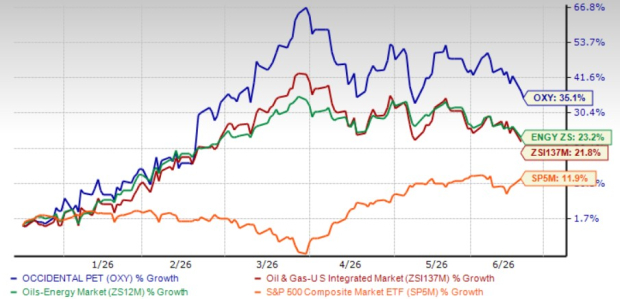

Occidental Petroleum Corporation’s OXY shares have gained 35.1% in the past six months compared with the Zacks Oil and Gas-Integrated-United States industry’s rise of 21.8%. The company has also outperformed the Zacks Oil-Energy sector’s return of 23.2% and the S&P 500 composite’s 11.9% in the same time period.

Occidental’s strategic investments and steady production growth continue to strengthen its cash flow generation capabilities. The acquisition of CrownRock L.P. has further enhanced the company’s footprint in the Permian Basin, supporting long-term operational growth. Additionally, the discovery of high-quality oil at the Bandit prospect in the Gulf of America is expected to contribute meaningfully to Occidental’s production volumes over time.

However, the ongoing geopolitical tensions in the Middle East and related logistical disruptions are likely to weigh on the company’s sulfur sales volumes from the region during the second quarter.

Price Performance (Six Months)

Image Source: Zacks Investment Research

Another operator in the same industry, ConocoPhillips COP, has low-risk and cost-effective operations spread across North America, Asia, Australia and Europe. ConocoPhillips’ shares have gained 20.8% in the past six months.

Is OXY stock worth adding to your portfolio solely because of its recent price gains? Before making an investment decision, it is important to look beyond the stock’s momentum and evaluate the key factors that could determine whether now is an attractive entry point for Occidental. Let’s take a closer look at those factors.

Factors Enhancing Occidental’s Growth Potential

Occidental is benefiting from its continued focus on the Permian Basin, a strategy that has been further strengthened through targeted acquisitions. The purchase of CrownRock L.P. is expected to expand the company’s presence in the region and improve the scale of its operations. Moreover, Occidental has close to a decade of high-return drilling opportunities in the Permian under current economic and technical conditions. The addition of CrownRock’s assets is also expected to provide a meaningful boost to the company’s production growth.

The Permian Basin remains the cornerstone of Occidental’s production portfolio. For the second quarter of 2026, the company expects Permian output of 783-803 thousand barrels of oil equivalent per day (Mboe/d), compared with total companywide production guidance of 1,390-1,430 Mboe/d. To support growth, Occidental plans to bring 460-510 wells online in the Permian Basin and 150-170 wells in the Rockies during 2026, positioning it for higher production volumes in the coming years.

Occidental recently reported a new oil discovery at the Bandit prospect in the Gulf of America. Exploration drilling at Green Canyon Block 680 identified thick, high-quality Miocene formations containing oil-saturated sands across the entire interval, underscoring the prospect’s significant development potential. The discovery is expected to enhance Occidental’s long-term production profile and further strengthen its offshore asset base. For 2026, the company anticipates Gulf of America production of 130-136 Mboe/d.

Occidental has been streamlining its portfolio through the sale of non-core assets and using the proceeds to strengthen the balance sheet. Over the past 20 months, the company has repaid nearly $13.9 billion of debt, a move that has lowered its annual interest expense about $740 million and improved financial flexibility.

Headwinds for Occidental Stock

Occidental’s operating results are influenced by shifts in demand and the volatility of both global and local commodity prices. As of Dec. 31, 2025, the company had no active commodity hedges in place, leaving it fully exposed to market fluctuations. A significant decline in commodity prices from current levels could adversely affect OXY’s financial performance.

