Accenture (ACN) closed meaningfully lower on June 18 after the technology consulting company missed Q3 revenue estimates and issued disappointing guidance for the future. The stock has continued its decline today.

In its third financial quarter, ACN earned a better-than-expected $3.8 per share on a 5.6% increase in revenue to $18.7 billion.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

But investors were more spooked by management’s guidance for a $18.07 billion in revenue in the current quarter — firmly below the $18.47 billion that analysts had forecast.

Year-to-date, Accenture stock is now down more than 50%, but the derivatives market seems to believe it could tumble further as the year unfolds.

www.barchart.com

www.barchart.comWhere Options Data Suggests Accenture Stock Is Headed

According to Barchart, the put-to-call ratio on ACN options contracts expiring mid-July sits at 1.04x currently, indicating a strong bearish skew.

The lower price on those contracts is set at $116 roughly, signaling the professional services firm could remain in a downtrend and lose another 9% over the next four weeks.

Note that Accenture is now trading below its key moving averages (MAs), with an RSI in the early 20s reinforcing intense selling pressure.

In fact, Barchart’s “100% SELL” opinion on ACN shares substantiates that technical momentum indeed favors continued downside ahead.

Why ACN Shares Aren’t Attractive to Buy on the Dip

Beyond headline numbers, a closer look at Accenture’s Q3 operational data reveals early cracks in enterprise demand.

New bookings slipped 2% year-over-year to $19.32 billion, highlighting a prolonged pullback in discretionary corporate IT spending.

Crucially, management disclosed that several large, high-margin managed services deals have been delayed until fiscal 2027, significantly hurting near-term revenue visibility.

Compounding these structural headwinds is a $4.17 billion M&A spending spree to acquire OT cybersecurity assets like Dragos.

Investors are punishing Accenture shares over fears that these huge cash outlays will depress near-term profitability while introducing high integration risks into a softening market.

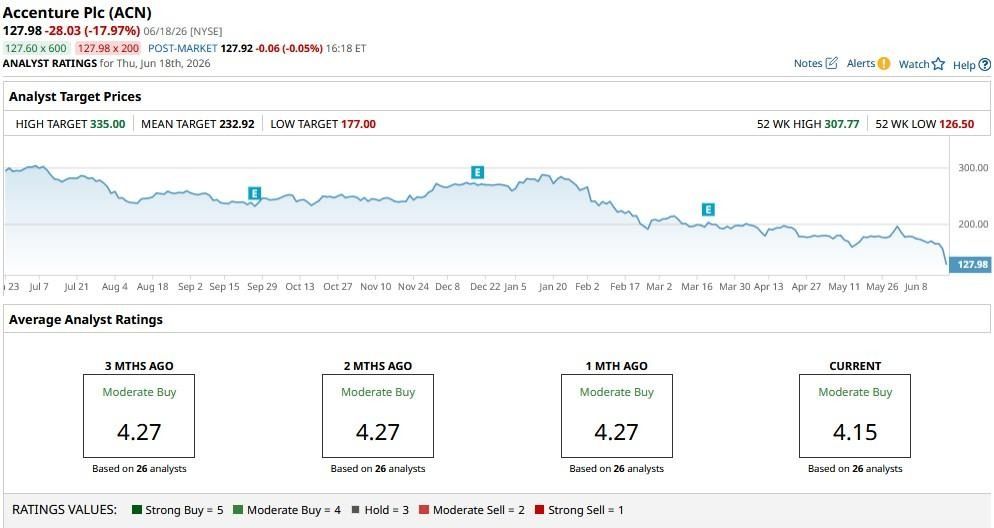

Accenture Remains Buy-Rated Among Wall Street Firms

Despite a weak Q3 print and bearish options pricing, Wall Street remains bullish on ACN stock.

The consensus rating on Accenture is currently “Moderate Buy,” with a mean price target of about $233 indicating potential upside of more than 80% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A New Chip Partnership Between Apple and Intel Is a Long-Term Catalyst for AAPL Stock Following Disappointing Accenture Earnings, Here's What Barchart Data Says Comes Next for ACN Stock The Smart Money Agrees That Seagate Stock Still Has Room to Surge Higher Barclays Just Upgraded Enphase Energy. Here's Why.