The business models of legacy software and information technology (IT) companies are being threatened by artificial intelligence (AI). It's not only investors who are ditching these companies to chase hot AI stocks, but also even top executives are on a similar path.

During its fiscal Q2 2026 earnings call, Adobe (ADBE) announced that its CFO, Dan Durn, would depart the company. Durn would join Marvell Technologies (MRVL), whose shares have more than tripled this year. Adobe, on the other hand, is trading near multi-year lows and is among the top losers of the S&P 500 Index ($SPX) in 2026.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

AI Stocks Have Soared in 2026

A cursory look at the index constituents underscores AI being the predominant theme this year. Accenture (ACN), Intuit (INTU), Gartner (IT), Workday, Salesforce (CRM), and Cognizant Technology (CTSH) are among the worst-performing S&P 500 Index stocks this year, with all losing at least a third of their market cap. These names are perceived as AI losers and have been squarely out of favor with investors.

www.barchart.com

www.barchart.comStacked at the top are AI companies, in particular chip and memory plays like SanDisk (SNDK), Micron (MU), Intel (INTC), and Seagate (STX). Notably, Intel, which fell to multi-year lows last year, has been an investor favorite and has risen sixfold from its 2025 lows.

Adobe Has Lost Top Leadership

Coming back to Adobe, it previously announced the departure of long-time CEO Shantanu Narayan during the Q1 earnings call in March. Losing both the CEO and CFO in a span of three months is hardly a positive development for any company and has only added fuel to ADBE’s sell-off.

