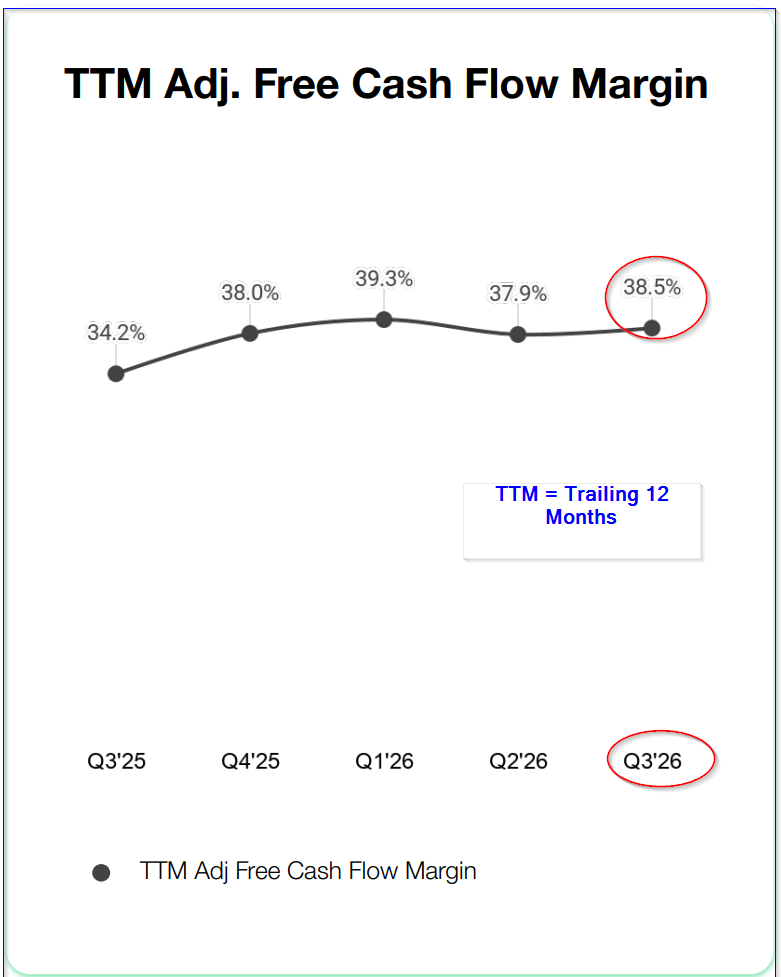

However, the company likes to look at things on a full-year rolling basis, since at least one quarter has significantly higher numbers due to subscription renewals. For example, its trailing 12-month (TTM) as of Q3 (ending April 2026) was 38.5% of revenue.

This has been trending upward, as can be seen in a chart the company produced in its deck (page 15):

Palo Alto Networks Q3 Presentation Deck - Q3 2026 - page 15

Palo Alto Networks Q3 Presentation Deck - Q3 2026 - page 15 Moreover, management is now saying it is targeting a 37.5% FCF margin for this fiscal year ending June 30, and a 40% margin by FY 28.

This is really quite extraordinary. Very few companies report their FCF margins, but also announce a forecasted FCF margin target.

This shows a high degree of confidence by management not only in its revenue growth but also in its ability to limit expense growth.

It also allows investors to set a very clear price target.

Price Targets for PANW Stock

For example, analysts surveyed by Seeking Alpha now project FY 2027 revenue (ending June 2027) will rise from the $11.42 billion forecast this FY to $13.77 billion.

As a result, if management can deliver a 37.5% adj. FCF margin next year, FCF could rise over $5 billion:

$13.77 b FY 27 revenue x 0.375 = $5.164 billion adj. FCF

That is over $1 billion higher than the $4.08 billion it generated over the trailing 12 months to Q3, with a 38.5% TTM FCF margin.

That could push PANW higher. Here's why.

