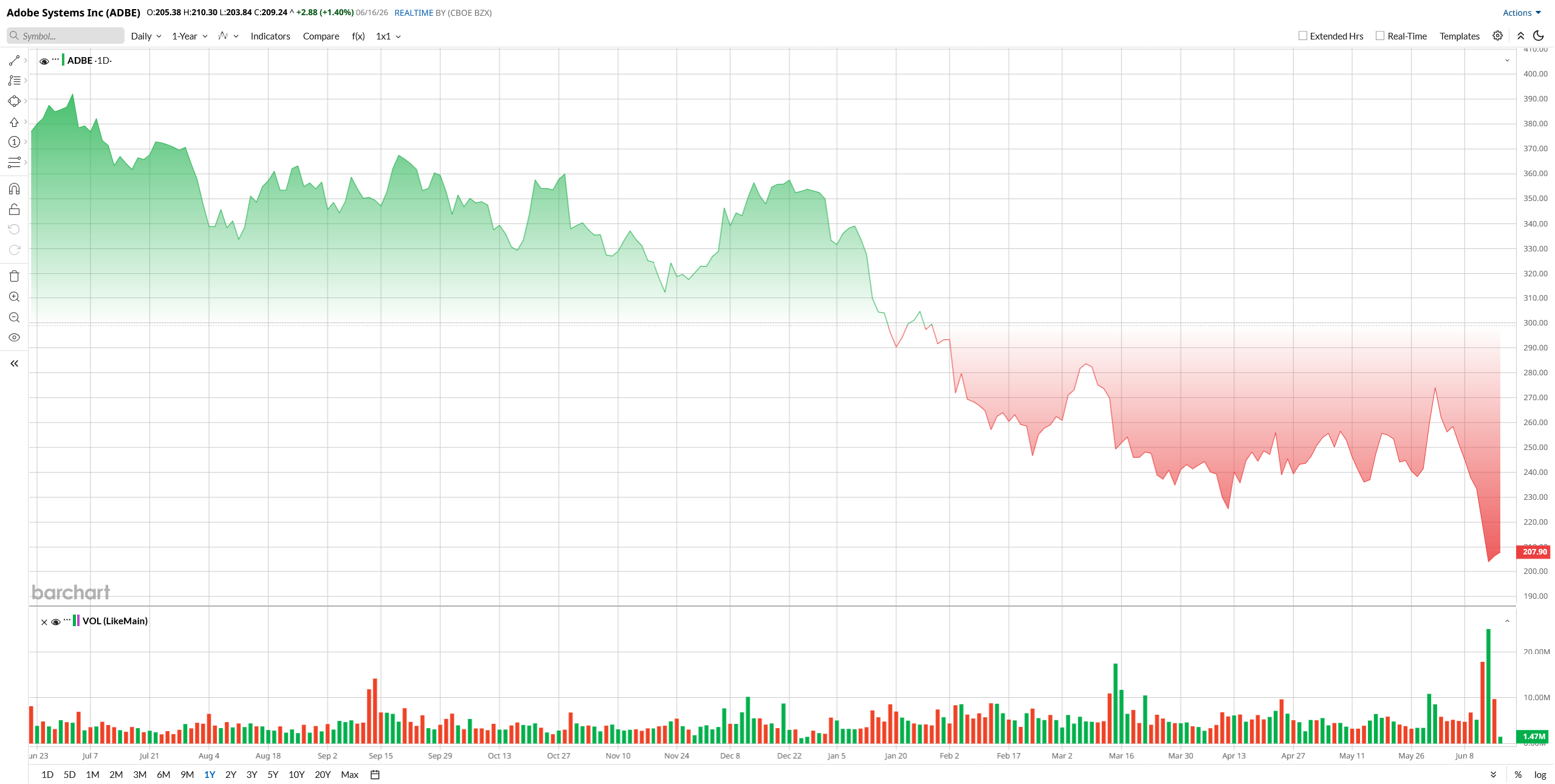

The software giant Adobe (ADBE) just posted a solid fiscal second quarter, even lifting guidance, but the stock still sank to its 52-week low as investors focused less on the beat and more on the surprise CFO shakeup.

