Shares of Willis Towers Watson Public Limited Company WTW have gained 1.1% in three months compared with the industry’s growth of 9.4%.

WTW is well positioned for long-term growth, supported by continued margin expansion, AI-driven productivity initiatives, a strong specialty business pipeline, disciplined capital returns and earnings contributions from strategic acquisitions. The expected long-term earnings growth is pegged at 15.9%, better than the industry average of 13.6%.

Image Source: Zacks Investment Research

Shares of other insurance brokers like Aon plc. AON and Arthur J. Gallagher & Co. AJG and Brown & Brown, Inc. BRO have gained 10.6%, 16.6% and 3.2%, respectively, in the past three months.

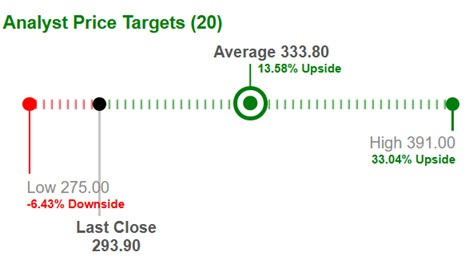

WTW's Average Target Price Suggests Upside

Based on short-term price targets offered by 20 analysts, the Zacks average price target is $333.80 per share. The average suggests a potential upside of 13.6% from the last closing price.

Image Source: Zacks Investment Research

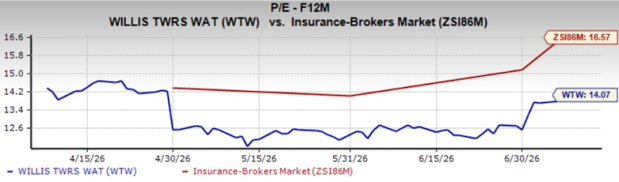

WTW’s Valuation

Shares of Willis Towers Watson are trading at a discount compared with the industry. Its forward price-to-earnings multiple of 14.07X is lower than the industry average of 16.57 X. It, however, has a Value Score of B.

Image Source: Zacks Investment Research

WTW’s Growth Projection Encourages

The Zacks Consensus Estimate for Willis Towers Watson's 2026 earnings per share (EPS) indicates a year-over-year increase of 14.5%. The consensus estimate for 2026 revenues is pegged at $10.50 billion, implying a year-over-year improvement of 8.1%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 13.3% and 5.2%, respectively, from the corresponding 2026 estimates.

Optimistic Analyst Sentiment on WTW

Four of the five analysts covering the stock have raised estimates for 2026, while two of the four analysts have increased 2027 estimates over the past 60 days. Thus, the Zacks Consensus Estimate for 2026 and 2027 moved 0.3% and 0.1% north, respectively, over the last 60 days.

WTW’s Favorable Return on Equity

Willis Towers Watson’s return on equity (ROE) of 21.5% for the trailing 12 months compared favorably with the industry’s 18.8%, reflecting the company’s efficiency in utilizing shareholders’ funds.

Factors Benefiting WTW

Willis Towers continues to benefit from a healthy pipeline across its specialty businesses. Strong client wins in data centers, nuclear energy, surety, construction and commercial insurance, including a major Fortune 100 account, are expected to support revenue growth in the coming quarters. WTW is also re-entering the reinsurance market through a joint venture with Bain Capital, which is expected to be a roughly 30-cent headwind to adjusted EPS in 2026.

WTW's AI strategy and margin expansion remain key long-term growth drivers. Management expects AI-driven automation and analytics to improve productivity, strengthen client engagement and expand margins. It also expects continued annual margin expansion over the coming years.

The company’s acquisition of Newfront adds a technology-enabled, middle-market broker operating across both Health, Wealth & Career and Risk & Broking, aligning with WTW’s focus on specialization, innovation and efficiency. Management expects Newfront to contribute about $250 million of post-close revenues in 2026 with an adjusted EBITDA margin of nearly 26%, though it is expected to have an approximately 10-cent impact on adjusted EPS in 2026.

Rising healthcare costs and increasing benefit complexity are driving demand for WTW's health consulting, and the health segment revenue grew 6% during the first quarter of 2026. Management expects high-single-digit growth for 2026.

Willis Towers Watson's solid balance sheet and steady cash flow are expected to help the company deploy capital through buybacks, dividend payouts, debt repayments and acquisitions. The company returned $388 million to shareholders during the first quarter of 2026 through share repurchases and dividends, and expects share repurchases of $1 billion or greater in 2026.

Risks for WTW

WTW's first-quarter organic revenue growth slowed due to project delays and softer market conditions. Prolonged weakness in organic growth could pressure revenue expansion and investor sentiment.

Wills Towers continues to face risks from geopolitical tensions and economic uncertainty, particularly in international markets, which may delay client spending and consulting projects.

Unfavorable exchange-rate movements could also negatively impact earnings and operating results despite the company's hedging programs.

Conclusion

Willis Towers Watson boasts growth through AI initiatives, specialty insurance expansion, the Newfront acquisition, effective capital deployment and continued margin improvement. However, slower organic growth, geopolitical uncertainty and foreign exchange volatility remain key risks.

Its solid growth projections, optimistic analyst sentiment, cheap valuations and favorable ROE should continue to benefit Willis Towers Watson over the long term. The stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Willis Towers Watson Public Limited Company (WTW): Free Stock Analysis Report

Aon plc (AON): Free Stock Analysis Report

Arthur J. Gallagher & Co. (AJG): Free Stock Analysis Report

Brown & Brown, Inc. (BRO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).