Companies operating in the Zacks Utility - Electric Power industry generate, transmit and distribute electricity to millions of residential, commercial and industrial customers across the United States. These companies manage extensive power generation assets and transmission networks to ensure a reliable energy supply. The regulated nature of utility operations allows them to recover costs through rate hikes and supports steady returns, while growing customer demand contributes to earnings expansion. In addition, utilities are known for offering attractive dividend payouts and stable returns, making them a reliable investment choice.

Electricity consumption across the United States continues to increase, supported by growing electrification trends, population growth, the reshoring of manufacturing activities and the rapid expansion of data centers. Companies operating in this industry are making strategic investments in generation and grid infrastructure supporting long-term revenues and earnings growth.

Given the increasing significance of the power generation, transmission and distribution business, let us compare CenterPoint Energy CNP and Eversource Energy ES. These two regulated electric utilities benefit from rising electric demand and supportive cost-recovery mechanisms, while consistently investing in infrastructure upgrades and grid modernization, making them closely comparable in the utility sector.

CenterPoint Energy is benefiting from rising electricity demand, especially in its Houston Electric service territory, where expanding industrial operations and increasing data center needs are fueling strong load growth. The company's systematic investments in infrastructure development and grid modernization are creating sustainable long-term value for shareholders. By pairing capital spending with constructive regulatory recovery mechanisms, it effectively transforms rate-base expansion into stable earnings growth.

Eversource Energy benefits from its regulated business model, which provides stable cash flow and supports timely cost recovery. ES is allocating capital toward transforming into a pure-play regulated utility, which offers stable growth prospects, aids customers in achieving clean energy goals and delivers more predictable earnings. The company is making strategic investments to expand and modernize its electric transmission and distribution network, enhancing grid reliability and meeting rising electricity demand. These investments are expected to grow its rate base, improve earnings visibility and support long-term value creation for shareholders.

CNP & ES’ Earnings Growth Projections

The Zacks Consensus Estimate for CNP’s earnings per share (EPS) is pegged at $1.91 in 2026 and $2.08 in 2027, suggesting year-over-year growth of 8.52% and 8.85%, respectively. CNP’s long-term (three to five years) earnings growth is currently pinned at 8.85%.

Image Source: Zacks Investment Research

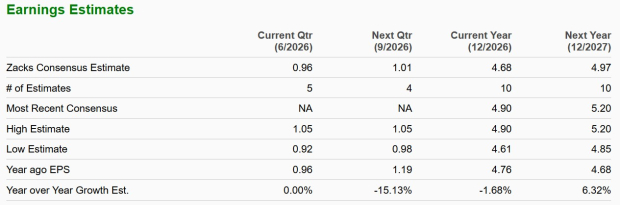

The Zacks Consensus Estimate for ES’ EPS is pegged at $4.68 in 2026 and $4.97 in 2027, suggesting a year-over-year decline of 1.68% and growth of 6.32%, respectively. ES’ long-term earnings growth is currently pinned at 3.25%

Image Source: Zacks Investment Research

Debt to Capital

The Zacks Utilities sector is capital-intensive and requires regular investments to upgrade and maintain infrastructure, enhance operational efficiency and serve rising energy demand. To fund these large-scale, long-term projects, utilities utilize a mix of internally generated cash flows and debt financing from capital markets, thereby supporting steady expansion and ensuring reliable service for customers.

Eversource Energy’s debt-to-capital currently stands at 64.50%, lower than CenterPoint Energy’s 68.31%. CNP and ES’ debt levels are higher than the industry’s 60.97%, with CNP’s being higher, indicating greater reliance on borrowed funds.

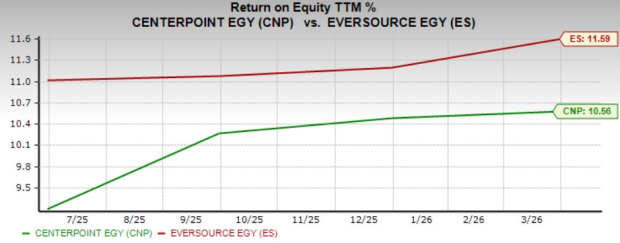

Return on Equity

Return on Equity (“ROE”) is a financial metric that reflects the amount of profit a company earns for each dollar of shareholders’ capital. A higher ROE indicates strong managerial efficiency in using shareholder funds to create value and drive profit growth.

Eversource Energy’s current ROE is 11.59%, outperforming CenterPoint Energy’s lower ROE of 10.56% and the industry average of 11.22%. ES utilizes shareholder capital more effectively and generates higher returns.

Image Source: Zacks Investment Research

Dividend Yield

Utility companies consistently increase shareholders' value through regular dividend distribution, highlighting their commitment to providing steady returns on invested capital. Such distributions reflect the stability of their earnings streams and their ability to generate strong and predictable cash flows.

Currently, the dividend yield for ES is 4.49%, while that for CNP is 2.13%. The dividend yields of both companies are above the S&P 500 average yield of 1.44%.

Capital Investment Plans

The utility sector requires substantial capital spending to maintain assets, improve system resilience and expand infrastructure. Electric utilities are making substantial investments to strengthen their transmission and distribution networks, modernize the grid and deploy advanced technologies, enhancing operational efficiency, system reliability and the quality of customer service.

Eversource Energy plans to invest $5.07 billion in 2026 and about $27.8 billion between 2026 and 2030, including Aquarion investments of $1.3 billion, $11.2 billion in electric distribution and $6.8 billion in natural gas distribution, with an additional $1 billion of potential opportunities. CenterPoint Energy aims to invest $6.8 billion in 2026 and reaffirmed its $65.5 billion 2026-2035 capital plan. These investments are expected to enhance grid resilience, reduce outage durations and deliver meaningful operational cost savings.

Price Performance

ES shares have gained 4% in the past three months compared with CNP’s growth of 3%.

Image Source: Zacks Investment Research

Zacks Rank

Eversource Energy currently carries a Zacks Rank #3 (Hold), while CenterPoint Energy has a Zacks Rank #4 (Sell). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Summing Up

CenterPoint Energy and Eversource Energy both benefit from a regulated structure, rising service demand and significant infrastructure investments to support millions of customers across the United States.

Based on the above discussion, our pick at the moment is Eversource Energy, given its better dividend yield, higher return on equity, lower debt-to-capital ratio, better Zack’s rank and price performance. These factors are expected to provide higher returns to investors when compared with CenterPoint Energy.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CenterPoint Energy, Inc. (CNP): Free Stock Analysis Report

Eversource Energy (ES): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).