HA Sustainable Infrastructure Capital, Inc. HASI has rallied sharply, with shares up 18.9% in the past six months and 50.4% over the past year.

The buying case rests on recurring earnings growth and higher yields. The caution case centers on valuation, funding costs and whether the company can keep converting its pipeline into profitable earning assets.

Why HASI Bulls See More Upside

HASI’s first-quarter adjusted earnings of 77 cents per share rose 20% year over year and beat the Zacks Consensus Estimate of 68 cents. Adjusted recurring net investment income increased 29% to $101 million, giving bulls a clearer earnings-quality argument.

The Zacks Consensus Estimate for 2026 and 2027 earnings has moved higher over the past month. Management also expects 2028 adjusted EPS of $3.50-$3.60, supporting the view that portfolio growth and recurring fee income can keep earnings moving higher.

Earnings Estimate Revision

Image Source: Zacks Investment Research

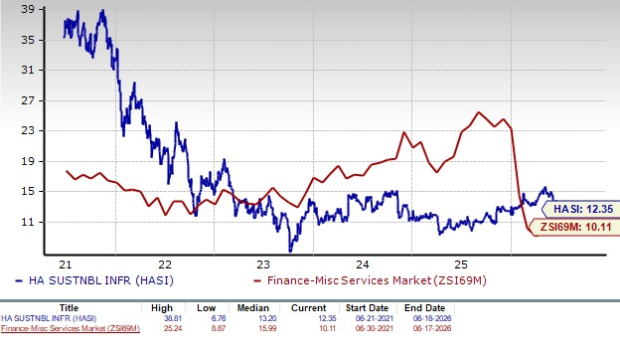

HA Sustainable Valuation in Context

HASI trades at 12.35X forward 12-month earnings. That is above the Zacks sub-industry’s 10.11X but below the Zacks Finance sector’s 16.37X and the S&P 500’s 21.65X.

P/E F12M

Image Source: Zacks Investment Research

That split matters. The earnings multiple does not look demanding relative to the broader market, but price/book and price/cash flow ratios are above industry averages, leaving less room for execution missteps.

Apollo Global Management Inc. APO and Ares Management Corporation ARES are comparison points in the broader financial-services peer set. Investors weighing HASI’s valuation may compare its yield-driven specialty finance model with other capital-allocation businesses, even though its sustainable infrastructure focus is distinct.

What Could Limit HASI Returns

The bear case starts with funding costs. HASI’s weighted-average interest rate increased from 5.8% in 2025 to 6.1% in the first quarter of 2026, reflecting higher-cost hybrid securities and redemption-related expenses.

Higher borrowing costs mean HASI needs to keep originating investments at attractive yields above 10.5% to protect profitability. If yields moderate or deployment slows, margin pressure could make targeted returns harder to achieve.

Debt also limits flexibility. Higher debt obligations could reduce the company’s ability to maneuver if capital markets become less favorable or if policy uncertainty slows project closings.

HA Sustainable Dividend and Balance Sheet

HASI adds an income component with a quarterly dividend of 42.5 cents per share. The indicated dividend yield is about 4.5%, giving investors a payout while they wait for earnings growth to develop.

The balance sheet cuts both ways. HASI had $5.4 billion of debt outstanding as of March 31, 2026, but also maintained $2.3 billion of available liquidity. That frames the stock as an income-plus-execution story rather than a simple value play.

Liquidity supports debt servicing and portfolio growth. Still, the company must keep matching capital deployment with attractive spreads to justify the recent stock move.

How HASI Screens on Zacks

The bottom line is mixed. HASI has earnings momentum, a sizable pipeline and a dividend yield that may appeal to income-focused investors, but valuation and funding costs argue against chasing the stock without a margin of safety.

The stock currently carries a Zacks Rank #3 (Hold). That rank supports a balanced near-term stance rather than an outright bullish call after strong gains. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores reinforce that view. HASI’s Growth Score of B fits the earnings expansion narrative, but its Value Score of D, Momentum Score of F and VGM Score of D show weaker factor support across the broader scorecard. For now, the setup favors investors who are comfortable betting on execution and recurring earnings durability, not those looking for a clean value or momentum screen.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Apollo Global Management Inc. (APO): Free Stock Analysis Report

HA Sustainable Infrastructure Capital, Inc. (HASI): Free Stock Analysis Report

Ares Management Corporation (ARES): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).