Yesterday’s markets edged higher with all the major indexes in positive territory on the day.

The S&P 500 was up 0.4%, 0.5% from an all-time high, thanks to strong earnings from Morgan Stanley (MS). Meanwhile, the Nasdaq Composite gained 0.6% on decent moves by Alphabet (GOOGL), Apple (AAPL), and ASML (ASML).

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

A stock that did not have a good day was Advance Auto Parts (AAP), the automotive aftermarket parts retailer. It lost nearly 6% on the day on above-average volume. I couldn’t find any news to account for the correction.

AAP stock, while up 33% in 2026 despite yesterday’s decline, has lost 75% of its value over the past five years. In the past three years, it’s traded between a high of $88.56 and a low of $28.89. It is currently trading below the midpoint of the 3-year range.

Which is why the stock’s one unusually active option yesterday stands out. Someone made a large bet on its Aug. 21 $62.50 call. I consider the reasons why.

The AAP Call Option in Question

AAP had the fourth-highest Vol/OI (volume-to-open-interest) ratio yesterday at 62.53. As I said earlier, I couldn’t find any news to account for the nearly 6% drop.

I do know that the stock’s overall options volume was 29,442, 3.4 times the 30-day average. The Aug. 21 $62,50 call accounted for 31% of the day's total, which was the third-highest daily amount over the past three months.

A quick look at the large trades for the Aug. 21 $62.50 shows us that there was a single trade for 8,800 call contracts (96% of the call’s volume) at 12:43 p.m. ET.

At first, I thought it could be a Covered Call bet. However, the multi-leg floor trade was a new position. There is another option leg to the trade, which negates the strategy.

Here are both legs. You’ll notice that they were both for 8,800 at 12:43 p.m. ET and both to open, making them new positions, not adjustments to existing trades.

The 2 Calls Scream ‘Bull Call Spread’

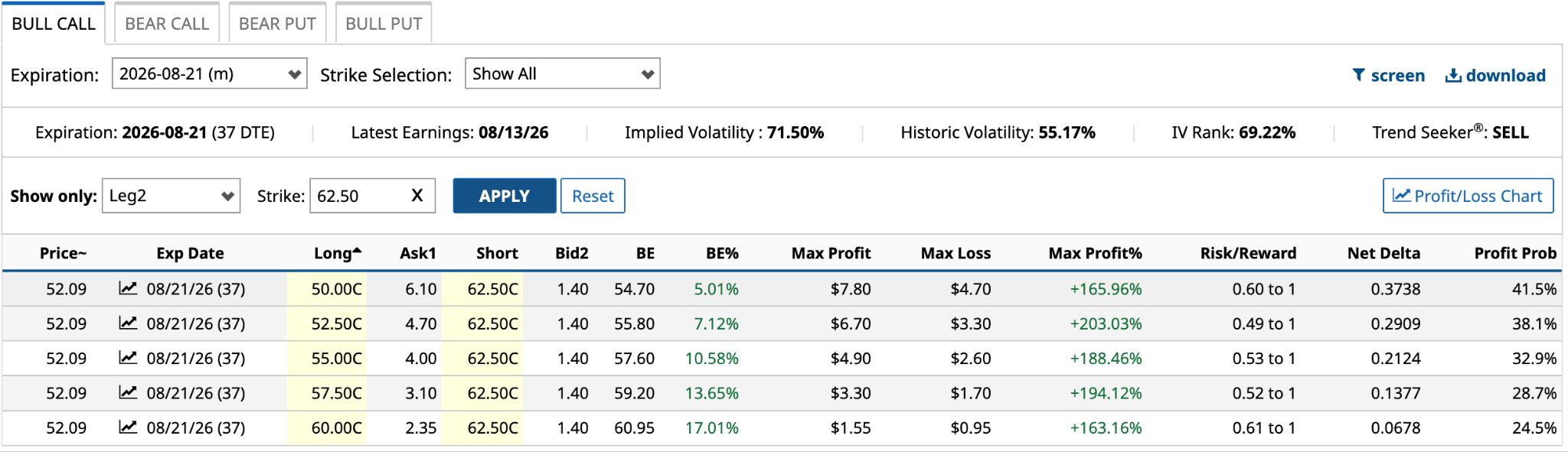

The Bull Call Spread involves buying a call and selling another call at a higher strike price. It is a bullish bet on AAP’s share price over the next 37 days. Based on yesterday’s unusual options activity, I’ve highlighted long calls between $50 (the second 8,800 trade shown earlier) and $60, combined with short $62.50 calls across the board.

