Helen of Troy Limited HELE reported first-quarter fiscal 2027 results, wherein both top and bottom lines beat the Zacks Consensus Estimate. While net sales increased, earnings decreased from the year-ago period’s actuals. Management raised net sales guidance for fiscal 2027.

HELE’s Quarterly Performance: Key Metrics & Insights

Helen of Troy posted adjusted earnings of 17 cents per share, beating the Zacks Consensus Estimate of 2 cents. However, the bottom line declined 58.5% from 41 cents reported in the year-ago period.

Helen of Troy Limited Price, Consensus and EPS Surprise

Helen of Troy Limited price-consensus-eps-surprise-chart | Helen of Troy Limited Quote

The company reported net sales of $402.1 million, which beat the Zacks Consensus Estimate of $375 million. The top line increased 8.2% from $371.7 million posted in the year-ago period, driven by growth across both business segments. Home & Outdoor benefited from strong international demand for packs, successful new product launches and a favorable comparison to the prior year due to tariff-related order timing. Beauty & Wellness growth was led by strong sales of nail care products, fans and thermometers.

The consolidated gross margin decreased 110 basis points to 46% in the quarter, primarily due to the net unfavorable impact of tariffs, higher inventory obsolescence costs compared with the prior year and a less favorable customer mix within Home & Outdoor. We estimated a 47.5% gross margin.

The consolidated SG&A ratio decreased to 31% from 45.1% posted in the year-ago period, reflecting a $54.9 million pre-tax gain from the sale of a distribution facility, lower outbound freight costs, reduced depreciation and amortization, favorable operating leverage and the absence of $3.5 million in CEO succession costs incurred in the prior-year period.

The adjusted operating income remained flat at $16.1 million, while the adjusted operating margin decreased 30 bps to 4%. The margin compression was primarily caused by tariff-related cost pressures, a less favorable inventory obsolescence impact year over year and an unfavorable customer mix within Home & Outdoor, partially offset by reduced outbound freight costs and favorable operating leverage. We expected an adjusted operating margin of 3% for the quarter.

HELE’s Segmental Performance

Net sales in the Home & Outdoor segment increased 9.5% to $194.9 million, driven by strong international demand for technical, lifestyle and travel packs, new product launches, expanded distribution in the home and insulated beverageware categories, and a favorable comparison to the prior year due to tariff-related order timing. These gains were partially offset by lower international sales in the home and insulated beverageware categories.

Home & Outdoor adjusted operating income increased 39.2% to $12.3 million, while the segment adjusted operating margin increased 130 bps to 6.3%.

Net sales in the Beauty & Wellness segment gained 7% to $207.2 million, driven by growth in nail care from new and expanded distribution, higher fan and thermometer sales benefiting from an easier comparison against prior-year tariff-related direct import cancellations and disruptions in the China thermometry market, and incremental sales from new Wellness product launches.

Beauty & Wellness adjusted operating income declined 48.2% to $3.8 million, while the segment adjusted operating margin decreased 190 bps to 1.8%.

HELE’s Financial Position

Helen of Troy ended the quarter with cash and cash equivalents of $21.7 million and total short and long-term debt of $716.1 million. Net cash used by operating activities for the fiscal first quarter was $0.6 million. The free cash flow for the same period was negative $6.4 million.

HELE’s Outlook

For fiscal 2027, the company raised its net sales guidance to $1.759-$1.831 billion, from the previous range of $1.751-$1.822 billion. The updated outlook includes Home & Outdoor sales of $859-$884 million (previously $854-$882 million) and Beauty & Wellness sales of $900-$947 million (previously $897-$940 million).

Adjusted earnings are still expected in the range of $3.25 to $3.75 per share, with adjusted EBITDA of $190 million to $197 million and free cash flow of $85 million to $100 million.

Management expects continued inflationary pressures, weak discretionary demand, cautious retailer inventory management and a highly promotional environment. The outlook assumes current tariff rates remain in place, includes $9.2 million in Phase 1 tariff refunds and excludes potential future refunds due to uncertainty. It also factors in higher product and freight costs, unfavorable Chinese yuan movements, and ongoing geopolitical and supply-chain risks that may increase input costs and disrupt supply.

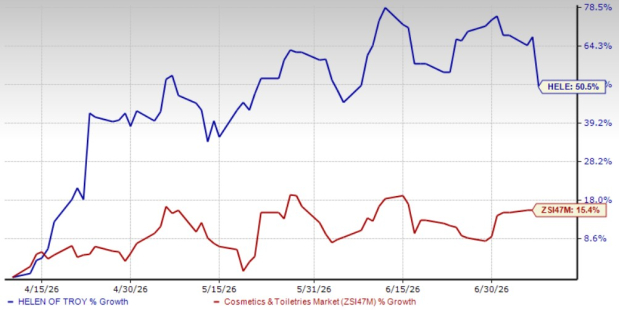

This Zacks Rank #3 (Hold) company has gained 50.5% in the past three months compared with the industry’s growth of 15.4%.

Image Source: Zacks Investment Research

Stocks to Consider

The Estee Lauder Companies Inc. EL manufactures, markets and sells skin care, makeup, fragrance and hair care products worldwide. It currently has a Zacks Rank of 2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Estee Lauder’s current fiscal-year sales and earnings calls for growth of 4.5% and 59.6%, respectively, from the year-ago reported numbers. EL delivered a trailing four-quarter average earnings surprise of 39.1%.

Mama's Creations, Inc. MAMA manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA holds a Zacks Rank of 2. Mama's Creations delivered a trailing four-quarter earnings surprise of 129.2%, on average.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 30% and 73.3%, respectively, from the year-ago figures.

Hormel Foods Corporation HRL develops, processes and distributes various meat, nuts and other food products to foodservice, convenience store and commercial customers in the United States and internationally. It carries a Zacks Rank of 2 at present. HRL delivered a trailing four-quarter earnings surprise of 3.2%, on average.

The Zacks Consensus Estimate for Hormel Foods’ current fiscal-year sales and earnings indicates growth of 1.5% and 9.5%, respectively, from the prior-year reported levels.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Helen of Troy Limited (HELE): Free Stock Analysis Report

The Estee Lauder Companies Inc. (EL): Free Stock Analysis Report

Hormel Foods Corporation (HRL): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).