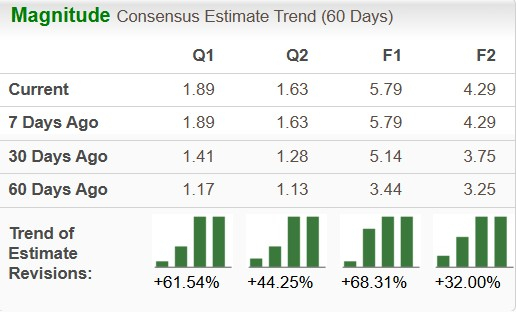

Occidental’s Earnings Estimates Are Moving Up

The Zacks Consensus Estimate for Occidental’s 2026 and 2027 earnings per share indicates an increase of 68.31% and 32%, respectively, in the past 60 days.

Image Source: Zacks Investment Research

Another company, Chevron Corporation CVX, is a leading publicly traded oil and gas company, supported by a diversified portfolio of operations across the globe. The Zacks Consensus Estimate for Chevron’s 2026 and 2027 earnings per share indicates an increase of 51.67% and 21.52%, respectively, in the past 60 days.

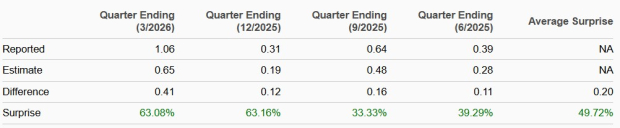

OXY Stock’s Earnings Surprise History

The stable performance of the company allowed its earnings to surpass estimates in each of the past four quarters, the average surprise being 49.72%.

Image Source: Zacks Investment Research

Chevron’s earnings also surpassed expectations in the last four quarters, resulting in an average surprise of 18.6%.

Occidental’s Long-Term Debt to Capital

Debt plays a vital role in the oil and gas industry, where companies require heavy capital investments for exploration, drilling, production and infrastructure expansion. Borrowed capital allows firms to pursue major projects, grow reserves and fund acquisitions while preserving liquidity. Prudent debt management also enables companies to navigate commodity price swings and maintain long-term growth momentum.

Currently, courtesy of efficient debt management, Occidental’s long-term debt to capital is pegged at 27.82%, lower than its industry average of 29.2%.

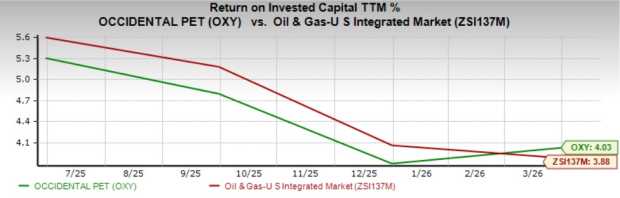

Occidental’s Return on Invested Capital

Return on Invested Capital (“ROIC”) measures how efficiently a company uses its debt and equity capital to generate profits. It reflects management’s ability to create value from invested funds. Generally, a higher ROIC indicates more effective capital allocation and stronger value creation, while a lower ROIC may signal less efficient use of capital.

Occidental’s ROIC is higher than the industry average in the trailing 12 months. ROIC of OXY was 4.03% compared with the industry average of 3.88%.

Image Source: Zacks Investment Research

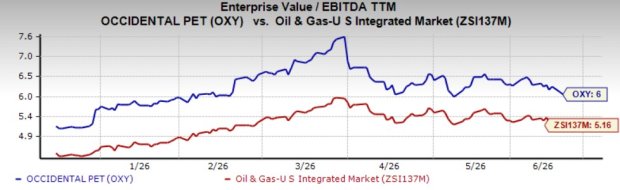

OXY’s Shares Are Trading at a Premium

Occidental’s shares are currently expensive on a relative basis, with the current trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA TTM) being 6.0X compared with its industry average of 5.16X.

Image Source: Zacks Investment Research

Wrapping Up

Occidental’s emphasis on reducing debt, supported by the strength of its domestic operations and the synergies from recent acquisitions, is likely to bolster overall performance.

The company continues to face challenges from the highly competitive industry and is presently trading at a premium.

Despite certain challenges, this Zacks Rank #2 (Buy) stock remains appealing due to its robust U.S. operations and significant presence in the resource-rich Permian Basin. With rising earnings estimates and better ROIC, the stock shows strong performance potential, making it a compelling addition to investors’ portfolios.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX): Free Stock Analysis Report

ConocoPhillips (COP): Free Stock Analysis Report

Occidental Petroleum Corporation (OXY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).