The net debits or maximum losses for the five possible short calls range from $0.95 to $4.70. That translates to between 1.8% and 9.0% of AAP’s share price. Anything below 10% isn’t a bad deal.

While you might be tempted to go for the lowest cost outlay, the $60 long call / $62.50 short call combination, the risk/reward proposition and maximum profit percentage are virtually identical to the $50 long call / $62.50 short call combination. Yet, the profit probability -- the likelihood of breaking even on the trade -- is much higher for the latter combination. Perhaps that’s what the trader/investor from yesterday’s two 8,800-call trades was thinking.

In the $50/$62.50 bull call spread scenario above, the breakeven is $54.70 [$50 strike + $4.70 net debit], 5.01% above yesterday’s $52.09 closing share price. If we use the data from yesterday’s two 8,800-call trades, the breakeven increases to $54.78 [$50 strike price + $4.78 net debit], but the percentage to breakeven drops to less than 1%.

With an expected move of nearly 15% by the Aug. 21 expiration, a good trade becomes a great trade.

What About the Covered Call?

As I said in the introduction, I originally thought the unusually active, 8,800-call trade might have been a covered call. But, as mentioned, the MLFT code ruled out that possibility.

However, let's consider the covered call options strategy nonetheless.

So, in this instance, you buy 100 shares of AAP at $52.09 a share, a $5,209 outlay. You simultaneously sell one Aug. 21 $62.50 call for $1.40 ($140) in premium income, reducing the outlay to $50.69 ($5,069).

The 2.8% [$1.40 premium / $52.09 share price - $1.40 premium] return shown above assumes the share price remains flat over the next 37 days. That translates into a 27.2% annualized return. Not too shabby.

However, if you believe in owning AAP for the long haul, you ultimately want the share price to move higher. So, let’s assume that it moves up to $62.50 by expiration and the 100 shares are called away. That’s a 23.3% return [($62.50 + $1.40 premium - $52.09 share price) / $52.09 share price - $1.40 premium].

Can you see the problem? Not only is your percentage return higher (27.2% vs. 23.3%) if the share price doesn’t move -- yes, the dollar gain is considerably higher -- but you lose out on further appreciation of the stock. AAP traded at an all-time high of $244.55 on Jan. 1, 2022, less than five years ago. While unlikely to go anywhere near that in the next 12-24 months, it’s not impossible.

Ideally, covered calls are meant to boost the long-term returns of your portfolio. They’re not meant to be the entire amount.

Should You Buy AAP for the Long Haul?

The analysts would say no. Of the 27 covering AAP, just two rate it a Buy (3.04 out of 5), with most sitting on the fence. The good news: the average analyst target price is $60.86, 15% higher than its share price at the start of Thursday morning trading.

However, the company’s Q1 2026 results were much better than expected. Top-line revenue was $2.61 billion, $50 million higher than Wall Street expected, with adjusted earnings per share of 77 cents, double the consensus. Furthermore, its same-store sales growth was 3.5% in the first quarter, the highest growth in the past five years.

Despite delivering reasonably good earnings -- it remains in a turnaround -- its shares have fallen since it reported results on May 21.

The two biggest concerns regarding AAP are a lack of growth and its debt levels.

The last time Advance showed positive five-year compound annual revenue growth was in Q3 2023, at just 0.3%. In the past 60 quarters, the five-year revenue CAGR has been positive 75% of the time. Of the 15 that were negative, 10 have come in the past three years.

So investors have legitimate concerns about growth.

The company’s current net debt is $2.69 billion. That’s 2.3 times its trailing 12-month EBITDA (earnings before interest, taxes, depreciation and amortization) as of April 25. The multiple’s not the highest in its history, but it’s high enough. As a result, it spent $177 million in the past 12 months on interest expenses, 57% of its operating income.

I don’t think it’s ready for bankruptcy -- its Altman Z-Score is 1.83, which suggests it’s not distressed, but it’s less than half of O’Reilly Automotive (ORLY), its much bigger peer -- but its debt remains a big drag on the profitability of its business.

If you’re an aggressive investor, buying AAP at current prices and doing bull call spreads seems like an acceptable risk.

However, if you want to own quality, buy ORLY instead.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AAP’s Unusually Active $62.50 Call Isn’t a Covered Call. It’s a Bullish Bet on a Beaten-Down Stock. IBM Just Had the Worst Day in Its History. Here's How to Get Paid to Buy the Dip. Why Strategy’s (MSTR) Q2 Earnings Test May Help Engineer a Short-Term Pop Micron Technology Bear Call Spread Could Net 16% in Five Weeks