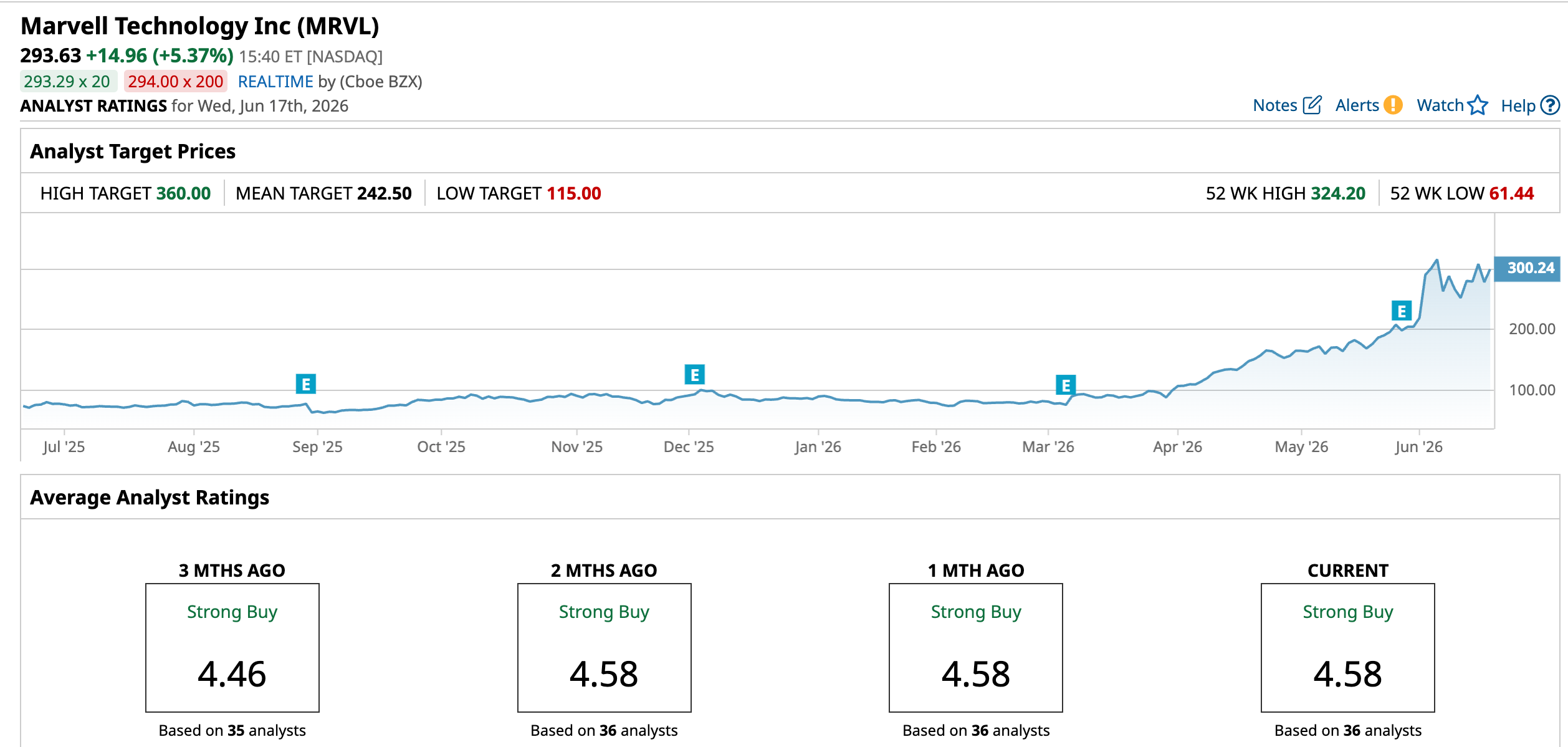

Shares of Marvell Technology (MRVL) have rallied strongly, up 258% year-to-date (YTD). Strong demand and bookings for its data center products, such as interconnect, custom AI chips, and switching, have accelerated its growth, supporting MRVL stock.

Adding to the excitement around the stock, Nvidia CEO Jensen Huang publicly said that Marvell could represent “the next trillion-dollar opportunity.”

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

But after such a massive run, will Marvell's fundamentals continue to support the stock's rise?

www.barchart.com

www.barchart.com Strong Results Point to Accelerating Demand

Marvell’s latest earnings report suggests its growth trajectory remains solid. Marvell’s top line increased 28% year-over-year (YOY) to $2.42 billion in the first quarter of fiscal 2027, while adjusted earnings per share (EPS) climbed 29% to $0.80.

The company reported exceptionally strong bookings across its data center portfolio, indicating that customers continue to expand their investments in AI-related infrastructure. Further, management’s guidance reflects this confidence. For the current quarter, Marvell expects revenue to rise 12% sequentially and 35% YOY. Data center revenue, the company’s largest growth engine, is projected to increase sequentially in the mid-to-high teens and YOY by approximately 45%. The guidance points to accelerating momentum rather than a moderation in demand.

Data Center Business Continues to Fire on All Cylinders

One of the biggest growth drivers is Marvell's interconnect business, which enables high-speed data movement within AI data centers. Management now expects this business to grow more than 70% YOY in fiscal 2027, significantly above its previous forecast of roughly 50%. The upgrade reflects rising demand for networking technologies that connect increasingly complex AI systems.

