At a closed-door event in Taiwan, Nvidia (NVDA) CEO Jensen Huang reiterated what he has been saying out loud all this time, although this time his words were a little bit more uncharitable for the AI-suspecting public.

“Remember last year when we were together, the rhetoric and the narrative around the investment were, 'What's the ROI?'Give me one example of some crazy person saying that now. They're going to sound insane. … Only for the last six months has the ROI been completely reset. [AI] is now insanely profitable," Huang said.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Huang may be sounding haughty to some, but what he has made Nvidia achieve in recent years is there for all to see. Nvidia's shares are up more than 1,017% over the past five years, and it is now the most valuable company in the world with a market cap exceeding $5 trillion. Notably, even amid murmurs of AI fatigue this year, NVDA stock is up 7.46% year-to-date (YTD).

www.barchart.com

www.barchart.com Is NVDA still a good investment now? Yes, so let's explore the reasons behind that bet.

Financials As Sound As They Can Be

Nvidia maintained its impressive momentum during the latest reporting period, posting impressive expansion, outperforming forecasts on revenue and profits, and lifting its future outlook.

Revenue climbed 85% year-over-year (YOY) to $81.6 billion, fueled mainly by the data center business, which surged 92% to $75.2 billion. Looking ahead to the second quarter, the company projects revenue of $91 billion, with no contribution assumed from China, compared to analyst estimates of $91.73 billion.

Earnings per share increased to $1.87, representing a 140% improvement over the year ago quarter and clearly topping the consensus view of $1.75. This achievement marked the ninth consecutive quarter of beating profit expectations. Gross margins showed notable strength, rising to 75% from 60.8% in the previous year.

Cash flow remained robust, as net cash from operating activities grew to $50.3 billion from $27.4 billion a year earlier. By the close of the fiscal first quarter, Nvidia held $13.2 billion in cash with only a modest short term debt position of $1 billion.

On valuation, NVDA differentiates itself from several other Magnificent Seven members with more balanced metrics. The forward price-to-earnings ratio of 24.23 times stands below the sector median of 25.09 times, while the forward price-to-sales multiple of 12.87 times and price-to-cash flow multiple of 24.02 times compare to sector medians of 3.34 times and 19.79 times, respectively.

What's Next?

There is a perception gaining ground, especially after the recent launch of Alphabet's (GOOG) (GOOGL) 8i TPUs, that Nvidia will play second fiddle in inferencing. Although how this battle plays out in the future will be fascinating to observe, Nvidia is not laying its tools down for the time being at all.

Nvidia plans to take advantage of Groqs SRAM-focused architecture to boost performance on inference-focused workloads through an approach known as disaggregation, implemented at the full rack level. This strategy separates the token generation sequence into distinct prefill and decode phases and assigns each phase to the hardware optimized for that specific function. The compute-intensive prefill stage runs on advanced Rubin graphics processing units, while the memory and cache-heavy decode operations shift to the specialized LPX rack.

Huang estimates that integrating these two purpose-built rack systems could achieve up to 35 times higher throughput per megawatt when handling LLMs with trillions of parameters. The performance benefits stand out most clearly in demanding applications that require rapid token generation, such as live interactions with AI agents.

Meanwhile, one of the key pillars of the company's moat is the CUDA ecosystem, and with the recent launch of CUDA 13.2, it has become more embellished. CUDA 13.2 extended CUDA Tile support to Ampere and Ada architectures, introduced closures and recursion into cuTile Python, and unified the ARM toolkit so that the same codebase runs seamlessly from data center GPU to Jetson edge device, which is a critical enabler for physical AI workloads.

Finally, there is physical AI, a $500 billion market that Huang is personally excited about. NVIDIA's strategy here is a bit different. For instance, Nvidia's robotics strategy is to not build the robots but to build the platform that everyone needs to build robots, with every major humanoid company, including Figure AI, Agility Robotics, Apptronik, Unitree, and Boston Dynamics, using some combination of Isaac Sim, GR00T, Cosmos, and Jetson for edge inference. At GTC 2026 in March, the company sharpened this platform. Nvidia unveiled Isaac GR00T N open models, updated Cosmos world foundation models for synthetic data generation, and partnered with Hugging Face to integrate Isaac and GR00T into the LeRobot open-source framework, connecting Nvidia's 2 million robotics developers with Hugging Face's 13 million AI builders worldwide.