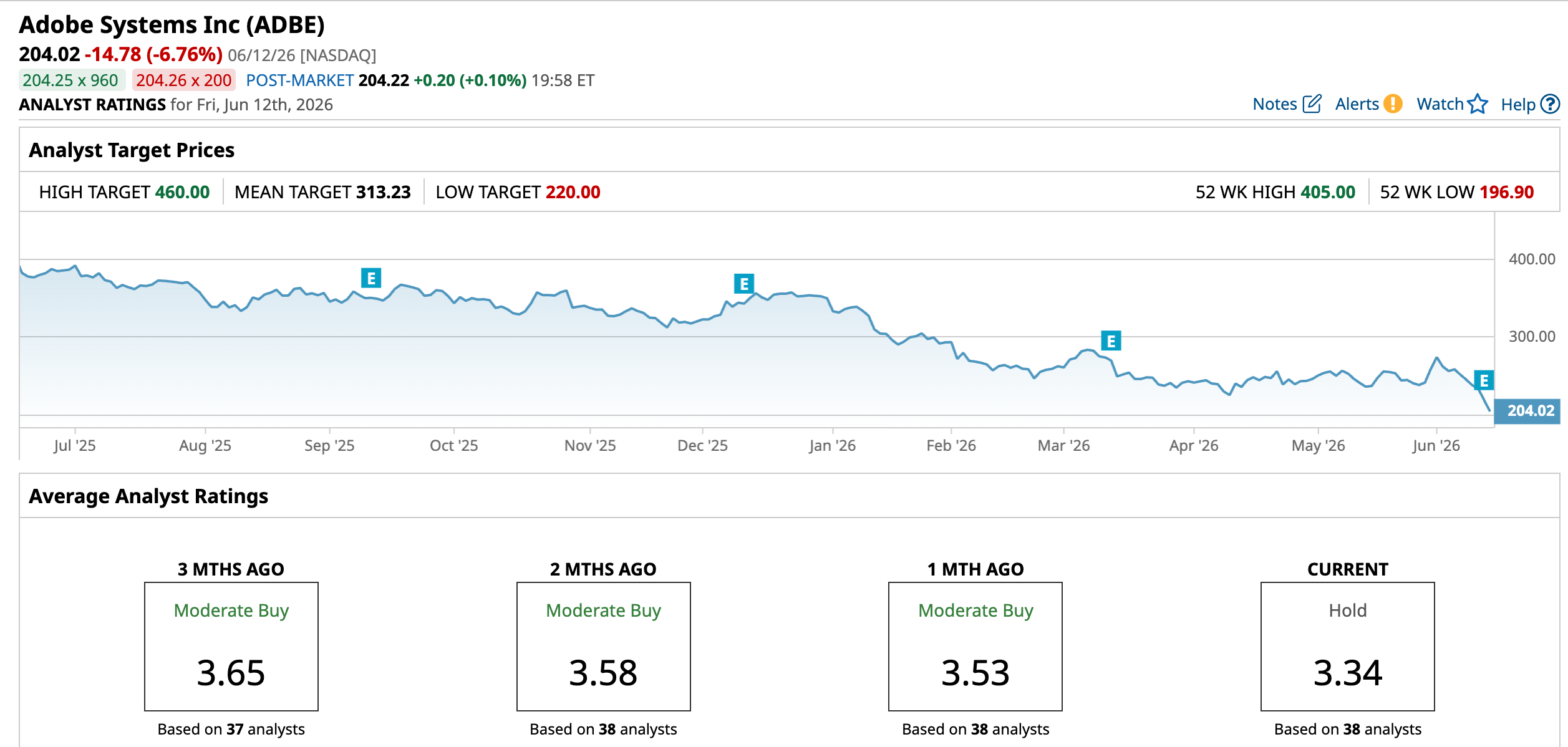

Meanwhile, Adobe’s fiscal Q2 earnings were better-than-expected, with revenues rising 13% year-over-year (YOY) to a record $6.62 billion. The adjusted earnings per share (EPS) came in at $5.96, which easily beat the $5.83 that analysts were modelling. In the current quarter, Adobe expects to post revenues between $6.67 billion and $6.72 billion, which is also ahead of estimates. The company raised its annual revenue guidance to between $26.5 billion and $26.6 billion while projecting adjusted EPS between $24.35 and $24.45. However, the earnings beat and upbeat guidance were more than overshadowed by the announcement of the CFO’s departure, and the stock is trading sharply lower this past Thursday and Friday, June 11 and 12.

In my previous article, I noted that while I am keeping ADBE on my watchlist, I did not find the stock a compelling buy yet. With Adobe now falling to a seven-year low, let’s revisit the stock’s forecast.

Should You Buy ADBE Stock?

Adobe is currently in a leadership transition phase and is headhunting for both a CEO and a CFO. While leadership transitions add a layer of uncertainty and jitteriness among investors, I believe Adobe stock looks like a buy at these levels. Here’s my bullish thesis for the embattled stock.

Subscription Revenues: Adobe boasts significant recurring revenues through subscriptions. It reported an annualized recurring revenue (ARR) of $27.1 billion at the end of the quarter ending May, with the number rising 12.5% compared to the same time last year. The company is pivoting to a freemium model and expects it to be a headwind for ARR growth in the short term, but is still optimistic about delivering double-digit growth in the metric. A Strong Moat and Creative Ecosystem: These two features are difficult to emulate. The company has largely held its ground against free and cheaper alternatives on the back of its ecosystem. Adobe has been the default choice for many creators. Deep Value Play: Adobe trades at a forward price-to-earnings (P/E) multiple of 11.43 times while the P/E-to-growth (PEG) multiple is 0.98 times. While there are some genuine concerns about the disruption caused by AI, the stock appears as a deep value play. Notably, Adobe is a cash flow powerhouse and generated operating cash flows of $2.17 billion in fiscal Q2. Its balance sheet is also strong with virtually no net debt, which gives it the freedom to repurchase shares. These buybacks further support EPS growth by lowering the outstanding share count.ADBE Stock Forecast

