International Business Machines Corporation (IBM) registered its worst day on July 14, as the stock dropped 25.2% intraday after the company reported disappointing preliminary second-quarter results. This was the result of customers redirecting spending towards chips and servers, as AI-driven shortages are affecting IT budgets.

CNBC’s Jim Cramer is not keen on the idea of capitalizing on IBM’s dip. According to Cramer, the company is on the wrong side of the shift in enterprise tech spending, as budgets are prioritizing AI, and the company’s Q2 revenue miss lends credence to that concern. Corporate IT spending is now centered on three key areas, which Cramer identified as cybersecurity, hardware, and AI “tokens.”

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About IBM Stock

IBM is a worldwide technology and consulting company that develops and delivers enterprise IT solutions, including hybrid cloud, AI software and services, mainframe systems, servers, and industry-focused digital transformation support. The company has a market capitalization of $198.50 billion.

Based in Armonk, New York, it brings together hardware engineering, software platforms such as Watson and Red Hat-based offerings, and professional services to help organizations modernize older systems and scale AI adoption. Recent updates include new enterprise AI agent capabilities, refreshed compact mainframe and server products, and deeper partnerships in open-source supply chain security.

As investors grew worried about AI disruption to parts of its software and mainframe-related business, and recent trends show investment moving away from IBM’s higher-margin offerings, the stock has taken a hit.

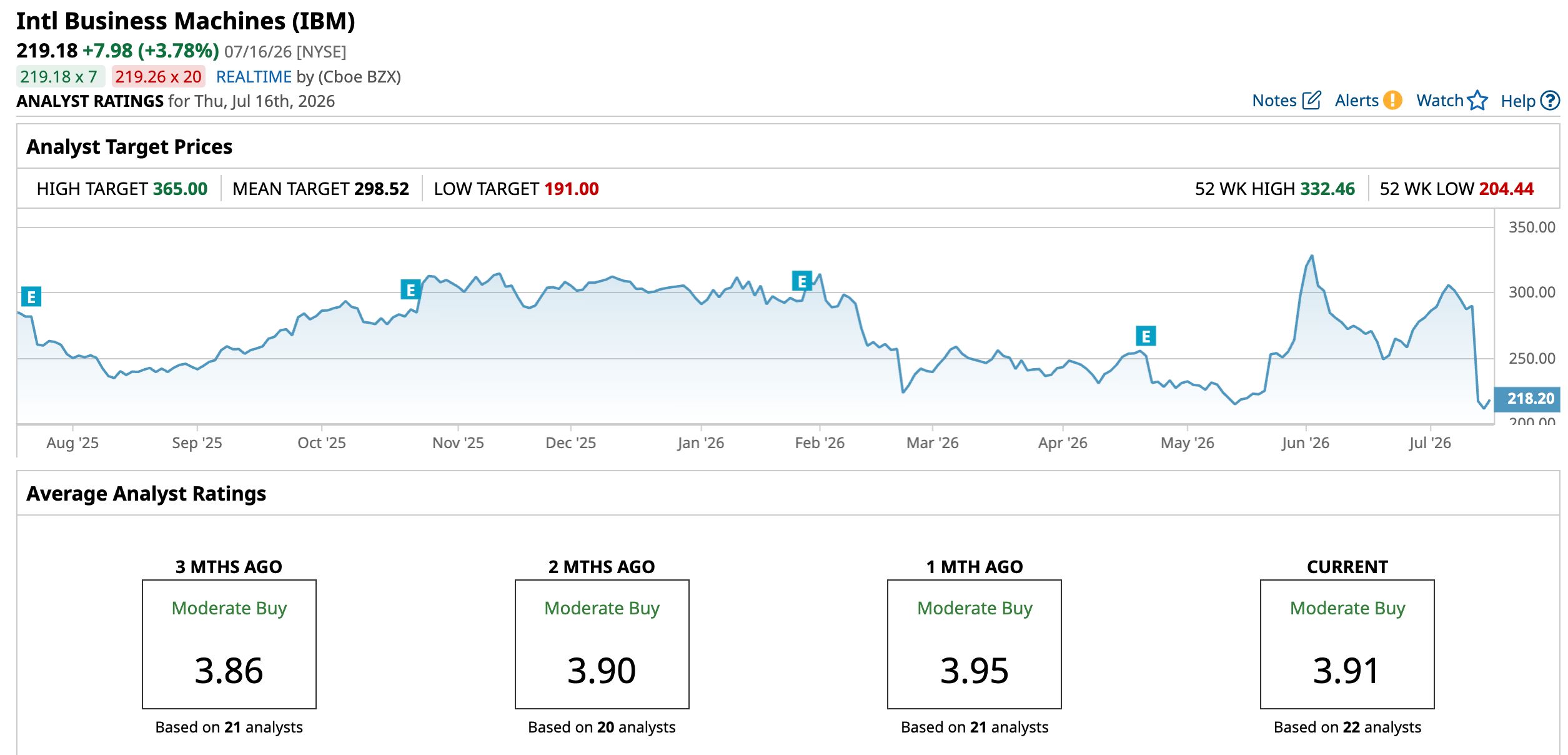

Over the past 52 weeks, IBM’s stock declined 22.78%, while it is down 26.5% year-to-date (YTD). Its shares reached a 52-week low of $211.03 on July 15 and are up only 3.4% from that level.

www.barchart.com

www.barchart.com The stock is currently trading significantly below its 100-day moving average, while its MACD line appears to be approaching the signal line.

On a forward-adjusted basis, IBM’s price-to-earnings (non-GAAP) ratio of 17.37 times is lower than the industry average of 24.45 times.

