Shares of Intuit, Inc. INTU are trading at a discount. Based on the forward 12-month Price-to-Sales (P/S) ratio, INTU trades at 3.27x, well below the Zacks Computer - Software industry average of 6.33x.

The stock also carries a lower valuation than several industry peers. For comparison, Oracle Corp. ORCL trades at a forward P/S multiple of 6.13x, while Automatic Data Processing, Inc. ADP trades at 3.87x, highlighting Intuit's relatively discounted valuation.

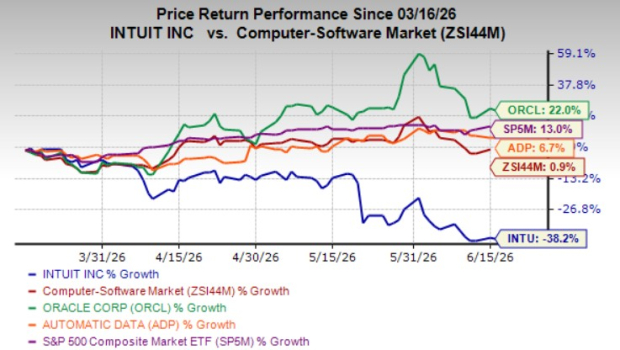

Image Source: Zacks Investment Research

This comes amid a 38.2% decline of Intuit’s shares over the past three months, compared with the industry’s 0.9% growth and the S&P 500 composite 13% rise. Its peers, Oracle and ADP, have increased 22% and 6.7%, respectively, during this period.

Nevertheless, the decline has raised questions about whether this is another temporary stumble or a sign of deeper trouble in the computer-software landscape.

Image Source: Zacks Investment Research

Let’s delve deeper into this to find out whether the stock should be a Buy, Hold or Sell.

Why Do INTU Shares Fall?

Intuit acknowledged weaker-than-expected performance in its DIY segment in the third quarter of fiscal 2026. Management citied pressure among the most price-sensitive DIY tax filers earning less than $50,000 annually and noted that the company 'lost on price' in this segment. To reaccelerate growth in this segment, Intuit plans to refine its offerings and pricing structure to better serve simple filers’ needs at the lower end of the market while leveraging its broader Consumer platform to generate revenue opportunities beyond tax preparation.

Intuit continues to invest in product development, artificial intelligence and go-to-market initiatives, which is likely to put some pressure on near term profitability. In the third quarter of fiscal 2026, total costs and expenses rose to $4.54 billion from $4.03 billion in the prior-year period. The company also announced a 17% workforce reduction and expects to incur about $300-$340 million in restructuring charges, largely to be recognized in the fourth quarter of fiscal 2026.

What’s in Favor of INTU Stock?

Intuit has evolved from a tax- and accounting-software vendor into a unified platform that integrates TurboTax, Credit Karma, QuickBooks, Mailchimp and Intuit Enterprise Suite, serving consumers, small businesses and mid-market companies. This shift is now being reflected in the company’s fundamentals. In the third quarter of fiscal 2026, the company reported revenue growth of 10.4% year over year. As a result, it has raised its full-year revenue-growth guidance to approximately 13% to 14%.

Intuit's Global Business Solutions segment serves small and mid-market businesses and accounting professionals. The segment combines AI-driven automation, data-driven insights and expert assistance to help customers manage end-to-end financial workflows. In the third quarter of fiscal 2026, Global Business Solutions revenues grew 15.3% to $3.29 billion year over year or 17% excluding Mailchimp. For fiscal 2026, Intuit expects the segment revenues to grow 14-15%.

Mailchimp, Intuit’s email marketing platform, is integrated with QuickBooks to help businesses use customer and financial data for more effective marketing. In May 2026, Intuit Mailchimp launched Analytics AI, a native conversational analytics agent built into Mailchimp. The tool lets marketers ask plain-language questions about campaign performance, audience behavior and revenue data and receive instant answers with strategic recommendations, eliminating the need to manually build dashboards or export reports.

Intuit’s consumer segment continued to underpin its strong quarterly results. In the third quarter of fiscal 2026, consumer revenues increased 7.5%, driven by Credit Karma revenue growth of 14.9% and TurboTax growth of 7%. Management noted that average revenue per user (ARPU) is about 30% higher for customers using both TurboTax and Credit Karma compared to customers using TurboTax alone. The company is seeing more than 35% of TurboTax customers adopt its fast money offerings.

Intuit continued to expand its assisted tax offerings through TurboTax Live, which is expected to account for approximately 53% of total TurboTax revenues in fiscal 2026. Management highlighted that TurboTax Live customers are projected to grow 38% this year, while revenues are projected to rise 36%, reflecting increasing consumer demand. For fiscal 2026, management expects Consumer Group revenue growth of 10%, including TurboTax at 7%, Credit Karma at 19% and ProTax at 4%.

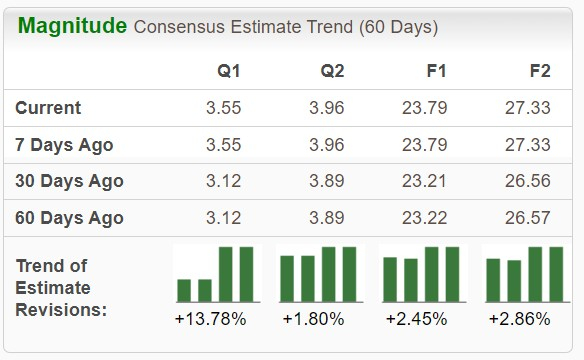

INTU’s Estimate Revision

Reflecting similar sentiments, the Zacks Consensus Estimate for fiscal 2026 earnings per share (EPS) has moved up 58 cents to $23.79 over the past 30 days. The 2026 EPS estimate suggests 18.06% growth from the prior-year quarter.

Image Source: Zacks Investment Research

How to Play the INTU Stock?

Intuit has built a diversified financial software ecosystem that serves consumers, small businesses and accounting professionals, creating a strong foundation for long-term growth. Its solid financial performances, positive earnings estimate, and discounted valuations position it well for sustained growth.

Although the stock's 38.6% decline for three-months improves entry points, the risk-reward profile does not yet appear compelling enough to warrant an aggressive buying stance. As such, existing shareholders may consider holding their positions and benefiting from Intuit's long-term growth potential. New investors, however, may be better served waiting for a more attractive entry point or greater visibility into future growth.

Currently, Intuit carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Automatic Data Processing, Inc. (ADP): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Intuit Inc. (INTU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).