While Meta Platforms (META) has been quite aggressive with its artificial intelligence (AI) efforts and, apart from bumping up capex, it has been on an acquisition and talent hiring spree, the markets haven't been too convinced about its AI strategy. While the company was seen as an early winner as its core business’s growth picked up due to AI initiatives, over the last few months it has been trying to shed the impression that it does not have a coherent AI strategy.

As early Facebook investor Chamath Palihapitiya told Axios, Meta “profoundly failed” and “fumbled” its early AI advantage. I would somewhat agree with that statement, even though the AI race is far from over, and it would be too early to pick winners and losers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Hyperscalers Are Spending Aggressively on AI

U.S. tech giants, particularly the hyperscalers, have been spending on building AI infrastructure as if there’s no tomorrow. Specifically, Meta Platforms raised its 2026 capex to between $125 billion and $145 billion at the last count. At the top end of the guidance, Meta would spend around 57% of its expected 2026 revenues on capex, which, for context, is the highest among hyperscalers, even though in absolute terms Amazon (AMZN) has the highest capex budget this year.

However, unlike other hyperscalers, Meta does not have a cloud business, which is booming due to AI. The growing cloud revenues help tech giants validate their AI capex to some extent as investors correlate that growth with the burgeoning spending to build AI infrastructure.

Meanwhile, a sagging stock price seems to have triggered a state of urgency at Meta, as I noted in my previous article. The company has been announcing a flurry of AI initiatives that would help it justify its capex.

Meta Raises Its Game in AI

In the most recent instance, it has released Muse Spark 1.1, which is capable of coding and agentic tasks. The company has priced the access at $1.25 per million input tokens and $4.25 per million tokens of output.

Earlier this month, Bloomberg reported that Meta is planning to launch a cloud business to see excess compute capacity. While that report hasn’t been confirmed, in the past, Meta CEO Mark Zuckerberg has touted the possibility of launching a cloud computing business. Reports suggest Meta plans to release a prediction market app, which would be powered by what else but AI. Additionally, the company is testing two subscriptions for its AI offerings and has priced Meta One Plus at $7.99 a month and Meta One Premium at $19.99 a month. Meta also has a new CEO for WhatsApp, and we can be reasonably sure of more monetization strategies for the messaging app.

These initiatives haven’t gone unnoticed in the sell-side analyst community, and earlier this month Erste Group upgraded the stock from a “Hold” to “Buy,” as it expects Meta's aggressive AI investments will drive the company’s revenue and profit growth.

