Lululemon Athletica (LULU) is one of the S&P 500's ($SPX) worst-performing stocks this year, with shares down about 43%. While the selloff has made the valuation look more attractive, the company is still struggling to revive growth in North America.

Intensifying competition, margin pressure, and underwhelming product launches continue to weigh on the business, suggesting the recent decline alone may not make LULU stock a buying opportunity.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Lululemon’s Struggles Continue

Lululemon reported first-quarter results that exceeded Wall Street's expectations, but a closer look suggests the business is facing mounting headwinds. While total revenue increased 4% year-over-year (YoY), comparable sales declined 2%, indicating that underlying consumer demand remains under pressure despite the headline beat.

Lululemon's core North American market continues to be its weakest link. Revenue in the region declined 3%, while comparable sales fell 6%, reflecting softer consumer spending and reduced store traffic. International markets once again provided the primary source of growth. Revenue in Mainland China climbed 30%, supported by a 13% increase in comparable sales, although management noted that the timing of the Chinese New Year contributed approximately eight percentage points to that growth. Meanwhile, revenue from the Rest of World segment rose 13%, highlighting continued strength outside North America.

www.barchart.com

www.barchart.com Although first-quarter performance came in ahead of expectations, management struck a cautious tone regarding the current quarter. Sales trends weakened as the second quarter began, with management citing softer customer demand, negative sentiment across traditional and social media that affected store traffic, and product launches that failed to resonate as strongly as anticipated.

In light of these challenges, the company revised its financial outlook. Lululemon now expects second-quarter revenue to range between $2.45 billion and $2.48 billion, representing a YoY decline of roughly 2% to 3%. For fiscal 2026, management lowered its full-year revenue guidance to $11.0 billion–$11.15 billion, compared with its previous forecast of $11.35 billion–$11.5 billion.

Profitability is also under increasing pressure. Gross margin contracted by 410 basis points during the first quarter, primarily due to higher tariff costs and increased promotional activity. Similar pressure is likely to persist in the second quarter and throughout the year, as tariffs, investments in new store openings, distribution network optimization, and elevated markdowns continue to weigh on margins.

The combination of weaker sales and lower margins is expected to negatively impact earnings. Lululemon projects second-quarter earnings per share (EPS) of $1.76 to $1.81, a sharp decline from $3.10 reported in the same period last year.

The full-year earnings outlook has also been revised downward. The company now expects fiscal 2026 diluted earnings per share of $10.95 to $11.15, compared with $13.26 in fiscal 2025. This is also well below its prior guidance range of $12.10 to $12.30, reflecting growing concerns that slowing demand and rising cost pressures will weigh on profitability throughout the year.

Lululemon's Risk-Reward Still Doesn't Look Favorable

Following its sharp selloff, Lululemon trades at a forward price-to-earnings ratio of 10.6, which is well below its historical valuation. While that may look attractive for a company with a strong brand and a long track record of growth, the discount appears justified.

Lululemon has lowered its expectations for the year as tariffs, increased promotional activity, and intensifying competition weigh on profitability. Analysts now expect the company to report a double-digit decline in earnings this fiscal year.

The lower valuation reflects these headwinds. Although Lululemon remains a premium brand, slowing growth, margin pressure, and declining earnings make the current risk-reward profile less compelling.

The Bottom Line: A Lower Valuation Doesn't Fix Lululemon's Problems

Lululemon's sharp decline has undoubtedly made LULU stock cheaper, but cheaper does not necessarily mean undervalued. With North American demand weakening, margins under pressure, and earnings expected to decline, Lululemon still faces significant execution risks. Until Lululemon shows that it can stabilize growth and restore profitability, investors may be better off waiting for clearer signs of a turnaround rather than buying solely because the stock has fallen.

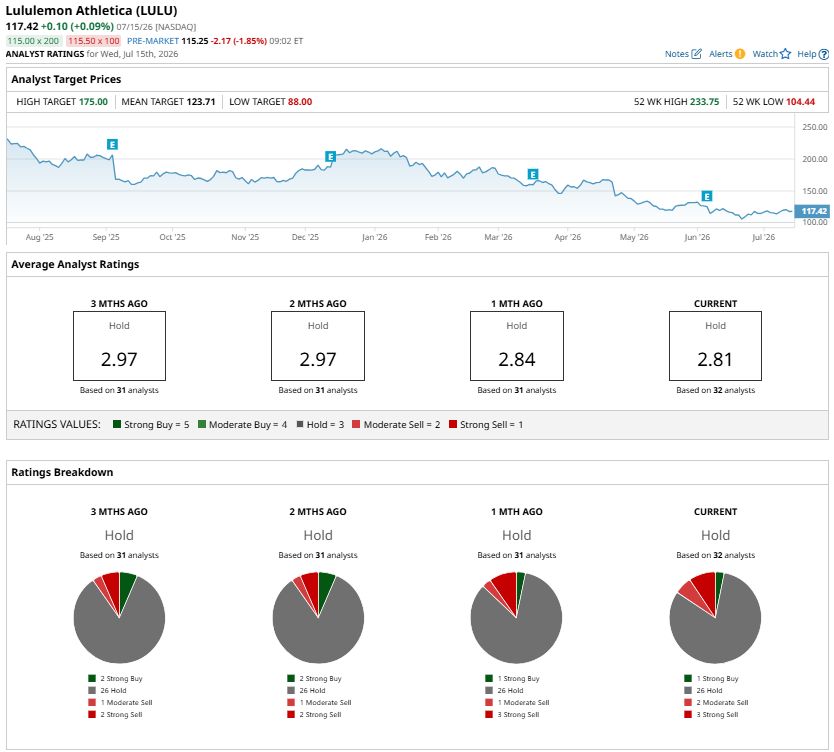

Analysts maintain a “Hold” consensus rating on LULU stock.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Skyworks Stock Just Got Downgraded Why Verizon Stock Can Still Be a Good Choice for Income Investors MU Stock Alert: What to Know as Micron Teams Up With Qualcomm NVDA Stock Alert: What to Know as Nvidia Launches New AI Model