Financial services major Wells Fargo has upgraded the shares of hard disk drive (HDD) maker Seagate (STX) to “Overweight,” citing strong demand and average selling price accretion in the coming times. Notably, the price target of $1,100 implies a potential upside of 27% from current levels.

Along with continued visibility in demand, strong free cash flow generation was another tailwind that the broker reckons is working in favor of the company.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Seagate

Tracing its origins to the late 1970s, Seagate is one of the world's two dominant manufacturers of HDDs and a critical supplier of mass-capacity storage to cloud and hyperscale data centers. Alongside Western Digital (WDC), Seagate sits at the center of the global HDD industry. Its products are used in hyperscale cloud data centers, enterprise storage, network-attached storage, video and image applications, and consumer devices.

Valued at a market cap of $204.1 billion, STX stock has exploded this year with a rally of 215% on a year-to-date (YTD) basis. Further, the stock offers a dividend yield of 0.33%.

The bullishness in the wider memory sector certainly helped in STX's rally. However, apart from Wells Fargo's primary reasons for optimism, what makes the investment case for Seagate? Let's find out.

www.barchart.com

www.barchart.com One for the Masses

Seagate's storage devices are quite popular among consumers, with many owning their HDDs. The company's major product families include Exos enterprise drives, IronWolf NAS drives, SkyHawk video and surveillance storage, and FireCuda gaming storage. It also owns the LaCie premium storage brand. However, the demand for memory for the AI infrastructure buildout has made the sale of mass-capacity storage to cloud and data center customers its primary growth driver.

Hyperscalers may require DRAM and NAND for inference and training, and for fast storage, respectively, but what about the storage of the massive volumes of data generated by these companies? This is where HDDs come in, offering low-cost mass storage. And here, it is essentially a duopoly, with Seagate cornering 40.8% of the market, trailing its counterpart, Western Digital's 42.3% share.

So, why do hyperscalers flock to these two? Well, economics is certainly a consideration, but Seagate offers something more than that. Its focus on area density, which means packing in more storage in a single device, rather than going for the volume play of selling more hard drives, is the key play here. Its ability to cram more capacity into the same physical drive means a hyperscaler can store an exabyte while using fewer racks, less floor space, and less power

Seagate quantifies this in its own testing, saying that a one exabyte Mozaic deployment improves infrastructure efficiency by roughly 47% compared with standard 30TB drives, trims data center footprint by about 100 square feet, and cuts annual energy use by around 0.8 million kilowatt-hours.

Underpinning all of this is HAMR, or heat-assisted magnetic recording, which briefly heats the disk surface with a tiny laser so bits can be written more tightly and packed at far higher areal density than older recording methods allowed. Mozaic is simply the productized platform built around HAMR, bundling the laser, a new suspension design, and a custom system-on-a-chip.

Speaking of Mozaic, Seagate announced the Mozaic 4+ platform in March 2026. It is the industry’s only HAMR-based storage platform deployed at scale, and Seagate confirmed it is already qualified and in production with two leading hyperscale cloud providers, shipping in volume at capacities up to 44TB. This is a meaningful step up from the prior 30TB class Mozaic 3+ generation.

Encouragingly, Seagate does this without a disruptive architectural overhaul. Each generation layers on a next-generation suspension design and an enhanced system-on-chip that enables precise recording at higher densities while maintaining enterprise-like reliability, so customers can keep scaling capacity without ripping out and requalifying entirely new systems. That continuity matters enormously to hyperscalers who dread costly qualification cycles.

Finally, for its future roadmap, Seagate is keeping it simple but effective. Today’s 4+TB per disk will pave the way for a future 10TB per disk, which would unlock drives of up to 100TB, and additional customer qualifications are already underway. The strategic logic behind this is that as AI floods data centers with training sets, historical archives, and increasingly heavy multimodal outputs like video, hyperscalers need somewhere economical to park it all, and denser drives deliver more capacity per rack and per watt.

Seagate's Q3 Joy

Seagate's numbers for Q3 2026 were solid, with both revenue and earnings surpassing estimates and reaching record levels.

Revenues for the quarter were at $3.1 billion, up 41% from the previous year. Earnings more than doubled in the same period to $4.10 per share, outpacing the consensus estimate of $3.52 by some margin. Notably, this was the ninth consecutive quarter of earnings beats from the company.

For Q4 2026, the company expects revenue and earnings to be in the ranges of $3.35 to $3.55 billion and $4.80 to $5.20 per share, respectively. Analyst expectations for the same are at $3.39 billion and $4.73 per share, respectively.

Further, cash flow from operations continued to grow at an impressive rate, too. For the nine months ended April 3, 2026, Seagate's net cash flow from operating activities stood at $2.4 billion, up from $575 million in the year-ago period. Overall, the company closed the quarter with a cash balance of $1.1 billion, with short-term debt of $398 million.

