Everpure, Inc. P is currently trading at a 12-month forward price-to-earnings (P/E) multiple of 26.83X, higher than the industry average of 21.98X. While Everpure’s P/E-to-growth of 1.39 exceeds the industry average of 1.13, signaling overvaluation, a deep dive into its financial metrics might reveal otherwise.

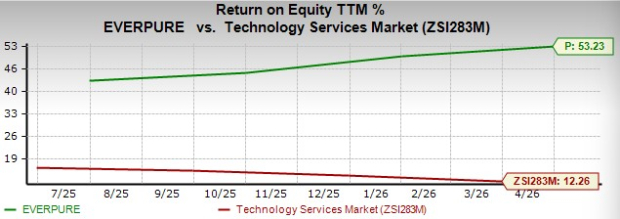

The company’s return on equity (ROE) is a standout metric. Currently, Everpure’s ROE is 53.2%, significantly higher than the industry average of 12.3%, highlighting management’s efficiency in generating substantial profits from shareholders’ equity. A high ROE might prompt investors to pay a premium for Everpure, as the business demonstrates a competitive moat in capital efficiency.

It is important to acknowledge that the company has no long-term debt on its balance sheet, implying that its high ROE can be attributed to a net income margin of 15.5% reported in the first quarter of fiscal 2027 that expanded 300 basis points from the year-ago quarter.

On the operations front, Everpure displayed strength in managing a supply-chain crisis, led by rising AI infrastructure demand. While this hindrance forced price hikes, leading to customer pull-ins, management assured customers that the company would share the cost pain rather than indulging in profit.

Despite these headwinds, new customer logos increased 20% year over year, and penetration stood at 64% of the Fortune 500. Total subscription revenues and contract value sales for storage-as-a-service gained 17% and 73% year over year, respectively, in the first quarter of fiscal 2027, resulting in an outstanding 35% rise in the top line.

Comparison With Competitors

Everpure’s top competitors, Xylem XYL and A. O. Smith Corporation AOS, are currently priced at a forward 12-month P/E of 19.16 and 14.7, respectively. While Everpure appears substantially overvalued compared with Xylem and A. O. Smith, Everpure holds an upper edge financially. In terms of ROE, Xylem and A. O. Smith are standing at 11.3% and 28.4%, respectively. Therefore, Everpure’s premium is fully justified as it operates in an entirely superior financial tier.

Everpure’s Price Performance, Value Score & Estimates

The P stock has risen 37.4% over the past year, outpacing the 11.3% rally in its industry.

P has a Value Score of D.

The Zacks Consensus Estimate for Everpure’s fiscal 2027 and 2028 earnings moved up 1.1% over the past 30 days.

Everpure currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

A. O. Smith Corporation (AOS): Free Stock Analysis Report

Everpure, Inc. (P): Free Stock Analysis Report

Xylem Inc. (XYL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).