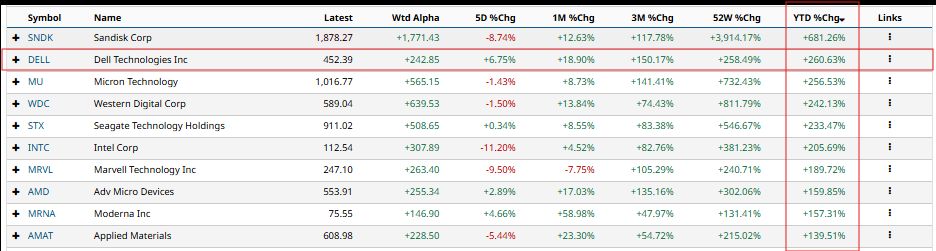

Dell Technologies (DELL) is one of the biggest winners of the artificial intelligence (AI) infrastructure boom, with its stock outperforming many AI chipmakers and memory hardware companies this year.

Shares of Dell have climbed more than 250% year to date (YTD), driven by soaring demand for its AI-optimized servers as enterprises and hyperscale cloud providers ramp up spending on next-generation AI infrastructure.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Despite this remarkable rally, Dell's growth story may be far from over. Strong AI server demand, a rapidly expanding order backlog, and a valuation that remains attractive relative to its growth prospects suggest the stock could have additional upside.

www.barchart.com

www.barchart.com Why Dell’s AI-Driven Growth Story Is Far From Over

Dell delivered one of the strongest quarters in its history, highlighting that enterprise spending on AI infrastructure remains robust across industries and geographies. Dell’s first-quarter revenue rose to $43.8 billion, representing 88% year-over-year (YoY) growth. Moreover, its adjusted net income soared 194%.

Looking ahead, the momentum in its business is likely to continue, driven by Dell’s Infrastructure Solutions Group (ISG). Notably, the segment’s revenue soared 181% YoY to $29 billion. During the quarter, Dell generated $24.4 billion in AI infrastructure orders and delivered $16.1 billion in AI server revenue, up 757% from a year earlier.

The strongest indicator that Dell's AI growth story is still in its early stages is its record backlog. The company ended the quarter with $51.3 billion in AI orders awaiting fulfillment. Further, customer demand continues to outpace supply, while Dell’s AI opportunity pipeline is several times larger than the existing backlog. This visibility provides confidence that Dell’s revenue growth should remain strong over the coming quarters.

Importantly, demand is becoming increasingly diversified. Dell now serves more than 5,000 AI customers, with growth spanning enterprise customers, neocloud providers, and sovereign AI initiatives. A broader customer base reduces concentration risk while demonstrating that AI adoption is expanding well beyond hyperscalers.

Dell's traditional infrastructure business also remains healthy. Revenue from conventional servers increased 92% YoY, supported by enterprise hardware refresh cycles and rising computing requirements. As AI inference workloads become more widespread, they are also driving incremental demand for traditional servers, creating another strong avenue for sustained growth.

Management's updated guidance further supports Dell’s investment case. Dell projects fiscal 2027 revenue of $165 billion to $169 billion, significantly above its previous outlook of $138 billion to $142 billion. The company also projects AI server revenue of roughly $60 billion and expects adjusted earnings per share (EPS) to rise 74% to $17.90.

Wall Street’s forecast also indicates strong earnings growth ahead. Analysts expect Dell to report EPS growth of 91.8% this fiscal year, followed by another double-digit growth next year.

Overall, Dell's accelerating AI demand, record backlog, diversified customer base, and solid earnings outlook suggest its AI-driven growth story is far from over.

Valuation Still Looks Attractive

Despite the rally, Dell's valuation remains compelling when viewed alongside its growth outlook. The company is well-positioned to deliver robust earnings growth as demand for AI infrastructure and enterprise technology continues to expand.

Dell currently trades at approximately 23.5x forward earnings, a multiple that appears attractive relative to its expected earnings growth. Meanwhile, its price-to-sales (P/S) ratio of 2.38x also looks reasonable given its strong revenue and profit expansion potential.

DELL Stock to Sustain Upward Trajectory

Dell is one of the top beneficiaries of the accelerating AI infrastructure investment cycle. Its record AI server demand, expanding order backlog, diversified customer base, and strengthening earnings outlook point to a business that is still in the early stages of monetizing a multi-year AI spending wave.

While DELL stock's exceptional rally may lead to periods of volatility or profit-taking, the company's execution and improving long-term visibility continue to support a constructive investment outlook.

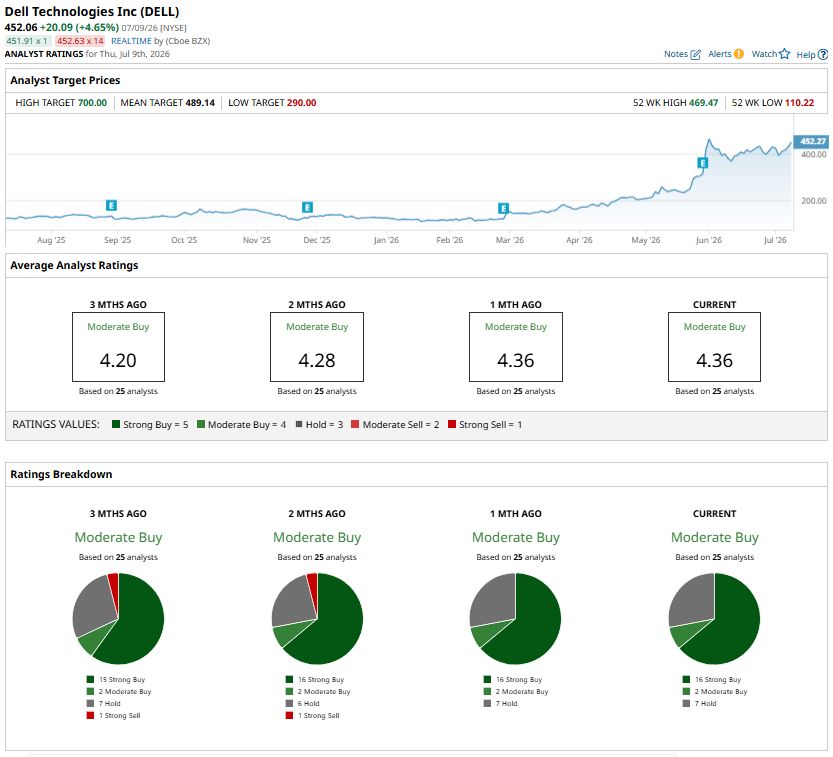

Overall, Dell appears well-positioned to sustain above-average growth, making it a compelling AI infrastructure play. Analysts maintain a “Moderate Buy” consensus rating on DELL stock.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dell Is Winning the AI Infrastructure Race. Here’s What Comes Next After a 250% YTD Rally. Option Volatility And Earnings Report For July 13 - 17 Stocks Set to Open Lower as SK Hynix Sparks Chip Selloff, U.S. Inflation Data and Big Bank Earnings Awaited Forget GPUs. Nvidia’s Next AI Gold Mine Could Be Even Bigger.