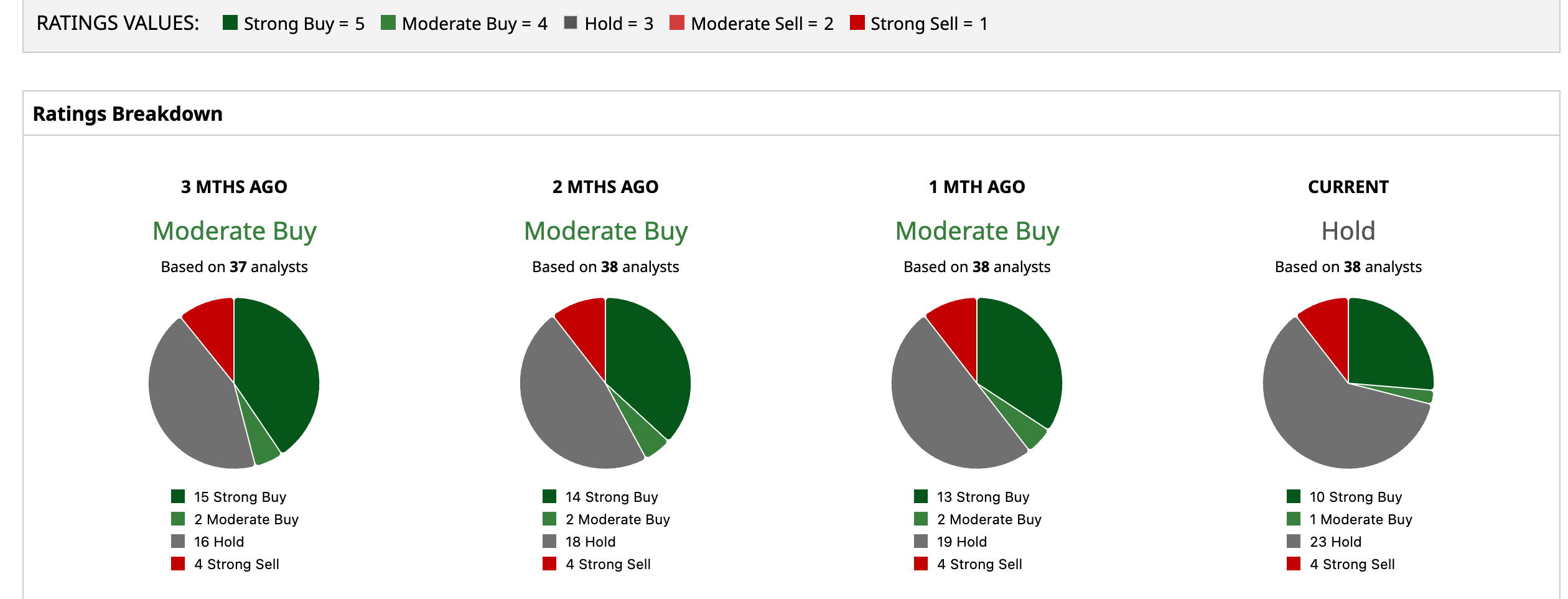

Of 38 analysts, 23 of the analysts rate ADBE as a “Hold.” Ten analysts rank it as a “Buy," with one rating it as a “Moderate Buy.” Four outliers are bearish providing a “Strong Sell.” However, in what seems a reflection of its deep value status, ADBE even trades below the Street-low target price of $190, while the mean target price of $313.23 implies 53.5% upside from here. The Street-high price point of $460 points to an upside of 125.5% for the following twelve months.

www.barchart.com

www.barchart.com https://www.barchart.com/stocks/quotes/ADBE/analyst-ratings

https://www.barchart.com/stocks/quotes/ADBE/analyst-ratingsOverall, with AI now showing signs of a bubble, perceived “AI losers” like Adobe could be good bets. The stock may be a good hedge against an AI-led sell-off, perhaps regaining favor with markets. The near-term trigger for the stock might be the appointment of a new leadership team, which could possibly formulate a strategic roadmap to revive investor confidence.

On the date of publication, Mohit Oberoi had a position in: ACN . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SpaceX's First Full Week, FOMC and Other Key Things to Watch this Week CoreWeave Just Raised $3.5 Billion. How to Play the AI Stock Here. Adobe CFO Quits to Join a Chipmaker. You Shouldn’t Quit ADBE Stock. When the AI Trade Collapses, These 3 S&P 500 Sectors Are Your Best Bet