Insulet PODD is well poised for growth in the upcoming quarters, owing to its strong momentum for the Omnipod 5 automated insulin delivery (AID) system for both Type 1 and Type 2 populations. The company is strongly executing against its long-term priorities to drive penetration, deepen competitive advantage, unlock new opportunities and scale profitably. However, macroeconomic pressures and intense competition could pose headwinds for Insulet’s operations.

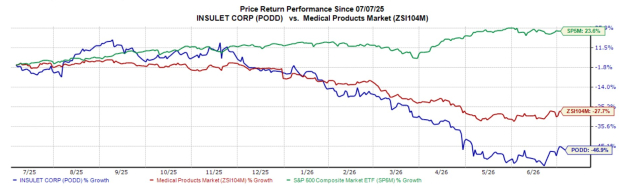

In the past year, this Zacks Rank #3 (Hold) stock has lost 46.9% compared with the industry’s 27.7% decline. The S&P 500 composite has returned 23.6% in the same time frame.

The developer, manufacturer and distributor of insulin delivery systems has a market capitalization of $16.21 billion. The company’s estimated long-term earnings growth rate of 22.2% is well ahead of the industry’s 12.5% growth. PODD’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 16.2%.

Let us delve deeper.

Upsides for Insulet

Omnipod 5 Gains Market Share: Omnipod 5 remains differentiated as a fully disposable, tubeless AID system that is expanding its installed base across both the U.S. and international markets. In first-quarter 2026, total company revenues grew 30.1% in constant currency, driven by Omnipod revenue growth of 33% in constant currency.

Management noted that its global customer base grew nearly 25% year over year, driven by higher new customer starts and retention trends consistent with the prior year. In the United States, growth included greater seasonality tied to deductible resets, but new customer starts improved through the quarter and into early second quarter. Internationally, growth continues to be supported by new customer starts and the conversion from Omnipod DASH to Omnipod 5, with Omnipod 5 now available in 19 countries.

Progress With Strategic Actions: Insulet is focused on driving growth in the global automated insulin-delivery market by expanding sensor connectivity and enhancing the Omnipod 5 experience. In the first quarter of 2026, the company completed a limited U.S. launch of Omnipod 5 integrated with Abbott Laboratories’ FreeStyle Libre 3 Plus and plans a broader rollout of the Libre 3 Plus integration and its latest algorithm update in the coming weeks.

Image Source: Zacks Investment Research

The company also enrolled the first participant in the EVOLVE pivotal study, which is intended to support a 510(k) filing in 2027. Supporting these initiatives, management raised its 2026 outlook, forecasting total company revenue growth of 21-23% and Omnipod revenue growth of 22-24%, while maintaining expectations for adjusted EPS growth of more than 25% for the year.

What Ails Insulet?

Tough Competitive Pressure: Insulet competes against large, established diabetes device companies and newer entrants offering pumps, smart pens, and other insulin delivery approaches. As AID adoption expands globally, management expects competition to increase, which can raise commercial spending requirements and heighten payer negotiations.

In the first quarter of 2026, SG&A expense increased 21.7% year over year as Insulet invested in sales force expansion, demand generation and customer experience programs. Over time, competitive intensity can reduce revenue growth durability or limit the pace of operating margin expansion, which is mentioned in 2026 guidance.

Economic Uncertainty and Supply Exposure: Insulet operates in a global healthcare supply chain that remains exposed to geopolitical and macro uncertainty. Management cited incremental raw material and shipping costs tied to the ongoing conflict in the Middle East as an offset to its 2026 margin outlook. These factors may lengthen sales cycles, increase cost variability and reduce visibility into achieving the company’s 2026 operating-margin expansion target.

PODD Stock Estimate Trend

The Zacks Consensus Estimate for Insulet’s 2026 earnings per share has remained unchanged at $6.46 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2026 revenues is pegged at $3.31 billion, implying a 22.2% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Integra LifeSciences IART and Phibro Animal Health PAHC.

Globus Medical has an earnings yield of 5.5%, well ahead of the industry’s negative 3% yield. Its earnings surpassed estimates in each of the trailing four quarters, the average surprise being 26.3%. The company’s shares have rallied 43.8% against the industry’s 4.8% decline over the past year.

GMED carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Integra LifeSciences, carrying a Zacks Rank #2 at present, has an earnings yield of 16% against the industry’s negative 3% yield. Shares of the company have gained 22.8% compared with the industry’s 4.8% growth. IART’s earnings topped estimates in each of the trailing four quarters, the average surprise being 16.8%.

Phibro Animal Health, carrying a Zacks Rank #2 at present, has an earnings yield of 9.2% compared with the industry’s 2.8% yield. Shares of the company have climbed 43.1% against the industry’s 27.9% decline. PAHC’s earnings beat estimates in each of the trailing four quarters, the average surprise being 16.3%.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Insulet Corporation (PODD): Free Stock Analysis Report

Integra LifeSciences Holdings Corporation (IART): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).