While looser lending criteria and increased usage of technology are expanding the borrower base, subdued consumer confidence is a headwind. Nonetheless, industry players like Credit Acceptance Corporation CACC, Enova International, Inc. ENVA and Encore Capital Group, Inc. ECPG are worth considering.

About the Industry

The Zacks Consumer Loans industry comprises companies that provide mortgages, refinancing, home equity lines of credit, credit card loans, automobile loans, education/student loans and personal loans, among others. These help the industry players generate net interest income (NII), which forms the most important part of total revenues. The prospects of the companies in this industry are highly sensitive to the nation’s overall economic condition and consumer sentiments. In addition to offering the above-mentioned products and services, many consumer loan providers are involved in businesses like commercial lending, insurance, loan servicing and asset recovery. These support the companies in generating fee revenues. Furthermore, this helps the firms diversify revenue sources and be less dependent on the vagaries of the economy.

3 Themes Driving the Consumer Loan Industry's Future

Interest Rates & Loan Demand: After lowering interest rates by 175 basis points since 2024, the Federal Reserve has paused its easing cycle and adopted a more hawkish stance. This shift reflects inflation remaining well above the central bank’s 2% target, exacerbated by the recent oil price shock stemming from geopolitical tensions in the Middle East. Additionally, consumer sentiment has remained weak since late 2025, with the Expectations Index staying below 80 for 16 consecutive months through May, a threshold that has historically signaled an elevated risk of recession. Despite these headwinds, demand for consumer loans is expected to remain resilient and gradually improve, supported by solid economic growth and a still-low unemployment rate. Consequently, industry participants are likely to benefit from continued expansion in net interest margins (NIM) and NII in the coming quarters.

Automation to Improve Operating Efficiency: Consumer loan providers are increasingly leveraging artificial intelligence (AI), machine learning (ML), robotic process automation and digital platforms to streamline loan origination, underwriting, servicing and customer onboarding. AI-driven credit assessment models analyze vast amounts of customer data in real time, enabling faster and more accurate lending decisions while reducing manual intervention, while digital onboarding tools lower acquisition costs and enhance customer experience. Meanwhile, AI-powered servicing and collections platforms improve operational efficiency and risk monitoring. These initiatives are expected to reduce processing expenses, support scalable growth and ultimately boost profitability through higher operating leverage and stronger returns.

Asset Quality: While lower interest rates have helped borrowers stay current on loan and interest repayments, persistent macroeconomic and geopolitical headwinds have kept inflation elevated. This has prompted the central bank to signal a potential rate hike later this year, which could somewhat weaken borrowers’ repayment capacity. As a result, consumer loan providers are likely to set aside substantial reserves for potential delinquencies. Moreover, several credit quality metrics are already trending above pre-pandemic levels.

Zacks Industry Rank Reflects an Optimistic Stance

The Zacks Consumer Loans industry is a 12-stock group within the broader Zacks Finance sector. The industry currently carries a Zacks Industry Rank #30, which places it in the top 12% of more than 245 Zacks industries.

The group’s Zacks Industry Rank, which is the average of the Zacks Rank of all the member stocks, indicates outperformance in the near term. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1. Looking at the aggregate earnings estimate revisions, it appears that analysts are confident in this group’s earnings growth potential. Over the past year, the industry’s earnings estimates for 2026 and 2027 have been revised upward by 2.9% and 9.6%, respectively.

Before we present a few stocks that you may want to add to your portfolio, let's take a look at the industry’s recent stock market performance and valuation picture.

Industry vs. Broader Market

The Zacks Consumer Loans industry has impressively outperformed the Zacks S&P 500 composite and its sector over the past two years.

The stocks in this industry have collectively soared 67.6% over this period, while the Zacks S&P 500 composite and the Zacks Finance sector have risen 42.4% and 37.2%, respectively.

Two-Year Price Performance

Industry Valuation

One might get a good sense of the industry’s relative valuation by looking at its price-to-book ratio (P/B), commonly used for valuing consumer loan stocks because of significant variations in their financial performance from one quarter to the next.

The industry currently has a trailing 12-month P/B of 0.74X, below the median level of 0.76X over the past five years. This compares with the highest level of 1.04X and the lowest level of 0.55X over this period. The industry is trading at a considerable discount compared with the market at large, as the trailing 12-month P/B for the S&P 500 is 8.11X and the median level is 8.01X.

Price-to-Book Ratio (TTM)

As finance stocks typically have a lower P/B, comparing consumer loan providers with the S&P 500 may not make sense to many investors. However, comparing the group’s P/B ratio with that of its broader sector ensures that the group is trading at a decent discount. The Zacks Finance sector’s trailing 12-month P/B of 4.53X for the same period is way above the Zacks Consumer Loan industry’s ratio, as the chart below shows.