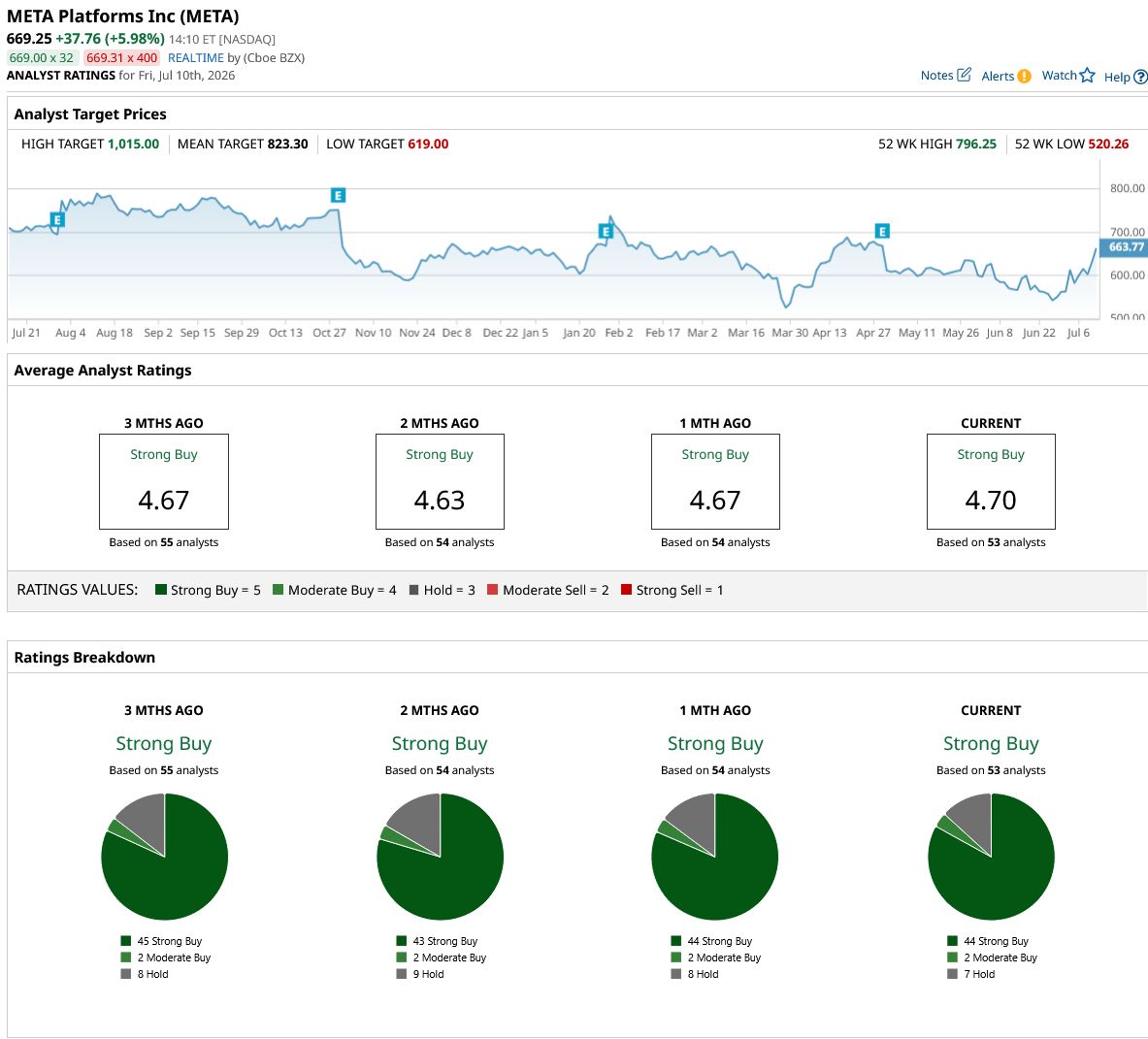

Overall, META stock has a consensus rating of “Strong Buy” from the 53 analysts polled by Barchart, while its mean target price of $823.30 is 23% higher than current price levels.

www.barchart.com

www.barchart.com Key Risks Meta Investors Should Watch

All said, there are several risks that Meta investors should watch out for. The first is the growing global clamor to ban social media for kids. On July 10, in its preliminary report, the EU Commission concluded that Meta was in violation of the Digital Services Act due to the “addictive” features on Facebook and Instagram.

In the U.S., a Los Angeles jury found in March that Meta and YouTube were negligent in protecting children on their platforms—and deliberately structured their platforms to make them addictive. On a related note, states are seeking $1.4 trillion from Meta, alleging that the company intentionally makes its apps addictive for kids. While Meta dismissed that number as “outlandish” during the Q1 2026 earnings call, CFO Susan Li had said, “We continue to see scrutiny on youth-related issues and have additional trials scheduled for this year in the U.S., which may ultimately result in a material loss.” Then there is the raging debate over Section 230, which provides immunity to platforms like Meta for the user-generated content that they host.

All said, I believe a company like Meta will always be prone to regulatory risks. However, given the stellar growth the company’s core business is experiencing and the flurry of monetization steps it has announced in recent weeks, I remain bullish on META stock and find it attractive at a forward price-to-earnings (P/E) multiple of around 21x.

On the date of publication, Mohit Oberoi had a position in: META , AMZN . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Meta Has Raised Its AI Game. The Stock Should Continue to Rise In 2026. Marvell’s Hidden Growth Engine Just Achieved a Major Milestone That the Market Hasn’t Priced In Yet Huge Earnings, Inflation Data and Other Key Things to Watch this Week Netflix Is Losing Viewers To The World Cup. That May Be The Wrong Measure Of The Business.