Gap Inc.’s GAP turnaround has gained traction across much of its portfolio, but Athleta remains the notable exception. While Gap, Old Navy and Banana Republic continue to post positive comparable sales growth, Athleta is still in the early stages of a multiyear rebuilding effort. Management has been clear that 2026 is a transition year for the brand, with the priority on rebuilding product, brand positioning and merchandising rather than pursuing near-term sales growth. The key question for investors is whether these foundational changes can translate into sustainable momentum over the coming quarters.

The first-quarter results highlighted the work still ahead. Athleta's net sales declined 12% year over year to $270 million, while comparable sales fell 11%, missing the company's expectations. Management attributed the weakness primarily to efforts to clear legacy inventory, a process that has taken longer than anticipated and weighed on top-line performance. Despite the sales pressure, Gap noted that introducing a cleaner assortment remains essential before the brand can return to more consistent growth.

Encouragingly, early signs suggest the strategy may be gaining traction beneath the surface. Gap reported positive customer response to Athleta's new Journey travel collection in select locations, with strong engagement and sell-through rates. New leg silhouettes across core franchises such as the Elation line have also performed well, giving management greater confidence in its future product direction. The company plans to continue clearing older inventory through the second quarter before introducing a broader assortment that better reflects Athleta's long-term positioning in the fall season.

While Athleta is likely to remain a drag on Gap's overall performance in the near term, management expects gradual improvement in the second half as new products gain a larger share of the assortment. Leadership continues to view Athleta as an important long-term growth engine and is investing in product, talent and creative capabilities to strengthen the brand's competitive position. The pace at which these initiatives translate into stronger comparable sales will likely determine whether Athleta can become a meaningful contributor to Gap's next phase of growth.

GAP’s Price Performance, Valuation & Estimates

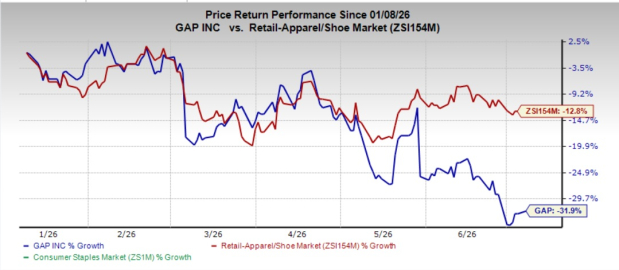

Shares of this Zacks Rank #3 (Hold) company have lost 31.9% in the past six months compared with the industry’s decline of 12.8%.

Image Source: Zacks Investment Research

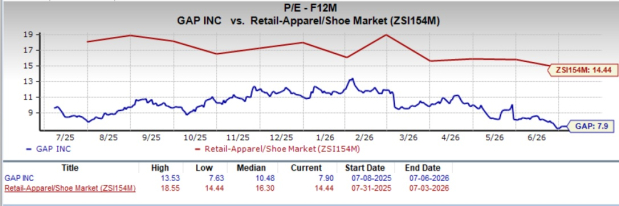

From a valuation standpoint, GAP trades at a forward price-to-earnings ratio of 7.90X compared with the industry’s average of 14.44X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for GAP’s current fiscal-year sales and earnings implies year-over-year growth of 1.2% and 9.9%, respectively. For the next fiscal year, the consensus estimate indicates a 1.9% rise in sales and 10.8% growth in earnings. The company’s EPS estimate for both fiscal years has remained stable in the past seven days.

Image Source: Zacks Investment Research

Key Picks

Ross Stores ROST, a leading U.S. off-price retailer operating Ross Dress for Less and dd's DISCOUNTS stores, sports a Zacks Rank #1 (Strong Buy) at present. ROST delivered a trailing four-quarter earnings surprise of 10.2%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Ross Stores’ current fiscal-year sales and earnings suggests growth of 9.1% and 17.1%, respectively, from the year-ago figures.

Five Below, Inc. FIVE, which operates as a specialty value retailer, currently flaunts a Zacks Rank #1. FIVE delivered a trailing four-quarter earnings surprise of 70.1%, on average.

The Zacks Consensus Estimate for Five Below’s current fiscal-year sales and earnings suggests growth of 14.36% and 34.3%, respectively, from the year-ago figures.

Tapestry, Inc. TPR provides accessories and lifestyle brand products in North America, Greater China, the rest of Asia and internationally. At present, TPR sports a Zacks Rank of 1. TPR has delivered a trailing four-quarter earnings surprise of 15.6%, on average.

The Zacks Consensus Estimate for current fiscal-year sales and earnings implies growth of 13.8% and 36.3%, respectively, from the year-ago reported figures.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Gap, Inc. (GAP): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).