NiSource Inc. NI benefits from data center-driven demand growth and strategic cost management that reduces expenses and boosts margin. Its systematic capital investment supports renewable energy expansion, infrastructure modernization and long-term growth.

This Zacks Rank #3 (Hold) company faces risks from the aging assets and regulatory risks, which may adversely impact profit.

NI’s Tailwinds

NiSource benefits from rising clean electricity demand, driven by rapid data center expansion, which is increasing power consumption and supporting revenue growth. The company’s unit, NIPSCO Generation LLC (GenCo), has secured 4 gigawatts (GW) of data center contracts and anticipates demand rising to as much as 9 GW. GenCo is engaged in strategic negotiations for an additional 3 GW and expects another 2 GW of data center opportunities, strengthening its growth prospects.

The company is gaining from ongoing cost-reduction efforts, supported by the launch of Project Apollo. The project is expected to deliver $40-$60 million in annual savings, maintain flat operating expenses over the five-year plan and limit average annual customer bill increases below 5%. The strategic cost management initiative enhances operational efficiency, reduces expenses and supports earnings growth and financial flexibility.

It expects consolidated capital investments totaling $28.6 billion for 2026-2030, including $21 billion in base plan capital investments and $7.6 billion in data center-related capital investments, supporting a 9-11% consolidated rate base CAGR through 2026-2033.

NI’s Headwinds

Despite ongoing maintenance programs and substantial infrastructure investments, NiSource remains exposed to risks associated with aging assets. Any unexpected equipment failures or operational disruptions could affect service reliability, pressure margins and adversely impact overall performance.

The company operates in a highly regulated environment and must comply with numerous federal, state and environmental requirements. Failure to comply with existing or modified laws could increase costs, affect operations and influence future earnings growth.

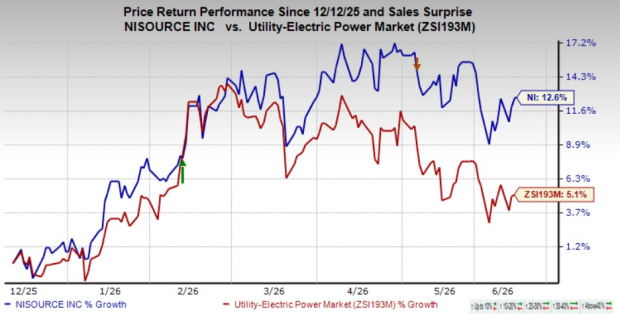

Price Performance of NI

In the past six months, NiSource shares have rallied 12.6% compared with the industry’s 5.1% growth.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks in the same industry are Duke Energy DUK, Consolidated Edison ED and PG&E Corporation PCG. All the stocks carry a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DUK, ED and PCG have dividend yields of 3.41%, 3.30% and 1.20%, respectively, which are better than the Zacks S&P 500 Composite’s yield of 1.46%.

The Zacks Consensus Estimate for Duke Energy, Consolidated Edison and PG&E 2026 EPS are pegged at $6.71, $6.09 and $1.65, suggesting year-over-year growth of 6.34%, 6.84% and 10%, respectively.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NiSource, Inc (NI): Free Stock Analysis Report

Pacific Gas & Electric Co. (PCG): Free Stock Analysis Report

Duke Energy Corporation (DUK): Free Stock Analysis Report

Consolidated Edison Inc (ED): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).