ADBE stock plunged about 7% on Friday right after earnings, with the market reacting to news that CFO Dan Durn will step down in mid-June, while concerns about rising AI competition and slowing momentum kept pressure on the stock

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For traders, the setup is now simple: Adobe is a beaten-down quality name with strong fundamentals, but sentiment is still fragile. The question is whether Q2 earnings marked a real turning point or just a relief rally inside a bigger downtrend.

Stock Weakness Has Created a Tradeable Setup

The recent sell-off brought the stock down to about 40% year-to-date (YTD), which is significantly lagging the broader market index, which rallied by double digits during the same time period. Adobe's underperformance came due to a mix of growth fears, AI competition, and leadership uncertainty.

Investors have grown more cautious as newer rivals like Figma (FIG) and Canva continue to pressure the creative software market, while fresh AI tools are also raising questions about how defensible Adobe’s core franchise really is.

Despite the weakness, Adobe’s valuation has become far more compelling. The stock trades at about 11.7 times trailing earnings, which is far below the roughly 80 times sector median. Its PEG ratio is around 0.85, another sign that growth expectations may have been marked down too aggressively.

That said, ADBE is not cheap on every metric. Its price-to-book ratio sits near 7.35, which still reflects a premium franchise and a market that is paying for quality even after the selloff. In other words, the stock looks inexpensive on earnings and growth, but not on asset value. That combination often attracts traders looking for a rebound, especially after a strong earnings beat.

www.barchart.com

www.barchart.com Q2 Earnings Show the Business Is Still Growing

Despite the reaction, Adobe’s latest quarter, which ended May 29, was clearly a strong one. Revenue hit a record $6.62 billion, up 13% year-over-year (YoY), while EPS came in at $5.96, topping the $5.82 consensus estimate.

The company also delivered robust cash generation. Net income reached $2.40 billion, and operating cash flow was about $2.17 billion. Both of Adobe’s major business divisions posted healthy growth. Annualized recurring revenue also topped $27.10 billion.

A big part of the quarter came from the newly acquired Semrush platform, which contributed about $480 million. That helped widen Adobe’s reach in digital marketing and visibility tools, reinforcing the company’s move beyond pure creative software.

Looking ahead, Adobe provided a stronger-than-expected outlook for both the third quarter and the full fiscal year.

For fiscal Q3, the company expects adjusted earnings of $6.05 to $6.10 per share, exceeding analysts' consensus estimate of $5.77 per share. Revenue is projected to range between $6.67 billion and $6.72 billion, ahead of the $6.52 billion forecast by analysts.

For the full fiscal year, Adobe raised its guidance and now expects adjusted earnings of $24.35 to $24.45 per share. The midpoint of this range is above the Wall Street consensus estimate of $23.54 per share.

Adobe Is Still Building Beyond the Core

Outside the quarter, Adobe has been busy reshaping its platform. The company completed its $1.9 billion Semrush acquisition in April 2026, adding SEO and brand-visibility tools to its marketing cloud. It also rolled out new AI-based products, including its Adobe CX Enterprise platform, as it pushes deeper into the “agentic” AI era.

At the same time, the company approved a massive $25 billion buyback plan and repurchased about 8.5 million shares during the quarter. That is a clear signal that management believes the stock is undervalued and that cash flow remains solid.

One more major change is on the horizon as CEO Shantanu Narayen has said he will step down once a successor is in place. That adds another layer of uncertainty, even as the company keeps leaning into AI-led growth.