IBM Q2 Preliminary Results Show Revenue Miss and Profit Warning

IBM’s Q2 preliminary results were disappointing amid investors worrying about the impact of AI. The company’s revenue for Q2 was $17.20 billion, up by a modest 1% year-over-year (YOY). However, this missed Wall Street analysts' $17.86 billion estimate. Investors noticed that the flat consulting revenue and infrastructure revenue are down 7% YOY. IBM’s GAAP-based EPS dropped 2% YOY to $2.27, while non-GAAP EPS increased 5% to $2.93, missing the $3.01 that Street analysts had expected.

IBM admitted that companies' capex reprioritization was contrary to its management's expectations. The firm observed clients shift their quarterly capex spend toward servers, storage, and memory purchases to secure supply-constrained infrastructure ahead of expected price increases. This dynamic impacted IBM’s client buying patterns. The company also stated that its clients were distracted by industry-wide cybersecurity concerns during the quarter.

Analysts believe IBM can further improve its bottom line. For the current year, IBM’s EPS is expected to grow 6.4% YOY to $12.33, followed by an 8.4% increase to $13.37 for the next year. For the third quarter, analysts expect the company’s EPS to grow 7.9% YOY to $2.86.

What Do Analysts Think About IBM’s Stock?

Wall Street analysts have some differing opinions on IBM’s stock. After the company released its preliminary Q2 results, analysts at Oppenheimer downgraded IBM to “Perform” and removed the $350 price target. Analyst Param Singh highlighted that IBM’s results have missed both Oppenheimer’s and consensus estimates across every segment.

Morgan Stanley analysts maintained an “Equal-Weight” rating on IBM’s stock but increased the price target from $267 to $293. Prior to the Q2 results, analysts at HSBC downgraded the stock from “Hold” to “Reduce,” and set a price target of $191. HSBC’s downgrade underscores sector-wide worries that cautious enterprise spending and slow AI-to-consulting monetization are weighing on investor sentiment.

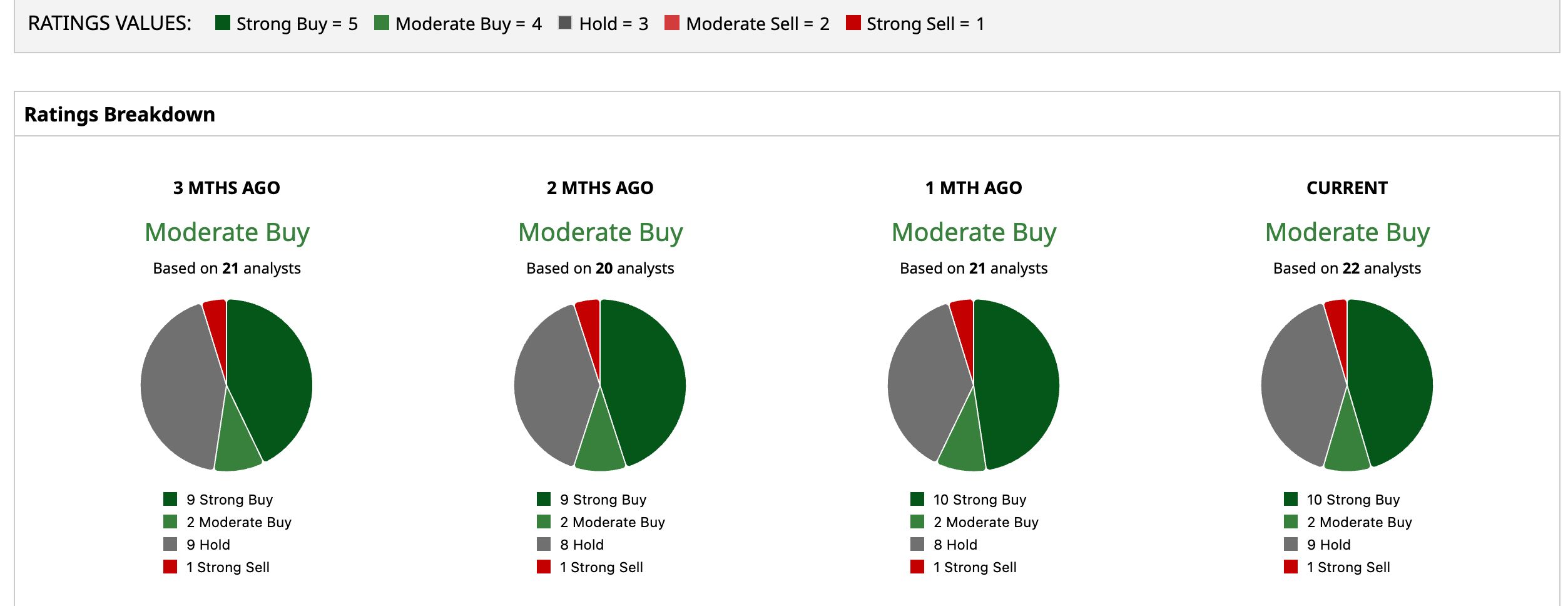

Wall Street analysts are still taking a positive stance on IBM’s stock now, with a consensus “Moderate Buy” rating overall. Of the 22 analysts rating the stock, 10 analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while nine analysts are playing it safe with a “Hold” rating, and one analyst gave a “Strong Sell” rating. The consensus price target of $298.52 represents a 36.2% upside from current levels. Moreover, the Street-high price target of $365 indicates a 66.5% upside from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Quantinuum Just Struck a New Deal with Rolls-Royce. What That Means for QNT Stock Here. Why Jim Cramer Is Telling Retail Investors to Stay Far Away from the IBM Stock Dip Reddit Just Scored a New 'Outperform' Rating. What Comes Next for RDDT Stock. SpaceX Is Back at Its IPO Price. Here Is When I Would Buy It.