Its FCF margin right now is 1.84%, since the market cap is $221.7 billion:

$4.08b TTM FCF / $221.7b mkt value = 0.0184 = 1.84% FCF yield

So, using the FY 27 FCF estimate:

$5.164b FCF / 0.0184 FCF yield = $280.7 billion market value

That is 26.6% higher than Palo Alto Networks' existing market cap ($221.7b). It implies a price target (P/T) of $344 p/sh:

1.266 x $272.05 = $344.42 PT

Adjusted Price Targets

However, given that the company has already generated a 38.5% TTM adj. FCF margin, and its goal is 40%, we could conservatively use a 38% adj. FCF margin for FY 27:

$13.77b FY revenue x 0.38 = $5.233 billion adj. FCF

$5.233b / 0.0184 = $284.4 billion mkt value

$284.4 / $221.7b = 1.283 = +28.3% upside

That implies a PT of $349 per share (i.e., $272.05 x 1.283). That's close enough to $350, since using a 1.8% FCF margin puts the value at $290 b, or +30.8% (i.e., $355 p/sh).

The bottom line is that PANW is between 26% to 31% undervalued, or a value of $350 per share. Analysts tend to agree. Yahoo! Finance, for example, shows that the average PT is $306.56, and Barchart's mean survey is $308.14.

Shorting OTM PANW Puts

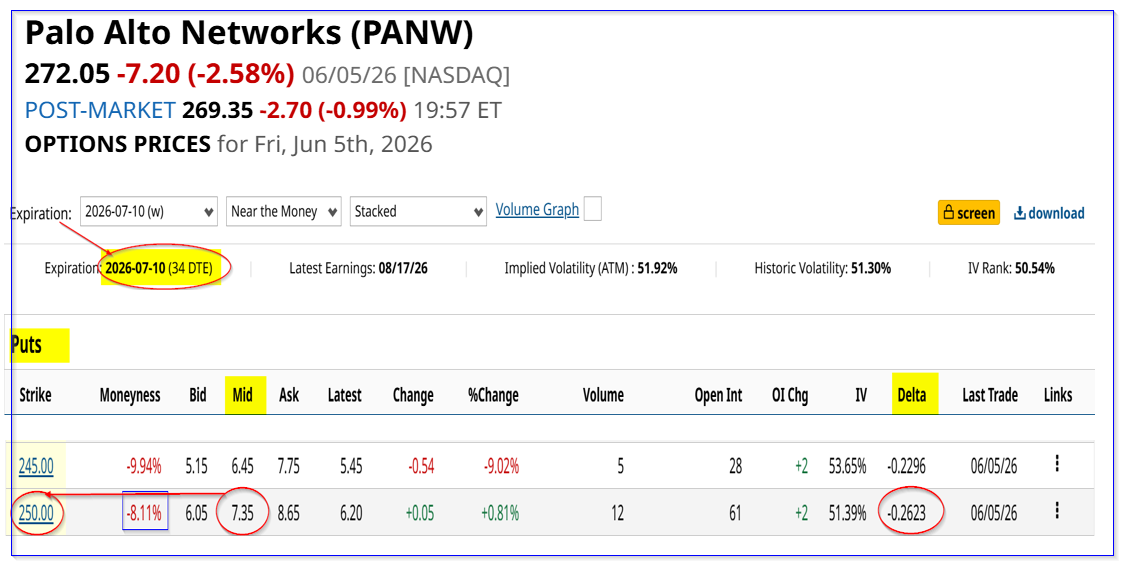

However, there's no guarantee this will happen. There is one play to help with this: shorting out-of-the-money (OTM) puts in near-term puts (usually one-month).

For example, the $250 put expiring July 10 (34 days from now) is 8% below Friday's close and has a 26% delta ratio (not high). The midpoint premium is $7.35, so a short-seller makes an immediate yield of 2.94% (i.e., $7.35/$250.00) for one month.

PANW puts expiring July 10 - Barchart - As of June 5

PANW puts expiring July 10 - Barchart - As of June 5 Moreover, the potential breakeven buy-in is $242.65 (i.e., $250-$7.35), which is 10.8% below the price on June 5. That makes it an attractive potential buy-in.

The bottom line is that PANW still looks undervalued, and one way to play it is to short OTM puts.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Palo Alto Networks Delivers Strong FCF Margins - Is PANW Worth $350? After Recent Rally Sparked by Jensen Huang’s Comments, Marvell Stock Is a Buy Using SPY Put Options For Portfolio Protection Stock Index Futures Climb as Tech Stocks Rebound, U.S. Inflation Data and SpaceX IPO Awaited