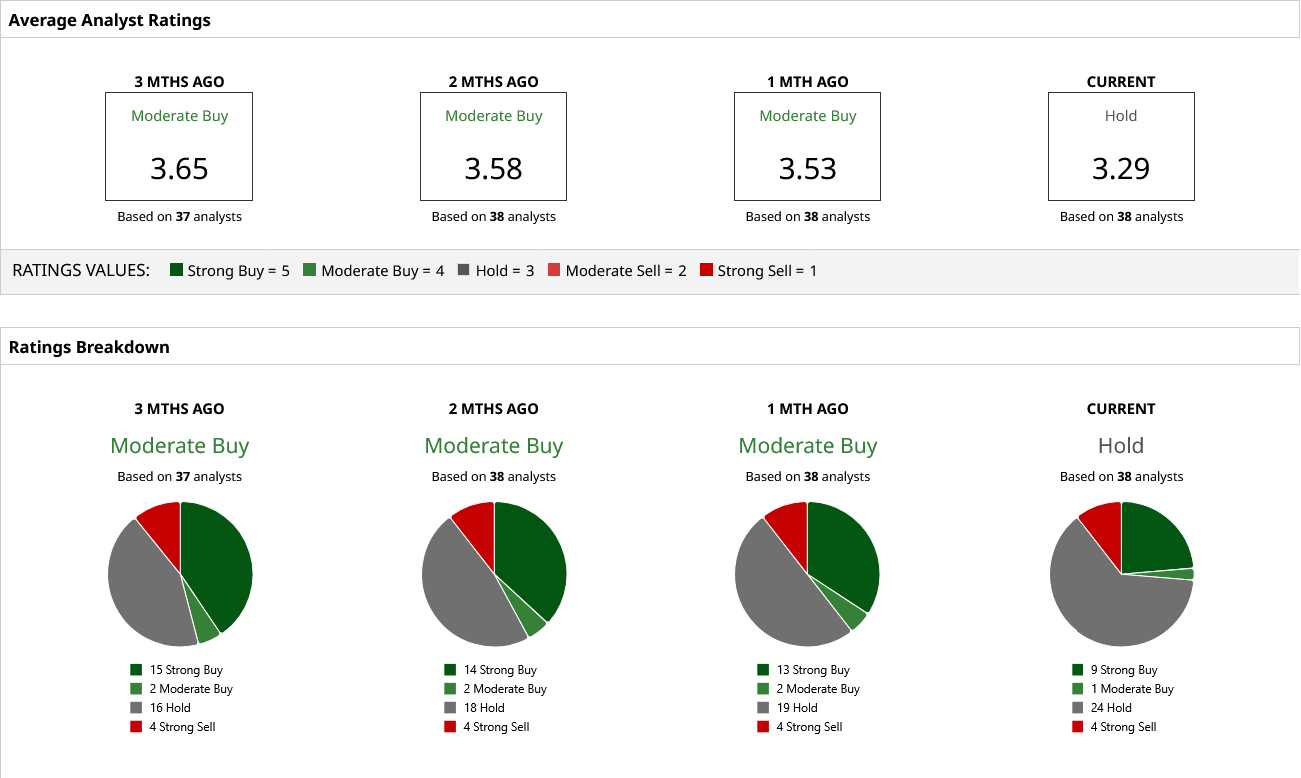

Wall Street Opinion on ADBE Stock

Analysts remain cautious overall. Goldman Sachs recently cut ADBE to “Sell” with a $290 target, pointing to slower growth and AI-related competition. Mizuho downgraded the stock to “Neutral” and reduced its target to $270, while KeyBanc also turned more defensive with a $310 target.

Still, not everyone is bearish. RBC Capital remains bullish with a target near $400, and Bernstein is even more optimistic at around $506. The consensus rating is roughly “Hold,” with an average 12-month target near $277.48, which implies meaningful upside of 33% from current levels if Adobe can keep execution on track.

In my opinion, Adobe now looks like a classic post-earnings battleground stock: weak technically, cheap on earnings, and supported by solid fundamentals. The next move will likely depend on whether management can prove that AI, buybacks, and new product launches are enough to restore growth confidence.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Lesser-Known Stock Is a ‘Bunker’ for Your Capital Thanks to Technical Strength The Battle of the Musks: Why Cathie Wood Sold Tesla Stock to Buy SpaceX The Dell Story Is No Longer Just About PCs. Here’s Why the Stock Still Looks Undervalued. CVNA Stock Alert: What to Know as Carvana Expands Into New Vehicles