Ford Motor Company (F) is one of the world's largest automobile manufacturers, operating since 1903. However, for much of the past several years, Ford investors have been dealing with the same frustrating story. The company boasts strong brands, dominant truck franchises, and a growing commercial vehicle business. Nonetheless, quality problems, recalls, high warranty costs, losses in the electric vehicle (EV) business, and inconsistent profitability have prevented the company from reaching its full potential.

Now, while there are signs that Ford is finally addressing some of those long-standing issues, the question remains: how long will investors have to wait to see meaningful profits?

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

www.barchart.com

www.barchart.com Ford's Biggest Problem Was Never Demand

Ford rose to prominence with its Model T and assembly-line manufacturing but is currently best known for the F-Series trucks, Mustang sports cars, Bronco SUVs, and commercial vehicle businesses. The company remains one of America's largest automakers, with dominant positions in pickup trucks, vans, and fleet vehicles.

So, demand was never the problem. But the company has failed to convert the sales to the level of profitability that investors expected. The main reason has been quality-related costs, such as warranty claims, recalls, and repairs, which have repeatedly eaten into earnings. Adjusted earnings per share (EPS) fell by 41% year-over-year (YoY) in 2025 to $1.09.

Signs of Progress Are Finally Emerging

In the most recent Q1 earnings call, management made it clear that the company believes many of those long-standing challenges are finally moving in the right direction. According to CEO Jim Farley, the strong Q1 performance reflected Ford's five-year effort to lay the groundwork for the Ford+ strategy. This plan aimed at strengthening industrial operations, improving quality, reducing costs, broadening software capabilities, and enhancing overall customer experience.

For instance, the company has deployed artificial intelligence (AI)-powered quality control systems that detect manufacturing and assembly errors in real time, allowing them to be fixed before the vehicles reach customers. Consequently, Ford expects to deliver more than $1 billion in material and warranty cost savings during 2026. In the first quarter, while revenue climbed a modest 6% to $43.3 billion, adjusted EPS showed a dramatic improvement of 371% YoY to $0.66.

Additionally, Ford Pro remains the company's most valuable asset. Despite manufacturing difficulties caused by aluminum supply challenges, the commercial vehicle division achieved $1.7 billion in EBIT during the quarter. The Ford Pro ecosystem also includes software subscriptions, which increased to 879,000 during the quarter, up 30% YoY. Ford appears to be recovering well from disruptions related to Novelis, its major aluminum supplier. This recovery could add to Ford's earnings in 2026. The company expects approximately $1 billion of YoY EBIT improvement from the recovery effort.

Looking ahead, Ford is gearing up for a major wave of product launches and updates over the next several years, with plans to overhaul 80% of its vehicle lineup across North America and 70% of its global lineup by the end of the decade. This includes future versions of key products such as the F-150 and Super Duty trucks. The company plans to do this by combining its advanced technology, software, digital, design, and manufacturing teams into a unified structure. Management believes this unified structure will develop future vehicles more efficiently while delivering a better customer experience.

The company has made headway in many areas that have disappointed investors for the last couple of years. Quality numbers are improving as warranty costs decline. Software revenue is growing, while Ford Pro remains highly profitable. Even the company’s balance sheet remains healthy with $22 billion in cash at the end of Q1. While free cash flow (FCF) was negative $1.9 billion in Q1, management predicts positive FCF of $5 billion to $6 billion for the full year. Analysts forecast Ford’s earnings to increase by 50% in 2026, followed by another 11.6% in 2027.

Additionally, income investors continue to appreciate Ford's dividend yield above 4%.

But the Hard Part Comes Next

While Ford has made progress in many areas, its EV business still faces significant challenges. Ford Model e reported an EBIT loss of $777 million in Q1. While the segment still remains deeply unprofitable, Ford continues investing aggressively in its future EV platform and Ford Energy initiatives as competition is tight in this market. Companies like Tesla (TSLA), General Motors (GM), Hyundai/Kia, Rivian (RIVN), and the rapidly growing Chinese manufacturers are competing directly for market share, pricing power, and future EV profitability.

This could test investors’ patience who are still waiting to see a clearer path of profitability in its EV business. Ford’s next phase will require it to consistently convert operational improvements into higher earnings, stronger margins, and durable shareholder value. All in all, Ford appears to be moving in the right direction, But, in my opinion, it looks more like a wait-and-watch story than an aggressive buy now.

Is F Stock a Buy Now on Wall Street?