For automobiles, on the other hand, Nvidia boasts an enviable list of partners. At GTC 2026 in March, Nvidia expanded its autonomous vehicle deals to include Hyundai Motor, Nissan, Isuzu (ISUZY), BYD Company (BYDDY), and Geely, all signing on to the DRIVE Hyperion platform, joining an existing roster that already includes Mercedes-Benz (MBGYY), Toyota (TM), General Motors (GM), Volvo (VLVLY), and JLR. Mercedes-Benz is bringing Level 2++ capabilities to U.S. roads starting in 2026, JLR vehicles will be built on the DRIVE AI-defined platform starting in 2026, and Volvo's EX90 runs on DRIVE AGX Orin with plans to migrate to DRIVE Thor. Also, Nvidia partnered with Uber (UBER) to deploy autonomous robotaxis across 28 cities on four continents by 2028, starting in Los Angeles and San Francisco, which gives Nvidia a direct stake in the robotaxi deployment wave.

Analyst Opinion

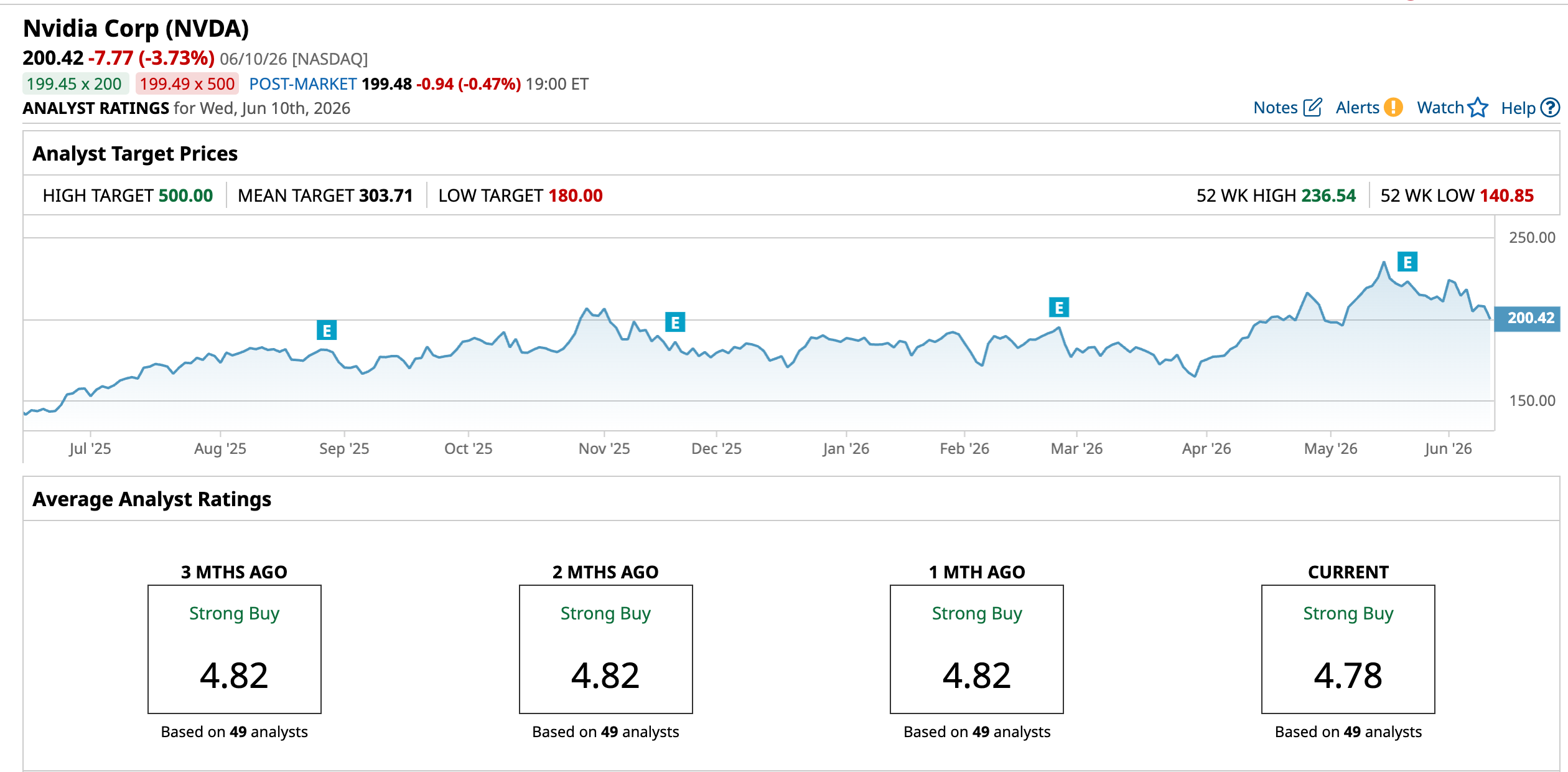

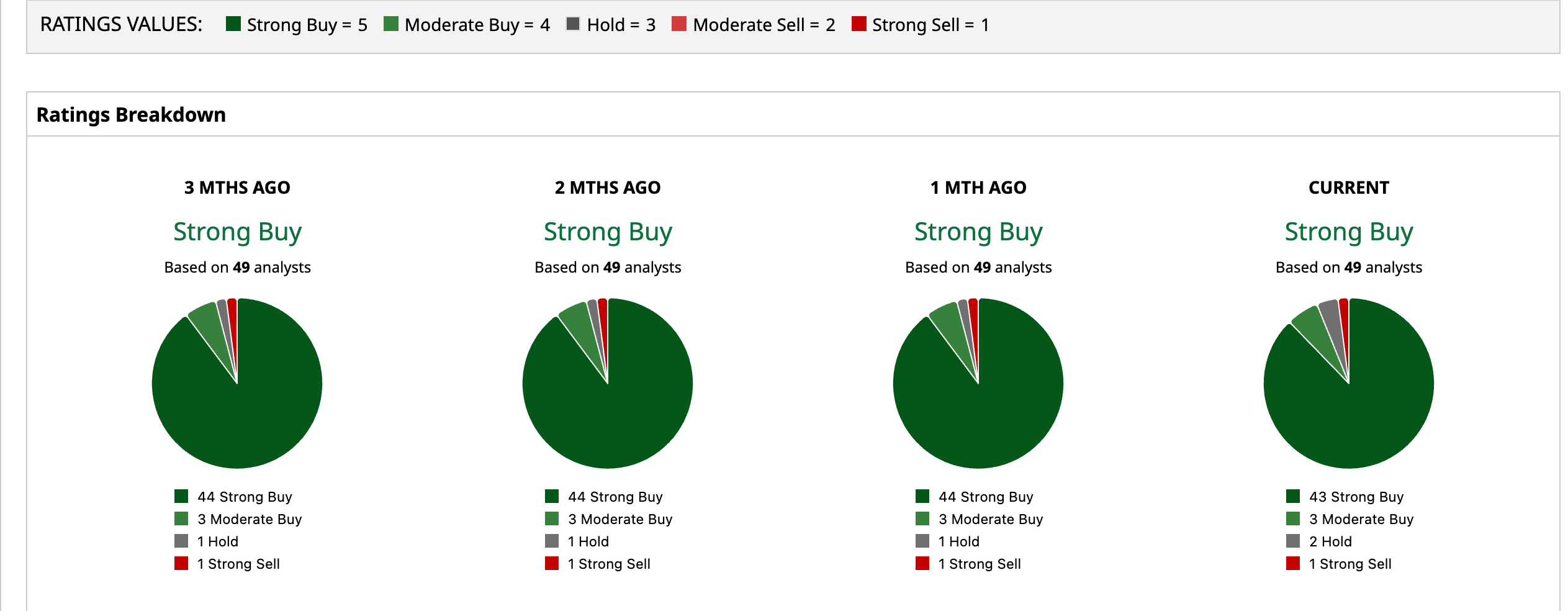

Overall, the Street remains optistic about NVDA stock, attributing to it a rating of “Strong Buy.” The mean target price of $303.71 indicates an upside potential of 51.5% from current levels. Out of 49 analysts covering the stock, 43 have a “Strong Buy” rating, three have a “Moderate Buy” rating, two have a “Hold” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FuelCell Stock Sink After Q2 Earnings Miss. Why 267% Pipeline Growth Wasn’t Enought. Jensen Huang Says AI Is ‘Insanely Profitable.’ That Means It’s Not Too Late to Hop on the Nvidia Bandwagon. Blue Owl Capital President Logan Nicholson Just Bought 3,000 Shares of OBDC Stock Amid Private Credit Scandal Nvidia Chose This AI Cloud Stock Over Everyone Else. Here’s Why.