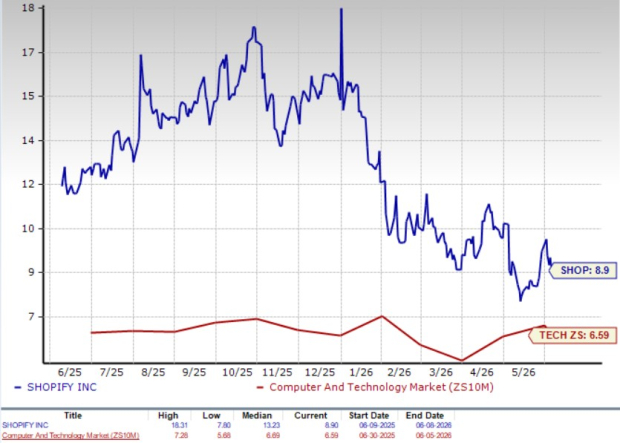

Shopify Inc. SHOP enters the second half of 2026 with a valuation that leaves little room for disappointment. The stock currently trades at a forward 12-month price-to-sales (P/S) ratio of 8.9x, well above the industry average of 6.59x, reflecting investors’ confidence in the company's long-term growth prospects.

The premium becomes even more evident when Shopify is compared with its peers. Amazon AMZN and Wix.com WIX trade at significantly lower forward P/S multiples of 3.03x and 1.16x, respectively. Such a valuation gap suggests that the market expects Shopify to continue delivering superior revenue growth and execution.

SHOP P/S (F12M)

Image Source: Zacks Investment Research

However, the stock's recent performance has not fully matched these lofty expectations. Over the past year, Shopify shares have gained just 0.4%, lagging both the industry's 42.6% growth and the S&P 500's 26% advance. Within its peer group, Amazon has posted a 13% gain, while Wix.com has experienced a sharp 68.7% decline.

Price Performance

Image Source: Zacks Investment Research

Given its rich valuation and relatively muted stock performance, investors may be wondering whether Shopify can generate enough growth and profitability improvements to support its premium multiple. As the company heads into H2 2026, its ability to execute on key growth initiatives will likely determine whether the stock can close the performance gap and reward shareholders.

Factors Likely to Aid Shopify in H2 2026

Shopify enters the second half of 2026 with several growth drivers supporting its outlook. One of the biggest catalysts is the company's deep integration of artificial intelligence across its platform. Shopify's AI-powered assistant, Sidekick, is witnessing rapid adoption, with weekly active shops using the tool increasing nearly fourfold year over year. The platform is helping merchants automate tasks, create custom applications and improve store operations, making Shopify's ecosystem increasingly sticky and valuable.

The company is also benefiting from the rise of AI-driven shopping channels. Shopify reported that traffic from AI-powered sources increased eightfold year over year, while orders generated through AI searches jumped nearly thirteenfold. By integrating with platforms such as ChatGPT, Microsoft Copilot and Google's AI services, Shopify is positioning itself at the center of the emerging agentic commerce ecosystem.

Another major growth lever is enterprise adoption. Shopify continues to attract large global brands while expanding relationships with existing merchants. The number of merchants generating more than $100 million in annual GMV on the platform has nearly doubled over the past two years, highlighting growing traction among larger businesses.

The company's payments business remains a significant contributor. Shopify Payments processed $67 billion in GMV during the quarter, up 41% year over year, while Shop Pay volume surged 59%. International markets also remain a bright spot, with international GMV rising 45%, supported by ongoing product localization and cross-border commerce initiatives.

Factors That Could Hurt Shopify Stock

Despite its strong growth trajectory, Shopify faces several risks that investors should monitor. Valuation remains a key concern. The stock trades at a premium to both the broader industry and major peers, leaving little room for operational missteps or slower-than-expected growth.

The company is also increasing investments in AI infrastructure. Management noted that growing adoption of AI tools such as Sidekick is driving higher large-language-model costs. While these investments may strengthen Shopify's competitive position over time, they could weigh on margins if expenses rise faster than revenues.

Competition is another challenge. Shopify operates in a rapidly evolving commerce landscape where rivals are aggressively investing in AI-powered shopping experiences, payments and merchant services. Maintaining technological leadership will require continuous innovation and execution.

In addition, Shopify's Merchant Solutions business is becoming a larger portion of revenue. Although this supports top-line growth, it generally has lower margins than Subscription Solutions, which could limit gross margin expansion over time. Management also expects Europe to remain a near-term headwind to payment penetration metrics as newer payment markets mature.

Finally, Shopify's growth thesis is increasingly tied to the adoption of AI-powered commerce and agentic shopping. If consumer adoption of these emerging channels develops more slowly than expected, some of the anticipated growth benefits may take longer to materialize.

SHOP’s Growth Projection Encourages

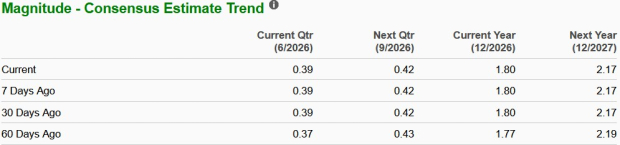

Over the past 60 days, the company’s earnings for fiscal 2026 and 2027 have increased 3 cents and decreased 2 cents, to $1.80 and $2.17, respectively. The Zacks Consensus Estimate for SHOP’s 2026 and 2027 earnings per share indicates a year-over-year increase of 53.9% and 20.8%, respectively.

Image Source: Zacks Investment Research

The consensus estimate for revenues is pegged at $14.71 billion and $17.99 billion for 2026 and 2027, respectively, implying a year-over-year improvement of 27.3% and 22.3%.

Wrapping Up

Shopify continues to execute well, supported by strong momentum in artificial intelligence, enterprise adoption, payments and international expansion. The company's ability to attract larger merchants, deepen engagement across its ecosystem and capitalize on emerging AI-driven commerce trends positions it favorably for long-term growth. In addition, earnings and revenue expectations point to sustained business expansion over the next few years. However, much of this optimism appears to be reflected in the stock's premium valuation, which remains well above industry levels and several key peers. Given the combination of solid fundamentals and elevated valuation, existing investors may consider holding the stock to benefit from Shopify's ongoing growth initiatives.

However, fresh investments may be best deferred until a more attractive entry point emerges, as any slowdown in execution, margin pressure from AI investments or weaker-than-expected adoption of new commerce channels could limit near-term upside.

SHOP currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Wix.com Ltd. (WIX): Free Stock Analysis Report

Shopify Inc. (SHOP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).