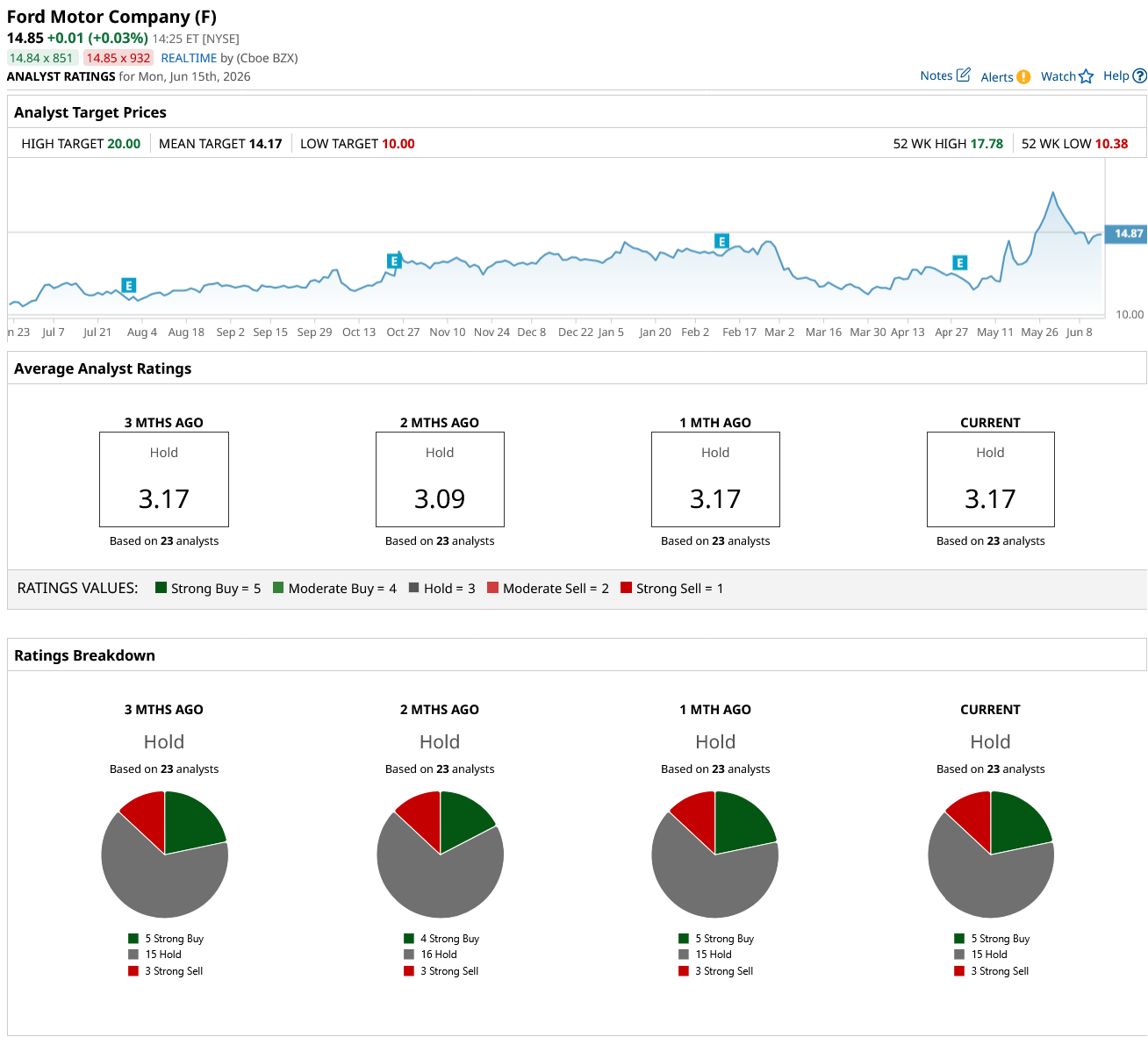

Even analysts have rated F stock a consensus “Hold.” Of the 23 analysts that cover the stock, five rate it a “Strong Buy,” 15 say it is a “Hold,” and three recommend a “Strong Sell.” While F stock has climbed just 14% year-to-date (YTD), the stock has climbed over 11% in the past month alone, surpassing its average target price of $14.17. However, the high price estimate of $20 implies the stock can climb by 35% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Ford Is Fixing Its Biggest Problems. The Hard Part Comes Next. Beijing Rebukes Alibaba and JD.com Over Misleading Discount Practices. How to Play Leading Chinese Stocks Here. A Major Short Squeeze Could Be Brewing in Cracker Barrel Stock A $1.24 Trillion Reason to Buy Dell Stock Now