Marvell is also benefiting from the growing adoption of custom AI chips and Ethernet switching products. Management said it now has visibility into more than $10 billion in annual custom silicon revenue by fiscal 2029, highlighting the scale of the opportunity ahead.

Marvell Keeps Raising Its Forecasts

Marvell once again raised its long-term expectations, which supports its investment case. Earlier this year, management projected quarterly revenue would approach $3 billion by the end of fiscal 2027. It now expects to reach that milestone by the third quarter instead.

Additionally, the company increased its expected sequential growth rate for the second half of the year to at least 10%, up from its previous forecast of 8%.

As a result, Marvell now expects fiscal 2027 revenue to grow roughly 40% YOY to nearly $11.5 billion, compared with its prior outlook of approximately $11 billion. Data center revenue is expected to increase by 50% this year.

Looking further ahead, management expects data center revenue growth to accelerate again in fiscal 2028 to roughly 55%. The company's custom silicon business is projected to more than double, while Ethernet switching revenue continues to ramp.

Overall, Marvell now forecasts fiscal 2028 revenue of approximately $16.5 billion, up from its earlier estimate of about $15 billion. Notably, this marks the second major upward revision in a relatively short period, suggesting customer demand is strengthening.

The Biggest Risk for MRVL Stock: Valuation

Despite the impressive growth outlook, investors should not ignore valuation risk. After gaining 227% this year, Marvell trades at 100.49 times forward earnings and a price-to-sales ratio of 27.66 times. Those are premium multiples, suggesting the market has already priced in a significant portion of the company's expected growth.

Marvell's earnings are projected to rise more than 42% in fiscal 2027, with EPS growth accelerating to 66.5% in fiscal 2028. In other words, Marvell may need to deliver results well above current forecasts to justify its lofty valuation and sustain its recent momentum.

The Bottom Line

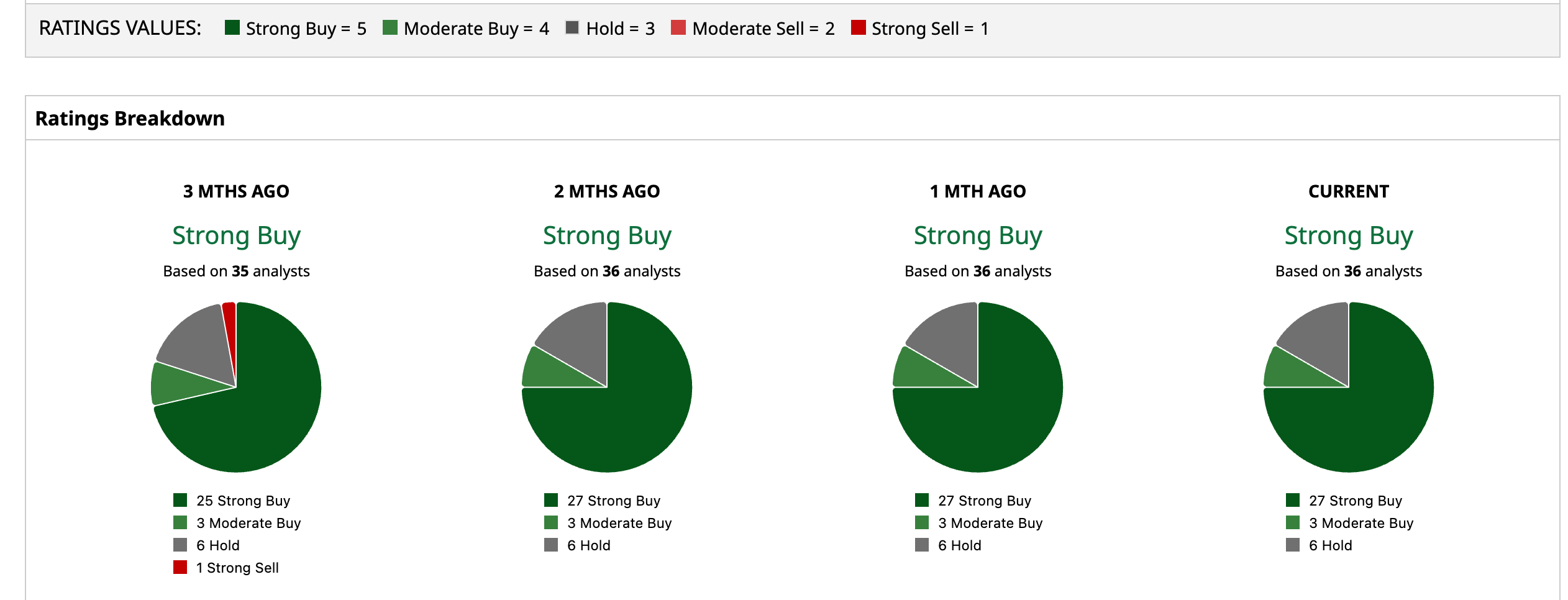

Marvell’s growth trajectory remains solid, led by data center products. It will continue to benefit from AI infrastructure spending, strong bookings, and the expansion of its custom AI chip business. Analysts are also bullish about its prospects and maintain a “Strong Buy” rating.

However, its high valuation could limit the upside potential in MRVL stock.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

INTC Stock Alert: Intel to Begin Production of Its Most Advanced Chip Marvell Stock Soars 228% This Year. Data Center Momentum Is Still Hot, But Future Upside May Be Limited. RIVN Stock Layoffs: What to Know About the Latest Rivian Job Cuts How Barchart Helped Me Make a Big Return on an Options Trade in Just 24 Hours. It Can Help You Too.