EZCORP, Inc. EZPW has gained investor attention as stronger pawn loan balances, acquisitions and store expansion continue to support revenue and earnings growth.

The key question is whether the company can sustain this momentum while managing higher costs, integration challenges and retail-related risks.

EZCORP Business Model Drives Growth

EZCORP generates revenues from pawn service charges, merchandise sales and jewelry scrapping. As of March 31, 2026, merchandise sales represented 47.9% of total revenues, pawn service charges accounted for 33.8% and jewelry scrapping contributed 18.2%.

Pawn loans create service charges when customers redeem or renew collateralized loans. Forfeited collateral can be sold as merchandise or scrapped for precious metals.

The core pawn remains the growth engine. Pawn loans outstanding increased 33% year over year to $349.4 million in the second quarter of fiscal 2026, supported by higher average loan balances, store expansion and demand for short-term liquidity.

EZPW Expansion Is Reshaping the Story

EZCORP ended the second quarter of fiscal 2026 with 1,506 stores across 16 countries, up from 1,360 stores at the end of fiscal 2025. Growth has come from de novo openings and acquisitions across the United States, Latin America and the Caribbean.

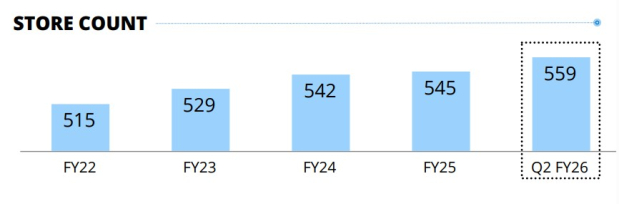

The Founders One transaction gave EZCORP control of a platform that includes Simple Management Group, adding 105 stores. The El Bufalo acquisition added 12 Texas stores, bringing its U.S. store count to 559 in the second quarter of fiscal 2026.

EZCORP U.S. Store Count

Image Source: EZCORP, Inc.

The company also continued opening stores organically, especially in Latin America, where it expanded its store count to 840 in the second quarter of fiscal 2026. In April 2026, it acquired 32 stores in Guatemala, further expanding its regional presence after quarter-end.

That footprint gives EZPW a larger earnings base. It also raises the execution test, because management must integrate acquired stores without letting costs dilute scale benefits.

EZCORP Earnings Momentum Looks Real

Recent results strengthened the bullish case for EZPW. Fiscal second-quarter 2026 revenues increased 46% year over year to $446.9 million, while gross profit rose 46% to $260 million.

The margin story improved as well. Adjusted EBITDA margin expanded 340 basis points to 18%, showing that revenue growth translated into better profitability.

While SMG contributed to growth, the improvement extended beyond the acquisition. Excluding SMG, total revenues increased 29% year over year, and gross profit rose 31%, pointing to strength in the existing platform.

Adjusted earnings per share increased 76% to 58 cents, and adjusted EBITDA advanced 76% to $76.9 million.

The Zacks Consensus Estimate for fiscal 2026 and 2027 earnings has remained unchanged over the past month, indicating year-over-year growth of 40% and 10%, respectively.

Estimate Revision Trend

Image Source: Zacks Investment Research

FirstCash Holdings FCFS and Enova International ENVA provide additional context within the broader alternative finance space. While FCFS serves as a direct benchmark as a leading pawn operator, ENVA offers exposure to non-traditional consumer lending.

The Zacks Consensus Estimate for FCFS earnings in 2026 and 2027 has remained unchanged over the past month, indicating year-over-year growth of 29% and 9%, respectively. For ENVA, earnings estimates for 2026 and 2027 have also remained unchanged, with expected year-over-year growth of 27% and 24%, respectively.

EZPW Risks Could Slow the Upside

EZPW’s expansion strategy brings cost pressure. Store expenses increased 33% in the second quarter of fiscal 2026, including a 13% same-store increase, with labor costs and Latin American minimum-wage increases among the drivers.

General and administrative expenses rose 37% year over year, reflecting higher labor costs, incentive compensation and expenses tied to SMG, which could weigh on margins.

Retail exposure is another risk. Merchandise sales are the largest revenue source, so weaker demand for pre-owned goods could pressure sales velocity and gross margin.

Gold prices also matter. Jewelry scrap sales surged in the second quarter of fiscal 2026, and scrap margin widened as gold prices rose, but that benefit could reverse if metal prices move lower.

EZPW Ratings Highlight a Balanced Growth Setup

The bottom line remains balanced. EZCORP's pawn loan growth, expanding footprint and operating leverage support its improving fundamentals, but integration risks, cost inflation and retail sensitivity remain key offsets.

EZPW currently carries a Zacks Rank #3 (Hold), which points to a neutral near-term earnings revision picture. That fits a setup in which the operating story has improved, but investors may still want confirmation that growth remains profitable. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Over the past six months, EZPW shares have gained 65.8% against the industry’s 11.4% decline.

Price Performance

Image Source: Zacks Investment Research

The Style Scores are more constructive. EZPW has a Value Score of B, Growth Score of B and VGM Score of B, indicating favorable characteristics across investing styles. However, its Momentum Score of D remains the key caution flag.

For now, EZPW's operating momentum is worth watching. Strong pawn loan growth and store expansion support the long-term story, but investors may want confirmation that these gains can continue without eroding margins.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EZCORP, Inc. (EZPW): Free Stock Analysis Report

FirstCash Holdings, Inc. (FCFS): Free Stock Analysis Report

Enova International, Inc. (ENVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).