Price-to-Book Ratio (TTM)

3 Consumer Loan Stocks to Bet on

Credit Acceptance Corporation: Headquartered in Southfield, MI, CACC offers financing programs and related products and services to automobile dealers across the United States, enabling them to sell vehicles to consumers irrespective of their credit history. Further, it is engaged in the business of reinsuring coverage under vehicle service contracts sold to consumers by dealers on vehicles financed by the company.

Revenue growth remains a major positive for Credit Acceptance, with the same witnessing a five-year (2020-2025) compound annual growth rate (CAGR) of 6.8%. Growth is primarily attributable to a steady rise in finance charges, which is also the main revenue component (accounting for almost 93% of total revenues in the first quarter of 2026). While finance charges are likely to witness headwinds from macroeconomic factors in the near term, solid dealer engagement will offer much-needed support. A steady rise in dealer enrolments and active dealers is expected to support the company’s top-line growth.

CACC continues to execute on a product roadmap aimed at reducing friction for dealers and scaling underwriting and servicing capacity without a proportional increase in expenses. The company is witnessing a steady rise in inbound customer service and account solutions calls routed to the AI-enabled agent, with plans to expand its usage going forward. Additionally, dealer-facing digitization is gaining traction. Over time, these are expected to support higher dealer engagement and improve operating efficiency.

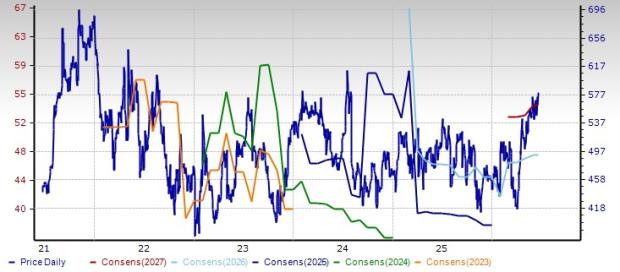

The Zacks Consensus Estimate for earnings for 2026 and 2027 suggests growth of 20.1% and 13.7%, respectively. Shares of this Zacks Rank #2 (Buy) company have jumped 25.8% over the past six months. It has a market cap of $6.1 billion. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: CACC

Enova International: Based in Chicago, IL, Enova is a leading financial technology company focused on providing online financial services. The company caters to small businesses and capitalizes on its proprietary technology, analytics and customer service capabilities to underwrite and fund loans.

Being an early entrant into online lending, the company has completed almost 65 million customer transactions and collected approximately 66 terabytes of consumer behavior data since its launch in 2004. This has enabled Enova to better analyze its specific customer base and expand small and medium businesses (SMB) lending. This Zacks Rank #2 company’s proprietary underwriting systems leverage advanced risk analytics, including ML and AI.

Moreover, the company has been diversifying its operations, which will support its long-term growth. In December 2025, Enova agreed to acquire Grasshopper Bancorp, which will boost its earnings over time. This will also expand the company’s ability to deliver a more comprehensive suite of financial products through a national bank charter, expanding access to credit to those who were traditionally underserved by banks.

The Zacks Consensus Estimate for earnings for 2026 and 2027 indicates an increase of 26.8% and 23.7%, respectively. ENVA’s shares have gained 24.1% over the past six months. It has a market cap of $5 billion.

Price and Consensus: ENVA

Encore Capital: Based in San Diego, CA, ECPG provides debt recovery and related financial services worldwide. Through its global subsidiaries, the company acquires portfolios of charged-off consumer receivables from leading banks, credit unions and utility providers, leveraging data-driven strategies to optimize collections and portfolio performance.

Encore Capital plans to leverage its leadership position in portfolio purchasing and recovery as well as credit management services to bolster its market share worldwide. Over the years, the company’s portfolio purchases and collections have increased, which supported its top-line expansion.

With rising delinquency/charge-off rates in the United States due to higher rates, there is more supply of non-performing loans. This offers Encore Capital an additional opportunity to purchase portfolios and apply its analytics and collections capabilities for higher returns. With scale, funding access and demonstrated execution, the company is expected to continue capturing high-return supply, extending collections growth beyond tax seasonality into subsequent quarters.

The company’s operating engine is delivering consistent overperformance that is now beginning to embed into forward estimates. Encore Capital is witnessing steadily higher collections than the forecasts, as technology, digital and operational innovations lift early-stage collections. Over the next few quarters, management expects the mix to transition from cash overs to higher portfolio revenue as ERC curves adjust upward.

Shares of this Zacks Rank #1 company has soared 52.4% over the past six months. ECPG’s earnings are expected to rise 19.3% in 2026 and 6.5% in 2027. The company has a market cap of $1.8 billion.

Price and Consensus: ECPG

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Credit Acceptance Corporation (CACC): Free Stock Analysis Report

Encore Capital Group Inc (ECPG): Free Stock Analysis Report

Enova International, Inc. (ENVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).