However, such a stark rally in share prices comes at the altar of overvaluation generally. And that is the case with STX as well. The stock is trading at a forward P/E, P/S, and P/CF of 61.11, 17.09, and 58.75, compared to the sector medians of 25.02, 3.39, and 18.99, respectively.

Analyst Opinion of STX Stock

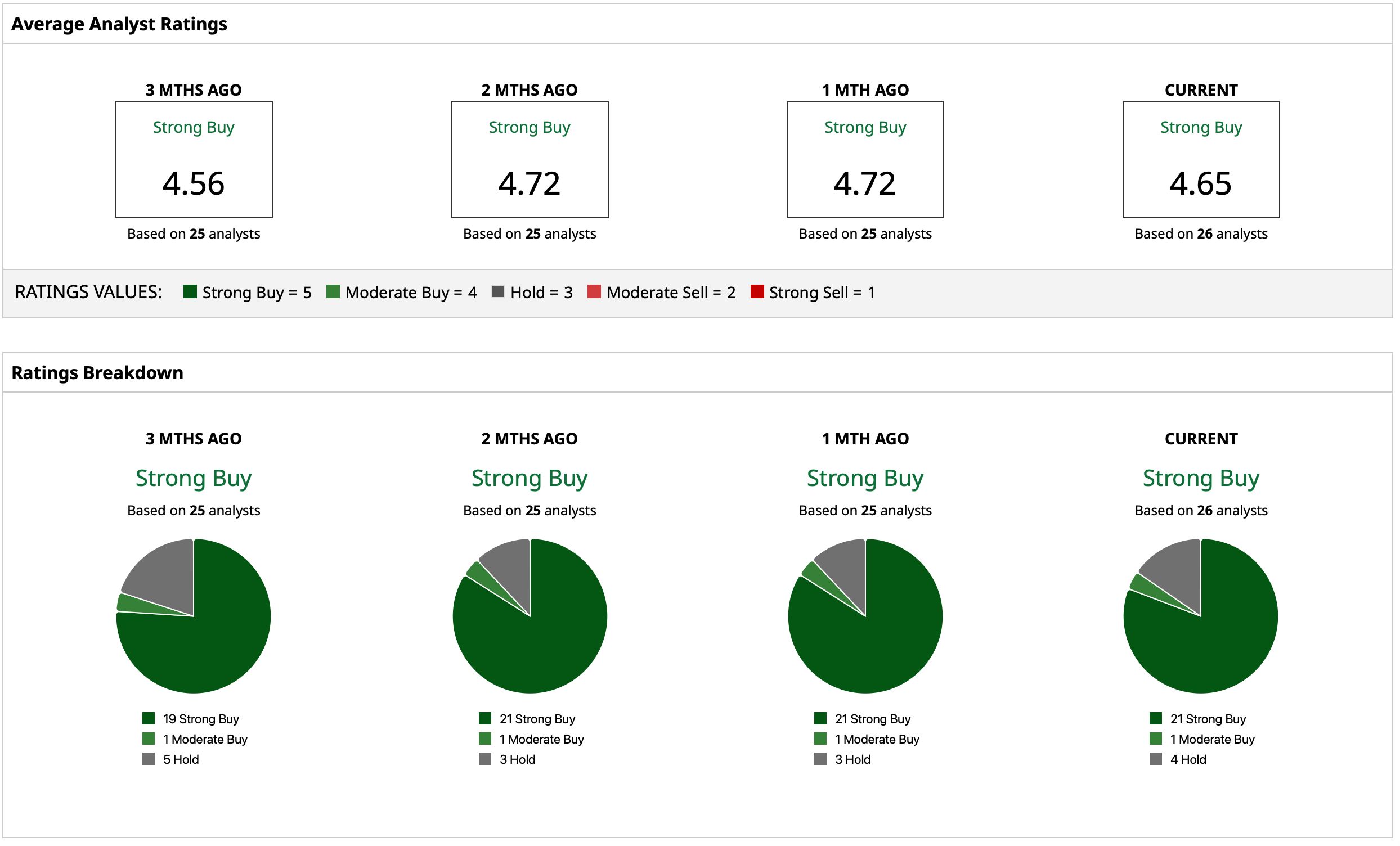

Overall, analysts have assigned a rating of “Strong Buy” for STX stock, with a mean target price of $981.30. This denotes a potential upside of about 13% from current levels. Out of 26 analysts covering the stock, 21 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and four have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Delta Air Lines Could Be a Top Stock to Buy for the Rest of 2026 Why Analysts Are Betting Western Digital Stock Can Gain Another 30% from Here COIN Stock Alert: 3 Reasons Why Coinbase Shares Are In Focus A New Report Says Meta Platforms Could Overtake Google AI. How to Play META Stock Here.